To: Bank of Canada Governing Council

From: Ed Devlin and Anders Forssell

Date: August 22, 2022

Re: Quantitative Tightening May Cause Unexpected Trouble

After bridging the unprecedented pandemic lockdown, we now have inflation the likes of which we haven’t seen in 40 years. In response, the Bank of Canada (BoC) has hiked the overnight rate at a dizzying pace – 2.25 percentage points to-date. It is letting the bonds it bought during the pandemic roll off its balance sheet, a process called quantitative tightening (QT). We lay out the case here for why QT could cause trouble for the Bank of Canada as they navigate the economy through these turbulent times.

QT is the term used to describe the shrinking of a central bank’s balance sheet. During the pandemic, the BoC purchased over $300 billion of Government of Canada (GOC) bonds (QE), funding government programs to provide relief to vulnerable Canadians. While successful at first, it went on too long. Inflation is currently too high, and the Bank is using QT along with overnight rate hikes to reduce inflation. This is the first time the BoC has tightened interest rates while simultaneously engaging in QT. A novel experiment, which is why QT deserves a close look.

Research that tries to quantify the impact of QE has found minimal impact, but this does not necessarily mean the reverse will be true with QT. With QE, there was policy coordination in that the federal government set the amount of new bonds to be issued while the BoC agreed to buy a certain amount. This coordination limited the impact of the fiscal expansion on “market determined” interest rates.

The big question: how much will QT cause government interest rates to rise? Unclear, but since the BoC is no longer buying, other private sector investors will determine the market clearing yield. This should cause a greater increase in interest rates than the decrease seen with QE.

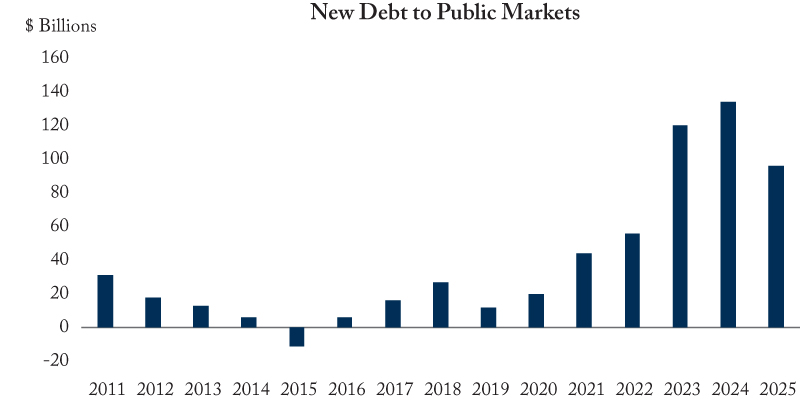

Here is a basic framework to assess the potential impact of QT on bond yields. First, we need to understand how much new debt the GoC will issue due to future deficits. Second, we project the BoC balance sheet under the announced QT program. And, lastly, subtracting the second step from the first, we can determine how much debt markets will have to finance now that the BoC is engaging in QT (see Figure). The massive increase in new issuance to be purchased in the open market should increase interest rates, but by how much?

During his press conference on May 4, 2022, US Federal Reserve Chair Powell estimated (admittedly, with uncertainty) that US$1 trillion in QT was equivalent to a one-time interest rate increase of ¼ percentage points. One of the main determinants of how high interest rates will go because of QT is the maturity profile of the new public debt issuance to the open markets.

Adjusting the Fed’s estimate for QT to the size of the Canadian economy, and the differences in the projected weighted average life of new debt issuances, we project the C$200 billion QT program that will end in FY 2024/25 to be worth approximately the equivalent of a 0.5 percentage point rate hike.

The GoC bond market is much less liquid than the US Treasury market. While liquidity can vary dramatically, based on our experience, the GoC market is generally 10-20 percent of US liquidity. This would apply further upward pressure on our 0.5 percentage point estimate.

The market impact of QE/QT is highly state-dependent, and will have significant effects in dysfunctional markets. We suspect the implementation of QT in a bear market, where investors are experiencing losses, may make liquidity problems worse.

So, what does this all mean? Getting inflation back to the 1-3% target range is the most important policy goal for the BoC and it should tighten monetary policy to ensure the BoC maintains its hard-won inflation fighting credentials. Within this inflation-targeting framework, we suggest that:

- The BoC should bear in mind that Canada and the world have little experience with QT and the risk of unforeseen consequences is correspondingly high;

- Flexibility is more important than predictability. QE theory and empirical evidence suggest that it should lower rates across the yield curve but that longer maturities are affected the most. Also, through lower discount rates and portfolio rebalancing QE increases asset prices in general and tightens credit spreads. QT will reverse some of these market moves and there is a risk that the effect in some markets will be disorderly. The BoC should be flexible when implementing QT both in terms of the size and pace of the operation and adjust to market conditions;

- Combining QT with higher rates may tighten financial conditions and slow the economy more than current models predict;

- If true, the BoC should be cautious and flexible in changing the policy rate now that the overnight rate is at the estimated neutral rate; and

- If the BoC sees forward expectations of inflation slowing more than expected, it should be willing to cut interest rates or slow down or stop QT. It would be most unfortunate for economic weakness to create a situation where the overnight rate is at the effective lower bound with inflation below target, again.

Ed Devlin is the Founder of Devlin Capital and a Senior Fellow at the C.D. Howe Institute, and Anders Forssell is a Partner at Devlin Capital.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the authors. The C.D. Howe Institute does not take corporate positions on policy matters.