From: William B.P. Robson

To: Federal Economic Ministers

Date: July 6, 2022

Re: Higher Productivity Would Help Fight Inflation

Canadians are beset by economic problems. Inflation is hammering their purchasing power. Forecasters are predicting weak, if any, rise in living standards. And now it seems that tighter monetary policy may cause a recession.

The list of challenges seems dauntingly long. On the other hand, they have a single underlying cause: slow growth of Canada’s productive capacity. Governments, especially the federal government, can and should help.

Inflation is high because fiscal and monetary stimulus has pushed demand above the level our economy can supply. If we could produce more, the mismatch between too much money and too little output would be less severe, and our purchasing power would not be falling so fast.

We are hearing warnings about weak growth in living standards largely because business investment in Canada is so low that our stock of capital per worker is falling. Too many Canadians are working with equipment that has worn out and intangible capital that has gone obsolete. Low investment also means less of the innovation and technological progress that raise living standards over time.

Slow growth of productive capacity also increases the risk of recession – actual declines in real activity. To get inflation down, the Bank of Canada needs to bring demand back into line with supply. If productive capacity were growing fast, that might mean slower growth in the volume of spending for a quarter or two. But with productive capacity growing as slowly as it is, the volume of spending may have to fall.

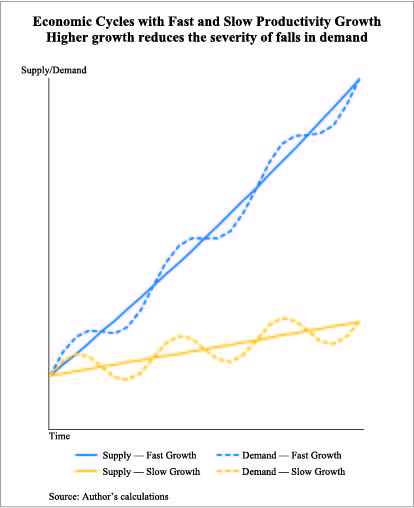

The nearby chart makes the point. Suppose the economy’s ability to supply goods and services was rising at 4 percent per year. Bringing demand back into line with supply might mean reducing its growth from 5 percent to 3 percent. Disappointing, perhaps, but hardly a disaster. On the other hand, if supply is growing at only 1 percent a year, then bringing demand into line might mean reducing its annual growth from 2 percent to 0 percent. Zero real growth and below – when the economic pie is actually shrinking – makes the pain and squabbling over who gets what worse.

Bottom line: When supply is rising fast, the central bank can keep demand close to supply without large risk of recession. Periods when demand actually falls are rare and short. But when supply is rising slowly, the fluctuations hurt more. Recessions happen more often and last longer.

The chart and those numbers understate the challenge the Bank of Canada faces now. Inflation close to 8 percent shows that demand is running far above supply. To get it back to 2 percent, demand will have to run well below supply. So the odds of at least a couple of quarters of falling real activity over the next two years are high.

Although the challenge right now is especially severe, the key point from the chart’s stylized scenarios still holds. Faster growth of Canada’s productive capacity would make bringing demand back in line with supply easier. We could hold the line on demand while supply catches up, rather than push demand down. We could lower inflation with less risk of recession.

The Bank of Canada cannot do much about the productive capacity of the Canadian economy, but governments can. They can free up resources for more productive uses by spending less. They can encourage investment by keeping taxes low, neutral and stable. And they can build confidence with transparent and predictable regulation.

Unfortunately, the federal government’s current directions promise no help for productive capacity. It continues to increase spending. It is depressing investment with discriminatory tax hikes – singling out specific sectors, such as banks and insurers, and specific products, such as cars, airplanes and boats – and it now proposes tighter limits on deductibility of interest when businesses borrow to invest. It is undercutting confidence with changes to competition law and greenhouse gas policies that seem longer on slogans than practicality.

As former Finance Minister Bill Morneau emphasized in a recent speech to the C.D. Howe Institute, the federal government has neglected economic growth, and needs to prioritize it. Faster growth of productive capacity in Canada would help lower inflation. It would yield higher living standards. And it would reduce the risk of recession.

A good time for a turnaround on productivity policy would be right now.

William B.P. Robson is the CEO of the C.D. Howe Institute.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the author. The C.D. Howe Institute does not take corporate positions on policy matters.

An earlier version of this Memo first appeared in the Financial Post.