From: Steve Ambler and Jeremy M. Kronick

To: Bank of Canada Governing Council

Date: July 20, 2022

Re: Thanks, We Needed That. Why the Bank Move Was the Right One

Last week, the Bank of Canada increased the scope of its interest rate increases, raising its overnight rate target by 100 basis points to 2.5 per cent. We haven’t seen a hike that big since 1994, and the target rate is now higher than at any time since before the financial crisis in 2008.

With mortgage and other market interest rates increasing with the overnight rate, fears of a recession are mounting.

There are two big questions.

First, is the blunt overnight rate the only inflation-fighting option? Second, how bad will the recession need to be to bring inflation back down?

Unfortunately, the answer to the first question is no, there aren’t any viable alternatives. However, the recession that could result might not be as bad as feared.

Some analysts argue against rate hikes. They think Canada’s inflation is mostly a supply-side problem, originating in high oil prices because of the Ukraine war and snarled supply chains. They advocate a wait-and-see approach and think that rate hikes are mostly futile.

Supply problems matter, but inflation reflects the balance of supply and demand for goods and services, and inflation is too widespread to attribute it only to the former. According to the Bank of Canada’s July monetary policy report, more than 70 percent of the goods and services in the consumer price index – an average measure of the price households pay for goods and services – showed inflation above the top end of the Bank’s 1-to-3 percent target band in May.

The fact that inflationary pressures are so widespread is not surprising. Money growth rates hit 40-year highs during the pandemic, and chequing and savings accounts ballooned to unprecedented levels. Excess money becomes less valuable – and that means rising prices. Higher interest rates will curtail money growth by dampening bank loans, for example. Spending will drop as households save more, bringing inflation down.

Is a possible recession a worthwhile tradeoff for lower inflation? Most economists subscribe to the idea that as unemployment falls, economic growth picks up until a level where demand starts to exceed supply, causing higher inflation (and vice versa.) The thinking then goes that to tame inflation, we need to bring economic growth to heel, which causes unemployment to go up.

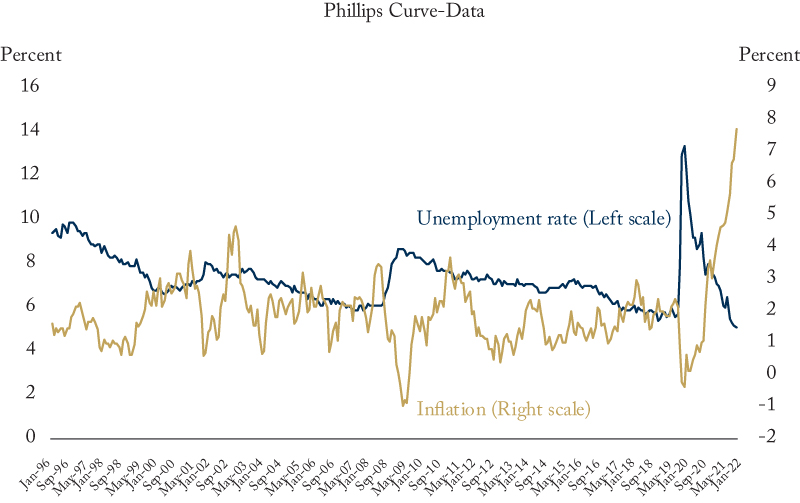

However, for much of the period since central banks started targeting inflation, swings in unemployment have not led to much movement in inflation – economists call it a flat Phillips Curve. The implication is that to get big movements in inflation, as we now need, the price will be a huge increase in unemployment.

The problem with this analysis is that when the central bank is doing a good job of keeping inflation close to the 2 percent target – as it has largely done since 1995 – future inflation is unrelated to current economic conditions. But when inflation is out of its ideal range, as was the case during the Great Recession, and is the case today, a more standard relationship between inflation and the state of the economy returns. This includes a normal negative slope between unemployment and inflation, which is very apparent in the data from both the Great Recession and the pandemic period (see Figure).

All this suggests that the unemployment required to bring down inflation may be less painful than implied by looking at data over the entire inflation-targeting era.

Nevertheless, there will be pain. A recession would disproportionately hurt low-income households as some workers lose jobs and people are forced to make unacceptable trade-offs, such as between eating and heating.

On the other hand, the longer high inflation persists, the more it will eat into purchasing power, forcing these same lower-income households to make the same trade-offs. Worse, as high inflation becomes embedded into expectations, it will make it even harder to tame the inflation beast down the line. And, while governments have tools to help in recessions – as we saw at the beginning of the pandemic – their tools to help with rising inflation are much weaker, and are often counterproductive.

It is a bad trade-off, which underscores why inflation targeting is so important.

These hikes are going to hurt, but they are the only option we have.

Steve Ambler, a professor of economics at the Université du Québec à Montréal, is the David Dodge Chair in Monetary Policy at the C.D. Howe Institute where Jeremy M. Kronick is associate director of research.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the authors. The C.D. Howe Institute does not take corporate positions on policy matters.

A version of this Memo first appeared in The Globe and Mail.