From: Don Drummond and Alexandre Laurin

To: Finance Minister Chrystia Freeland

Date: September 29, 2022

Re: Federal Finances: This is No Time for Loose Pursestrings

After the pandemic-induced swelling of the federal government’s deficit and debt burden, there has been some apparent good fiscal news of late.

The Parliamentary Budget Office (PBO) declared federal finances “sustainable.” Its projection shows that under the status quo the federal net debt would be eliminated by 2061. Spending could rise or taxes decline by 1.8 percent of GDP and the net debt-to-GDP ratio would remain stable at 39.4 percent.

Next, the federal government reported a surplus of $10.2 billion for the first quarter of 2022-23. In this context, it announced a multi-billion dollar package to help some Canadians cope with inflation amid calls for more relief. Does the good fiscal news mean higher government spending or tax cuts can be handled easily? We do not believe so.

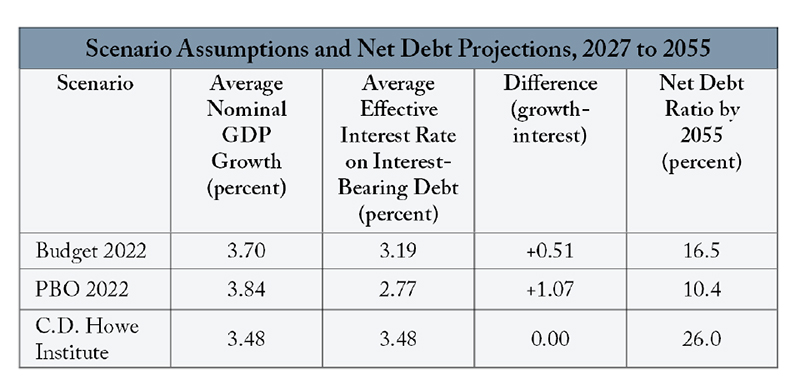

The PBO fiscal sustainability report is based on economic assumptions that should be questioned. From 2027 to 2055, it assumes average annual nominal economic growth of 3.84 percent and an average effective interest rate on interest-bearing debt of 2.77 percent. The positive difference between growth and the interest rate of 1.07 percentage point is a key reason the debt burden ratio is projected to decline so steeply under the status quo and why the ratio can be sustained at 39.4 percent even with higher spending or lower taxes. Growth has exceeded the effective interest rate in recent years, but this is not the normal historical relationship nor what theory would predict to hold over the long term.

A stable net debt-to-GDP ratio as a fiscal sustainability goal should also be questioned as this ratio is now high by historical standards, and in particular well above the burden prevailing before COVID-19 struck. Stabilizing the debt burden at that level would leave a fiscal vulnerability.

The fiscal surplus over the first three months of 2022-23 is welcome, but we must keep in mind the perilous economic times that may be ahead as efforts are applied to bring inflation back to 2 percent. A recession is by no means certain, but it is a distinct possibility. That would quickly and strongly turn around the recent, favourable fiscal results.

To present a more balanced view of long-run fiscal prospects, we present fiscal projections along the lines done by the PBO and Finance Canada using different, but we believe, realistic assumptions.

Source: Authors calculations. Budget’s average effective interest rate is our estimate extrapolating from the budget’s disclosed assumptions. Our GDP and net debt long-run scenarios follow the methodology in “Rolling the Dice” updated for new Statistics Canada’s population projections and Budget 2022 projections.

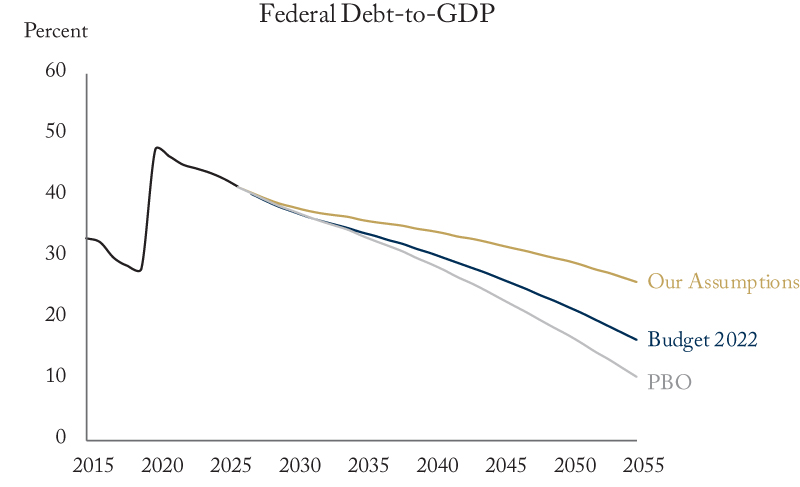

With the large positive differential between growth and the effective interest rate on debt, the PBO scenario produces a debt burden dropping sharply, down to 10.4 percent by 2055. The Budget 2022 growth and interest rate assumptions yield a debt burden in 2055 of 16.5 percent. With our assumption of growth equal to the effective interest rate the debt burden still declines steadily, but we only go back to the pre-pandemic debt-to-GDP mark by 2050.

Allowing for the possibility of economic weakness due to efforts to bring inflation back to 2 percent, and using realistic long-term economic assumptions, suggests the Canadian federal government’s balance sheet can return to an acceptable position over the next few decades following the surge in deficits and debt relating to COVID-19. But there is little scope for net new spending or tax cuts. Programs targeted at various objectives will need to be funded through spending reallocation or tax increases.

Don Drummond is Stauffer-Dunning Fellow and Adjunct Professor at the School of Policy Studies at Queen's University and a C.D. Howe Institute Fellow-in-Residence. Alexandre Laurin is Director of Research at the C.D. Howe Institute.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the authors. The C.D. Howe Institute does not take corporate positions on policy matters.