The Study In Brief

- A green wave of regulations is headed for Canada’s banks. Regulators at home and abroad are generating new rules for financial institutions regarding the monitoring, disclosure and mitigation of climate-related risks.

- In Canada, the Office of the Superintendent of Financial Institutions (OSFI) has issued an initial draft guideline on climate-risk management for federally regulated financial institutions, and is seeking comment from stakeholders before issuing a revised version in early 2023.

- Globally there is a rapid if uneven evolution toward adoption of the disclosure guidelines proposed by the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD), with momentum building toward mandatory adoption. To implement the TCFD recommendations, banks will need to obtain more standardized and detailed information from their clients on the business and projects being financed and how the business and related climate impacts will evolve over time.

- Amid this green regulatory wave, this E-Brief focuses on a crucial question: Should banks’ capital requirements be increased to reflect climate-related risks?

Introduction

The Bank of Canada and the Office of the Superintendent of Financial Institutions (OSFI) released an analysis in January 2022 providing detailed scenarios, developed with six Canadian financial institutions (banks and insurers), that examined the implications for the Canadian financial sector of climate change and the transition to an economy with much lower GHG emissions. As stated in the report, “The climate transition scenarios are not meant to be forecasts or comprehensive. Rather, they explore different plausible but intentionally adverse transition pathways consistent with achieving specific climate targets….They are consistent with global commitments of limiting global warming to below 2˚C.”

With these adverse scenarios as a backdrop, this E-Brief considers the alternatives for managing climate risk for Canadian banks and the financial system as a whole. We ask whether more capital buffers are needed in a country where capital ratios are already well above the regulatory floor, or whether other approaches are more appropriate. While capital buffers are critical in smoothing out negative economic shocks, they raise the cost of funding for banks, which must rely more on capital than debt to fund their risk exposures. Related costs are then passed on to borrowers, which may reduce demand for credit or affect a bank’s risk appetite. Adding capital to manage climate risk comes at a cost.

This E-Brief makes two recommendations. First, any consideration of additional capital surcharges should involve Canadian authorities working with international peers through the the Basel Committee on Banking Supervision to agree on how best to incorporate climate risks. Second, improving climate risk assessment and disclosure can help mitigate the need for further capital surcharges.

Climate Risk

Climate risk comes in multiple forms. First, there is physical risk and related financial exposure from the increasing frequency and severity of extreme weather events. These events include hurricanes, tornadoes, overland floods, sea surge, forest fires, extreme wind and precipitation, and rapid temperature variation. Climate change presents a physical risk to living things, natural assets and property affected by these events. There is also a related risk to financial institutions that provide life insurance, property and casualty insurance, and mortgage financing.

A second risk is related to financial exposure as policymakers and the market require the economy to transition toward an eventual net-zero emissions footprint. That transition has already begun in Canada and will continue for decades to come. The climate transition will touch upon all aspects of the economy and financial system, with a particular focus on sectors and activities with high GHG emissions intensity – oil and gas, transportation, heavy industry (like cement and steel), and buildings. Seventy-five percent of Canada’s GHG emissions come from these four sectors. Sectors that are negatively affected by the climate transition face an enhanced risk of lower net income and declining asset values, with related implications for financial institutions. Climate transition risk is widely spread across the economy and it will affect most aspects of financial intermediation in some manner. Assessing and managing the climate transition is therefore attracting much more attention from governments, central banks and financial regulators in Canada and globally.

A third risk to be anticipated is policy instability. In Canada, successive governments have announced numerous climate policy initiatives that have either not been fully implemented or have been altered or dropped by a subsequent government. Placing a big bet on an innovative lower-emissions technology or system could turn out badly if there were to be a shift in the expected policy environment.

The Role of Bank Capital

For banks, capital is the cushion between a bank’s assets and its liabilities that protects creditors to the bank, including depositors, from loss if the bank encounters extreme stress. For insurers, capital plus business assets (premiums plus investment income) must exceed the present value of potential future liabilities (or claims) if an insurance company is to remain viable. While OSFI oversees both federally regulated banks and insurers (as well as some pension funds and credit unions), this E-Brief focuses on bank capital. That said, the principles of climate risk and the consequential institutional and systemic risk would equally apply to insurance underwriting and investment management.

Shareholder capital invested in an individual bank’s balance sheet is a financial buffer intended to protect the bank’s depositors and other creditors against unexpected losses and uncertainty. By comparison, provisions are a portion of bank income set aside in a bank’s income statement to cover the estimated expected losses over the life of specific at-risk exposures.

If a number of significant borrowers are suddenly unable to repay their loans beyond what was provisioned for (due for example to a shock event, or an under-assessment of a structural risk), or if the bank’s investments sharply fall in value, a bank could experience financial loss – and could even go bankrupt without a significant capital cushion. With a solid capital base, it will be able to use the capital to absorb the loss and continue to operate and serve its customers (ECB 2019).

Bank capital is also, de facto, a buffer against systemic risk for the financial system as a whole, reducing the potential need for exceptional intervention by the bank regulator, central bank, and its overseeing government.

A priori, climate change represents an added layer of risk that could warrant adding capital to a bank’s balance sheet, unless that risk is properly identified, assessed, managed, and reflected in a bank’s accounting, expected-loss estimations, and existing capital base.

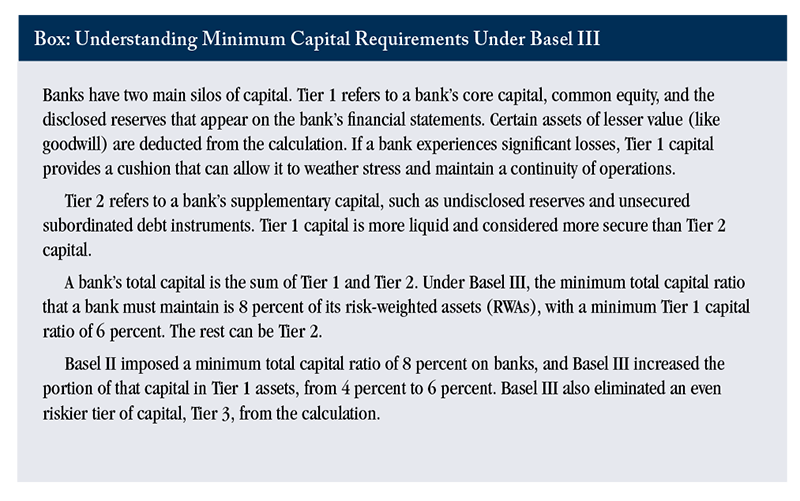

Basel III Pillars

The level of capital that banks globally are expected to hold has been defined through a series of agreements among major bank regulators, with the aim of creating a sufficient standard for capital adequacy to reduce the need for future bailouts by governments, while maintaining a competitive level playing field. Understanding the evolution of these Basel agreements is useful when assessing whether Canadian banks should hold more capital to address climate-related financial risk.

The first agreement, called Basel I, was finalized in 1988 and implemented to some degree in G10 countries by 1992. It developed a methodology for assessing banks’ credit risk based on risk-weighted assets (the riskier the asset, the more capital a bank must hold). It also indicated minimum capital requirements to keep banks solvent during times of financial stress. Basel I was followed by Basel II in 2004, which was still in the process of being implemented when the 2008 global financial crisis hit.

A third accord, Basel III, attempted to correct the miscalculation of risk that contributed to the 2008 financial crisis. Banks were required to hold higher percentages of their assets in more liquid forms, and to fund themselves more with equity, with less reliance on debt (CFI Basel III). OSFI released its initial Basel III capital rules for Canadian banks a decade ago; the most recent revisions were released on January 31, 2022. These new regulations will take effect in 2023 and 2024 (OSFI 2022). Full implementation of Basel III globally is still ongoing.

Basel III is based on three “pillars” building on experience with Basel I and II.

Pillar 1 – Capital Adequacy Requirements: Pillar 1 requires banks to maintain a minimum capital adequacy requirement of 8 percent of its risk-weighted assets. Specific capital buffers for capital conservation, countercyclical forces and systemic impacts were added as part of raising the minimum capital ratio. Basel III provides banks with additional guidance on calculating capital requirements based on credit risk and each type of asset’s risk profile. Basel III also considers operational and market risks in the calculations, in addition to credit risks.

Banks are permitted to use an internal ratings-based approach (i.e., use their own risk parameter assessments) to calculate regulatory capital, with the supervisor’s approval, should they be engaged in more complex operations with more developed risk-management systems. This would include large Canadian banks.

Pillar 2 – Enhanced Supervisory Review Process for Firm-wide Risk Management and Capital Planning: “Supervisory Review” was initially added as Pillar 2 under Basel II, to reflect the need for effective supervision of a bank’s internal capital adequacy. Banks were expected to assess their internal capital adequacy for covering all weighted risks they can potentially face in their operations. Financial regulators are responsible for determining whether a bank is using appropriate assessment approaches and covers all associated risks (CFI, Basel II).

Pillar 2 has been enhanced under Basel III to address: firm-wide governance and risk management; off-balance sheet exposures and securitization activities; managing risk concentrations; and incentives for banks to better manage risk and returns over the long term. Pillar 2 also expects sound compensation practices, valuation practices, stress testing, accounting standards for financial instruments, corporate governance, and supervisory colleges (BIS website).

We understand that in practice, at least in Canada and USA, supervisors generally do not formally use Pillar 2 because any such requirements would likely have to be disclosed under securities law. Instead, supervisors work closely with banks to ensure that each bank’s capital plans and practices “voluntarily” encompass risks that are not well captured under the Pillar 1 framework.

Pillar 3 – Enhanced Risk Disclosure and Market Discipline: “Market Discipline” was also added under Basel II, as Pillar 3. It aimed to ensure market discipline by making it mandatory to disclose relevant market information. Investors and analysts should receive the relevant information required to make informed investment decisions -- such as information related to climate risk stemming from a bank’s business activities (CFI Basel II).

Pillar 3 disclosure requirements have been enhanced under Basel III in order to highlight securitization exposures and sponsorship of off-balance sheet vehicles. Enhanced detailed disclosures are expected on the components of regulatory capital and their reconciliation to the reported accounts, with a comprehensive explanation of how a bank calculates its regulatory capital ratios (BIS).

We note that the Financial Stability Board is now developing guidelines on banks’ climate risk disclosures, which regulators will most likely expect banks to use.

Bank of Canada-OSFI Climate Scenarios

To better understand and anticipate the impact of climate risk on the Canadian financial sector, the Bank of Canada and OSFI undertook, in 2021, a climate scenario pilot in collaboration with six Canadian federally regulated financial institutions.

A set of Canada-relevant climate transition scenarios were therefore developed that explored pathways consistent with achieving certain climate targets. The scenarios vary in terms of two key drivers of climate transition risk: (i) the ambition and timing of climate policy, and (ii) the pace of technological change and availability of advanced technologies (Bank of Canada 2022, p. ii). The scenarios use conservative assumptions for technological change by not relying heavily on technologies that are not yet commercially available and/or could face scalability issues (Bank of Canada and OSFI 2022, p.10).

The scenarios describe a number of potential material risks to the economy and the financial system stemming from the climate transition. Important sectoral restructuring in the Canadian and global economies can be expected in order to meet climate targets. While every sector contributes to the transition, the oil and gas sector is front and centre. Refined oil products, the oil and gas sector as a whole, as well as the crops sector, have the highest probabilities of default and the most significant income loss under the various scenarios, due to a combination of policy developments and market responses.

The scenarios highlight the risks of significant macroeconomic impacts in a commodity-exporting country like Canada, notably the risk of declines in commodity prices and demand due to global climate policy changes. The scenarios also highlight that delaying climate policy action increases the overall economic impacts and risks to financial stability (Bank of Canada and Office of the Superintendent of Financial Institutions 2022).

As part of the Bank-OSFI research, a survey was also conducted on financial institutions’ current governance and risk-management practices around climate-related risks and opportunities. It found Canadian financial institutions (like those in many other nations) were generally at an early stage of building climate-related risk assessment capabilities for transition risks, including both gathering appropriate data and the use of climate-scenario analysis.

Managing Bank Climate Risk: Necessary vs. Sufficient Conditions

OSFI is developing an operating framework for managing the climate transition and related risk that will ultimately be anchored to Basel III and its three pillars. OSFI has issued an initial draft guideline on climate risk management for federally regulated financial institutions, and is seeking comment from stakeholders before issuing a revised version in early 2023. The initial draft guideline outlines OSFI’s risk management expectations on climate-related physical and transition financial risks faced by banks and insurers, with the aim of achieving five desirable prudential outcomes:

1. Awareness: climate-related financial risks and their impact are understood throughout the institution.

2. Governance and strategy: Climate-related financial risks are embedded in the financial institution’s overall strategy and risk appetite and integrated into the risk governance regime.

3. Risk management: Material climate-related financial risks are integrated into the institution’s enterprise risk management processes and managed accordingly.

4. Financial resilience: The bank remains adequately capitalized and liquid through severe yet plausible climate-risk scenarios over extended time horizons.

5. Operational resilience. The institution continues to deliver critical operations through any disruption due to climate-related disasters (OSFI 2022).

A central issue is what would represent sufficient conditions for managing climate risk under Basel III. Implementation of Pillars 2 and 3 are certainly necessary conditions. Under Pillar 2, OSFI will determine whether a given bank is using appropriate risk assessment approaches and is covering all associated risks, including climate risks. Under Pillar 3, OSFI will assess the adequacy of the climate-related information being required and shared by banks, and how that information is being used in the capital adequacy calculations, to allow the market to make informed investment decisions.

Sufficiency may require drilling down deeper. There is now a rapid if uneven evolution globally toward adoption of the disclosure guidelines proposed by the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD), with momentum building toward mandatory adoption. The TCFD final report provided four broad recommendations and offered advice on specific areas of disclosure, which is particularly germane for financial institutions that extend credit to firms across the economy.

1. Governance: An organization’s governance around climate-related risks and opportunities; i.e., the role of the board and management.

2. Strategy: The actual and potential impacts of climate-related risks and opportunities on an organization’s businesses, strategy, and financial planning where such information is material.

3. Risk Management: How an organization identifies, assesses, and manages climate-related risks.

4. Metrics and Targets: The metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material, notably Scope 1 (direct), Scope 2 (indirect or energy used), and, if appropriate, Scope 3 (supply chain) greenhouse gas (GHG) emissions; related risks; and performance targets (TCFD 2021).

To implement the TCFD recommendations, banks will need to obtain more standardized and detailed information from their clients on the business and projects being financed and how the business and related climate impacts will evolve over time. The term “financed emissions” is now being used for GHG emissions associated with financial institutions’ lending, investing, and insurance underwriting, which reportedly can be 700 times larger than operational emissions from the financial sector itself (Canadian Climate Institute 2021). Reporting on financed emissions is currently voluntary, but it is foreseeable that it may eventually become a mandatory regulatory requirement.

Establishing a common standard among banks on client information related to climate risk is certainly desirable; it would define expectations, promote operating efficiency, and maintain a competitive level playing field among banks. To that end, a global-financial-industry-led group called the Partnership for Carbon Accounting Financials (PCAF) published a global greenhouse gas emissions accounting and reporting standard in late 2020, which is now being considered, and even gaining adoption, within the financial industry (PCAF 2020). This standard provides detailed methodological guidance for six asset classes: listed equity and corporate bonds; business loans and unlisted equity; project finance; commercial real estate; mortgages; and motor vehicle loans.

Finally, in addition to managing climate risk by meeting the necessary conditions under Pillars 2 and 3, banks could reduce climate risk by helping to finance their clients’ own efforts to reduce GHG emissions and climate risk in their activities, for example by financing carbon capture and energy use transition initiatives. Banks also have the option of taking action to reduce the climate-risk weighting of their assets. Shifting the composition of Canadian bank portfolios towards client assets and activities with a lower or declining emissions pathway would help limit a bank’s financed emissions and associated risk and thereby reduce any need for additional capital.

Capital: The Ultimate Backstop

OSFI recently set out its initial expectations on climate-related financial risk management and transparency. It is obviously focused on managing the risks to bank stakeholders like depositors, creditors and investors, and limiting systemic risk to the Canadian financial system and economy.

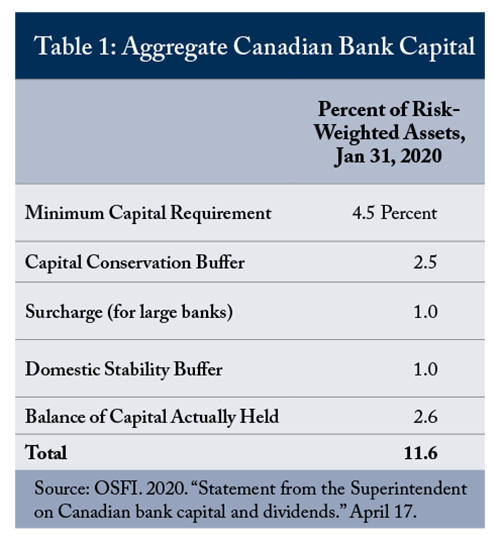

Under the current regulatory structure, to help foster bank solvency, multiple layers of capital protection have been added to banks’ balance sheets that limit the potential need for exceptional policy intervention. OSFI’s capital regime for banks includes: a minimum capital requirement; a capital conservation buffer; a systemic surcharge for large banks; and a domestic stability buffer. The domestic stability buffer was initially set at 2.25 percent of weighted assets. It has since been reduced to 1.0 percent but remains one the largest counter-cyclical buffers set anywhere by prudential regulators, in view of Canada’s relatively high household indebtedness

(OSFI 2020).

There is thus an expectation that Canadian banks will hold capital well in excess on the Basel III Pillar 1 standard of 8 percent of risk-weighted assets.

To help build public confidence during the early stages of the 2020 COVID pandemic, OSFI publicly reported aggregate actual Canadian bank capital levels at 11.6 percent of risk-weighted assets, as shown in Table 1.

The key question with respect to climate risk is whether, at this stage, banks have taken it explicitly into account in their capital plans, and whether additional capital would be beneficial in managing this risk, which interacts with numerous other risks for which capital is required. The challenge is that measurement of climate risk is in its infancy and there is a fair amount of uncertainty and judgement required to impose prudential requirements. That reality means it is likely too soon to consider a Pillar 1 requirement imposing a uniform climate-risk calculation on all banks.

Climate change is a global issue, so it would make sense to first develop a common international approach or methodology for addressing climate risk under Pillar 1. Canadian authorities could work with international partners within the Basel process to determine how best to address climate risk across the global banking system, which is the best way to ensure comprehensive global treatment of climate risk while maintaining a level playing field competitively.

Canadian banks’ climate-risk management practices and transparency can also be advanced under Pillars 2 and 3, with a focus on the concept of financed emissions. Establishing a common risk measurement and disclosure framework, as proposed by OSFI, would help to determine how best to factor climate risk into the capital plans of Canadian banks.

Conclusions and Recommendations

OSFI has established a Basel III-consistent capitalization standard under which Canadian banks already hold high levels of capital that go well beyond the Pillar 1 floor. Climate risk is another factor that is now being formally considered as part of Basel III implementation in Canada and elsewhere. To that end, OSFI is developing an operating framework for managing the climate transition and related risk.

Climate change is a global issue, and consideration of requiring banks to hold additional capital should involve Canadian authorities working with international counterparts by using the Basel process to agree on how climate risks should be incorporated.

That said, the capital base methodology in place for the Canadian banking system provides a strong solvency buffer against all risks -- and creates room for considering alternative means of ensuring that bank climate risk is being managed adequately, rather than simply requiring more capital.

Consistent with Pillars 2 and 3, OSFI is right to expect a rigorous approach to climate-risk assessment, and thorough disclosure, on the part of Canadian banks under the guideline now being proposed. Such a rigorous approach would help reduce the need for further capital surcharges under Pillar 1. To that end, banks can develop and adopt sophisticated climate-risk assessment and management systems, and robust disclosure and transparency practices. Making use of the greenhouse gas emissions accounting and reporting standard developed by the Partnership for Carbon Accounting Financials, based on the concept of financed emissions, would be a concrete way to strengthen climate-risk disclosure.

References

Bank for International Settlements (BIS). “Basel II: Revised international capital framework.” Available on website at: https://www.bis.org/publ/bcbsca.htm

_____________. 2017. “Basel Committee on Banking Supervision – Basel III” (summary chart). Available at: https://www.bis.org/bcbs/publ/d424_hlsummary.pdf

_____________. 2022. Basel III Monitoring Report. February. Available at: https://www.bis.org/bcbs/publ/d531.htm

Bank of Canada. 2022. “Transition Scenarios for Analyzing Climate-Related Financial Risk.” Staff Discussion Paper 2022-1. Available at: https://www.bankofcanada.ca/2022/01/staff-discussion-paper-2022-1/

Bank of Canada and Office of the Superintendent of Financial Institutions. 2022. “Using Scenario Analysis to Assess Climate Transition Risk.” January. Available at: https://www.bankofcanada.ca/wp-content/uploads/2021/11/BoC-OSFI-Using-Scenario-Analysis-to-Assess-Climate-Transition-Risk.pdf

Canadian Climate Institute. 2021. “Sink or Swim: Transforming Canada’s Economy for a Global Low-carbon Future.” October.

Corporate Finance Institute (CFI). 2020. “Basel II.” Updated Feb. 26, 2022. Available at:

https://corporatefinanceinstitute.com/resources/knowledge/finance/basel-ii/

_____________. 2020a. “Basel III.” Available at: https://corporatefinanceinstitute.com/resources/knowledge/finance/basel-iii/

European Central Bank (ECB). 2019. “Why do banks need to hold capital?” May. Available at:

www.bankingsupervision.europa.eu

Hood, Joe. 2022.“What you need to know about OSFI’s new proposed climate-risk guidelines for financial institutions.” Financial Post. May 26.

Office of the Superintendent of Financial Institutions (OSFI). 2020. “Statement from the Superintendent on Canadian bank capital and dividends.” April 17.

_____________. 2022a. “Building Federally Regulated Financial Institution Awareness and Capability to Manage Climate-Related Financial Risks.” January.

_____________. 2022b. “OSFI completes Basel III reforms, releases final capital and liquidity rules to protect Canadians.” News release, Jan 31.

Partnership for Carbon Accounting Financials (PCAF). 2020. “Global GHG Accounting and Reporting Standard for the Financial Industry.”

Scotiabank. 2022. “Scotiabank’s Net-Zero Pathways Report.”

Task Force on Climate-related Financial Disclosures (TCFD). 2017. “Recommendations of the Task Force on Climate-related Financial Disclosures.” June.