To: Canada’s Policymakers

From: Mawakina Bafale and Andrew Spence

Date: April 24, 2023

Re: Expanding Competition in the Canadian Banking Sector

Canada’s recent record on business investment has been jarring in its weakness, with available capital per worker in a sustained decline that undermines the economy’s capacity for productivity growth, innovation and dynamism.

This is true for financial services as well.

Creating more competition in the sector might sound counterintuitive given the collapse of financial institutions in our more notoriously competitive neighbours to the south, but one does not preclude the other. We need stability – but we also need dynamism.

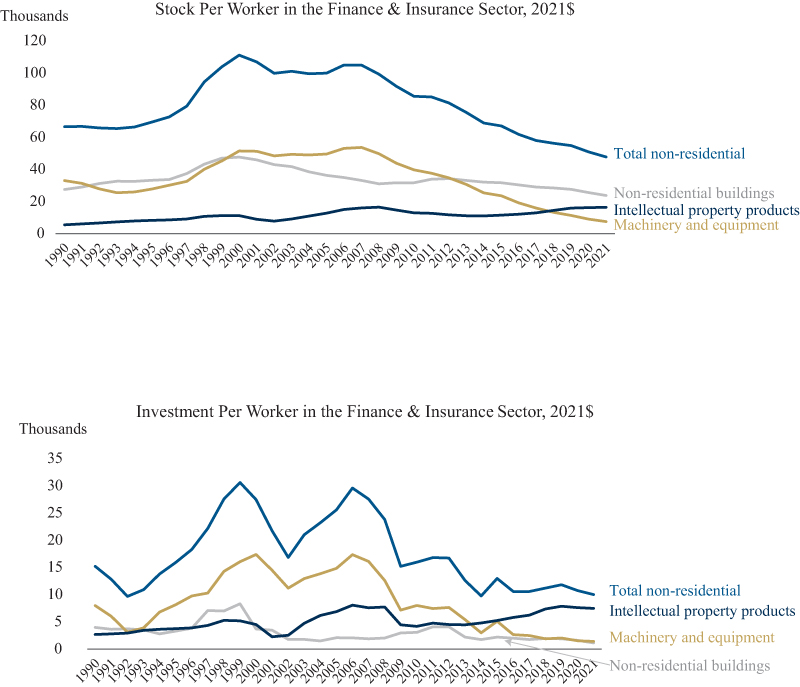

Canadian banks consistently outperform international peers in terms of return on equity. A good thing. However, this financial strength is not leading to strong investment in the sector’s workers.

The stock of non-residential capital relative to the labour force in financial services peaked in the early 2000s (Figure 1). But by 2021, it was 57 percent below that peak. The good news is the stock of intellectual property products (IPP) – key to sectors such as financial services – is increasing. Even so, investment per worker has been falling across all types of capital, and of late, even IPP is down, 5 percent lower than its pre-pandemic level (Figure 2). At a time when it is increasingly important to invest in software to protect consumer data from cyber threats, this is not good news.

More competition will help.

With the collapse of Silicon Valley Bank (SVB) triggering a number of other bank collapses, it might seem odd to promote increased competition in the financial sector – not least of which because none of the bank failures are Canadian. However, it is possible to have a regulatory and policymaking focus on stability, while promoting the kind of dynamism necessary to sustainably grow our economy.

The SVB failure ostensibly supports Canada’s focus on bank safety and can easily be interpreted as a warning of the dangers of competition in such a sensitive piece of public infrastructure. However, it can also be interpreted as a simple failure of adequate regulation and supervision, and not as a warning of the dangers of competition.

SVB’s failure demonstrates the need for key risk management regulations backed up with close supervision. Moreover, it demonstrates the need to observe and adhere to some basic risk management requirements that minimize the probability of a bank run. Banks must have a diversified portfolio of assets and a diversified source of deposit financing, backstopped with deposit insurance. Banks also need to minimize interest rate risk to avoid insolvency because of illiquidity. SVB would have remained solvent if its bond holdings, which had declined in value as interest rates increased, could have been marked to maturity. The forced sale to cover withdrawal requests meant the bonds had to be marked to market and the loss realized.

Canada is a leader in financial regulation and supervision. However, we have fallen behind in encouraging more competition across the sector. And, to be clear, we can have both things. The goal should be to use financial stability as a tool to encourage an efficient, dynamic, financial services sector, one that innovates and offers more affordable services to Canadians. This urgency is not reflected in the government’s current efforts.

As a first step to reform, Canada needs to design a modern regulatory framework. In this regard, competition policy should be independent of prudential regulation. A competitive outcome for banking should be defined, and objectives set. Prudential regulation should be designed to ensure that a more competitive and dynamic system remains safe through prescriptive regulations and supervision.

A second step is to ask what, specifically, can be done to drive productivity growth. Canada has been working for some time to modernize its payment structures. Some of its efforts have been slow to materialize. The implementation of the real-time retail payments system via the real time rail (RTR) has been delayed several times. It would provide continuous and immediate settlement of retail payments. More than 50 countries already use RTR, including all other G20 members.

Additionally, Ottawa has been slow on open banking, which has been under review since 2018 – a full five years ago. Open banking gives customers control over their data, leading to the tailored products and services that would drive competition and, therefore, productivity. Canadians are missing out. We urge the government to get going.

Canada’s focus on banking system stability is understandable given its success in avoiding some of the perils encountered south of the border. It should also turn its attention to the kind of competition necessary to improve our weak productivity. The federal government’s recent efforts to implement open banking and modernize our payments industry are steps in the right direction, but more is needed – and at a quicker pace to benefit all Canadians.

Mawakina Bafale is a Research Assistant at the C.D. Howe Institute, and Andrew Spence is former Global Head of Rates and FX Research at TD Securities, and VP and Chief Economist for Ontario Teachers’ Pension Plan.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the authors. The C.D. Howe Institute does not take corporate positions on policy matters.