To: Canada’s budget observers

From: Alexandre Laurin, William B.P. Robson and John Lester

Date: April 6, 2023

Re: 2023 Federal Budget Buries Prudence under Billions of New Spending and Borrowing

A major theme in the run-up to the 2023 federal budget was the government’s commitment to prudence.

Prudence was also a major theme in the run-up to the 2022 budget. Both times, the run-up proved misleading. Last year’s budget hiked projections for spending and borrowing. This year’s also involves much higher future spending and borrowing than the run-up led us to expect, ruling out the 2027-28 return to surplus promised last year.

Because the fiscal plan buries the key numbers under hundreds of pages of political messaging and re-hashed material, it takes some digging to discover how much the budget repeats the imprudence of its predecessors. One point of contrast is that, in the 2021 and 2022 budgets, strong revenue growth improved the status quo bottom line. Rather than return the budget to surplus, as the government could easily have done on those occasions, it spent nearly all the windfall. In 2023, lower-than-anticipated revenue growth, mainly driven by a mild downturn this year, and higher-than-expected expenses, mainly driven by increasing interest on the federal debt, worsened the status quo bottom line. But the policy reaction is the same: spend more – a total of about $65 billion more over the projection horizon.

The government says it will cover about one-sixth of the cost of new spending by trimming operations and cutting outsourced professional services. But spending reviews promised in the recent past have so far come to little. The budget also promises new revenues, particularly from the revamped Alternative Minimum Tax, the corporate Global Minimum Tax, and the denial of the inter-corporate dividend deduction on shares held by banks. But those new revenues will only come in if the affected taxpayers do not react, which experience suggests is unlikely.

Spending and borrowing more in both good times and bad is not new. Many countries, including Canada, have done it before and are now doing it again. Governments often believe expansionary fiscal policy should support demand, even in booms. They dismiss concerns about deficits unfairly shifting the cost of government services to the future, possibly because they believe future generations will be richer. Or it may be simple populism: Gain a short-term electoral advantage with handouts and services that current voters can enjoy, while sticking future voters with the bill.

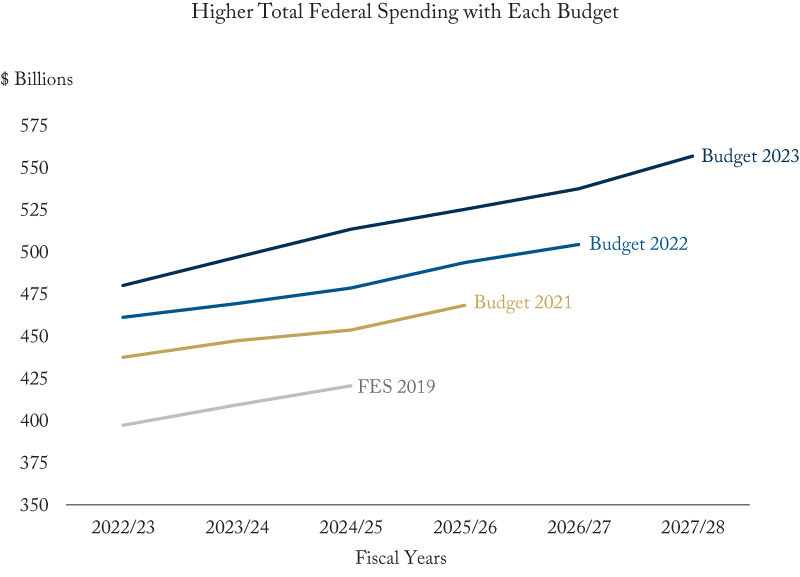

Whatever its motives, this federal government is all-in on spending and borrowing. The last year in the fall 2019 fiscal update’s projections – the last pre-COVID projection – was 2024-25. In the 2020 fall update, projected spending for 2024-25 was $9 billion higher than it had been a year earlier. The 2021 budget added another $24 billion, the 2021 fall update $11 billion, the 2022 budget $14 billion, the 2022 fall update another $26 billion, and now the 2023 budget adds another $9 billion. That’s a total add-on of an astonishing $93 billion. Projected spending for 2024-25 has been growing roughly $13 billion every six months (see Figure).

Finance Minister Chrystia Freeland cites a projected decline in the debt-to-GDP ratio over the next 30 years as proof of the government’s prudence and fairness to future generations. But that projection is recession-free. The next 30 years will inevitably bring recessions and governments will inevitably respond with more spending and borrowing.

A recent study by two of us (Alex Laurin and John Lester) uses past experience to simulate scenarios with recessions. Applied to the budget’s base case, its approach shows a one-in-four chance the debt ratio will rise from its 2027-28 value over the next three decades. A truly prudent fiscal plan would make failure to reduce the debt ratio much less likely.

A government that wanted to be fair to future generations would pay down the cost of temporary COVID-19 supports before generations that did not benefit from them start paying taxes, i.e. by 2040-41. Doing that with enough certainty while allowing for business cycles would require fiscal restraint equivalent to raising the GST by four percentage points by 2027-28. Simply returning the debt ratio to its pre-pandemic level of 30.7 percent, a substantially less demanding target, would require restraint equivalent to raising the GST by two percentage points.

On current evidence, getting federal finances on a prudent path that is fair to future generations will require the government to surrender some of the fiscal flexibility it has been using so unwisely. One option would be legislation requiring it to set out a ceiling on non-cyclical spending, so that revenue windfalls are saved, not spent. Whatever option we choose, Budget 2023 underlines that the current approach leads nowhere good.

Alex Laurin is Director of Research at the C.D. Howe Institute where William B.P. Robson is CEO. John Lester is an Executive Fellow with the School of Public Policy at the University of Calgary.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the authors. The C.D. Howe Institute does not take corporate positions on policy matters.

A version of this Memo first appeared in the Financial Post.