The Study in Brief

- The federal government’s massive spending and borrowing during the COVID-19 pandemic has desensitized Canadians to fiscal excess.

- The government has promised costly new programs without revenue to cover them or measures to boost economic growth and the tax base. This Shadow Federal Budget for 2022 changes course, focusing on growth and ensuring Canadians have the fiscal resources they will need for post-pandemic challenges.

Introduction

Since the COVID-19 pandemic hit in early 2020, Canadian federal fiscal policy has largely prioritized mitigating its economic damage through support to individuals and businesses. However impressive the speed with which it was delivered, the scale and duration of COVID-related spending have exceeded the requirements of the emergency. The government has also added or promised major programs not related to the pandemic. Elected representatives and many Canadians have become too used to announcements of tens or even hundreds of billions of dollars of new commitments.

Such spending, unmatched by new revenue, is reducing Canada’s capacity to address the many economic challenges it faces. The 2022 federal budget should change course. Federal fiscal policy should emphasize growth and fiscal sustainability.

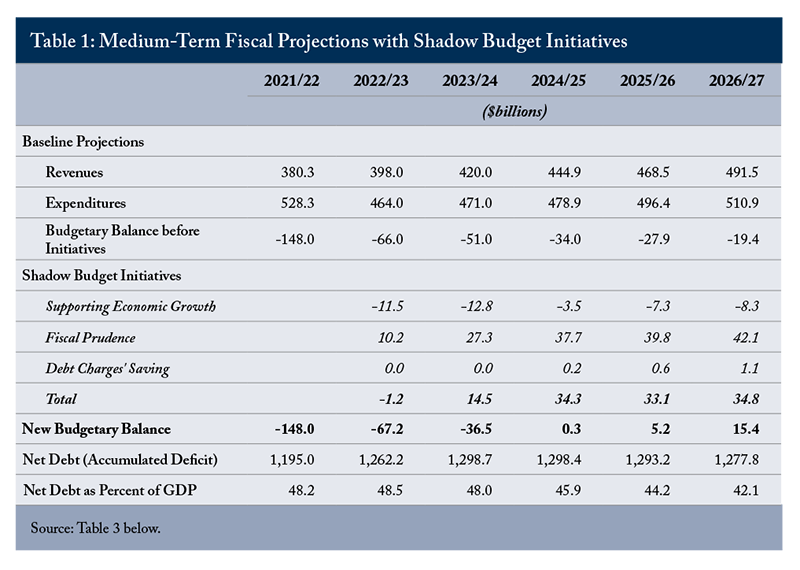

This Shadow Budget also breaks with the past in putting the government’s financial position and projections for revenues and expenses, deficits and net debt front and centre – on this page. Recent federal budgets have buried key numbers in annexes after hundreds of pages of repetition and political messaging. To give these numbers the prominence they deserve, Table 1 presents our outlook based on the government’s Fall Economic and Fiscal Update (Fall Update) and our own judgment, the projected impact of this Shadow Budget’s measures and the resulting new trajectories for the bottom line and the federal government’s accumulated deficit.

Our Shadow Budget would ensure a sustainable path for federal and national finances. The ratio of net debt to gross domestic product (GDP) would decline immediately, and deficits would end by fiscal year 2024/25. The combination of growth-enhancing and fiscally prudent policies would redress the damage COVID has done to federal fiscal capacity, and provide more resources Canadians will need to address an aging population, climate change and the energy transition, subsequent pandemics, and challenges we do not yet foresee.

The Fiscal Framework

A Commitment to Transparency and Accountability

Reflecting the government’s commitment to presenting spending estimates that match budget projections, the fiscal year 2022/23 Main Estimates accompanying this Shadow Budget follow Public Sector Accounting Standards, and will appear before the start of that fiscal year, after appropriate vetting by the Treasury Board. The 2023/24 Main Estimates will appear by mid-February of that year, simultaneously with the 2023 federal budget.

This Shadow Budget also breaks with the recent past in being transparent about figures and assumptions. It lays out the assumptions underlying its economic and fiscal projections.

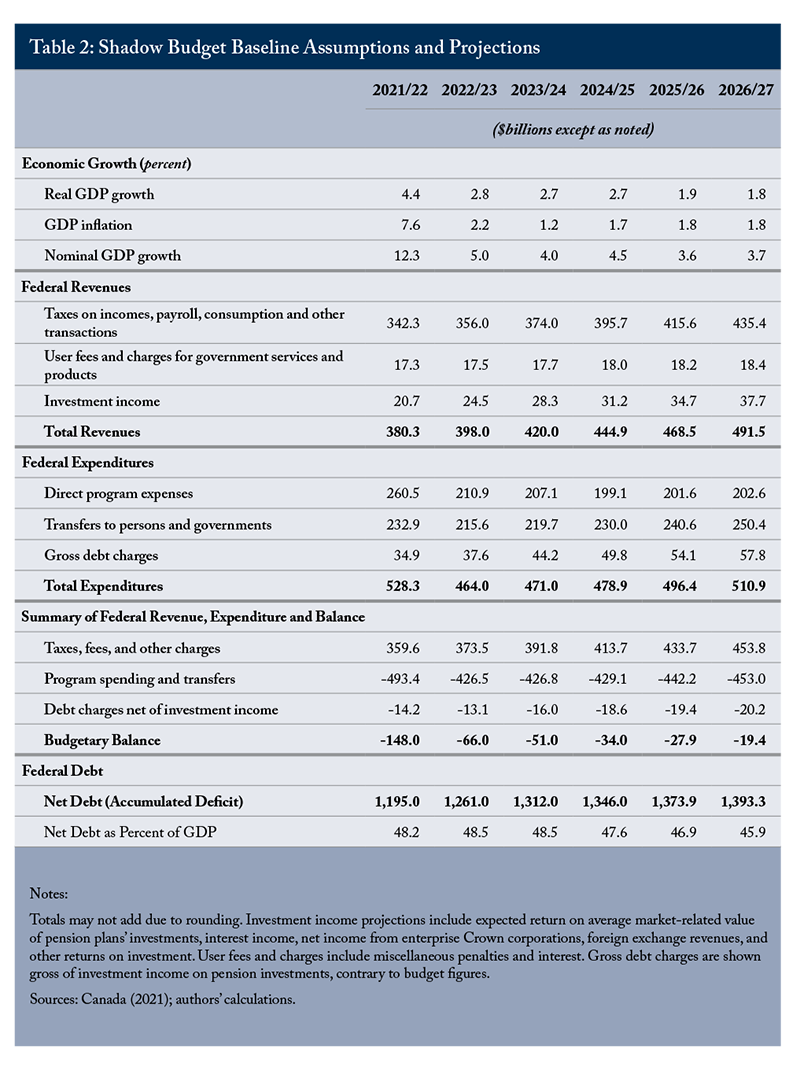

The Fall Update (Canada 2021) presents two economic scenarios in addition to its main outlook (Canada 2021). The baseline for our fiscal plan is the slower recovery alternative.

The Update’s main outlook, based on private forecasts, projected higher nominal GDP than expected in the 2021 budget: an average of $87 billion per year over the five-year forecast horizon. The resulting boost to revenue would have lowered Ottawa’s accumulated deficit by some $91 billion by 2025/26 – if actions in the Update and since the 2021 budget had not absorbed about two-thirds of it. In contrast, the slower-recovery scenario, involving more prolonged supply chain bottlenecks and a more severe effect of the Omicron variant of the COVID virus, projects nominal GDP up by less: an average of $50 billion per year over the budget horizon, while the deficit would be about $6 billion higher on average.

The Shadow Budget’s planning baseline starts with a $148 billion deficit in fiscal year 2021/22, deficits of $66 billion in 2022/23 and $51 billion in 2023/24, and continued borrowing through the end of the projection period (Table 2). The federal debt-to-GDP ratio would decline only marginally, from 48 percent of GDP to 46 percent in 2026/27.

The Importance of Economic Growth

The 2021 federal budget and Fall Update were missed opportunities to engage Canadians in a discussion about the economic and fiscal challenges facing the country.

The challenges are many. COVID will continue to cause economic harm and require fiscal supports. Higher interest rates are needed to rein in inflation and discourage debt accumulation. That shift will be jarring. Until the Bank of Canada’s recent increase in its policy rate to 0.50 percent, the question of when the Bank would move the rate up from its emergency level of 0.25 percent overshadowed the implications of its returning to more normal levels. The Bank has said a more normal level for the policy rate would be between 1.75 and 2.75 percent, and recent higher-than-expected inflation may mean a rate higher than that. Debt is high everywhere: among households, businesses and governments. The higher the debt goes while interest rates are low, the greater the risk of instability when interest rates increase.

Climate change poses a twofold risk to the fiscal outlook. First, notwithstanding the federal government’s insistence on the existential threat of global warming, more frequent and costly natural disasters do not figure in its projections. The 2021 budget presented no downside long-term scenarios. Instead, it presented two upside scenarios, adding 0.2 and 0.4 of a percentage point of annual real growth to Finance Canada’s previous projection. Second, actions to mitigate climate change will mean economic disruption. Canada’s economy is carbon intensive: simply replacing fossil fuels in transportation and home heating will involve massive expenditures with no concomitant increase in households’ current living standards and a potential decline in the tax base.

Canada’s aging population is also a twofold risk: it will slow growth of the economy and government revenue, and it will put upward pressure on public spending. Higher seniors’ benefits are a direct federal responsibility, and although the bigger challenge of healthcare costs is a direct provincial/territorial responsibility, the federal government has promised a bigger Canada Health Transfer and a new transfer for mental health, so the pressure will affect both levels.

The rise of global protectionism is another risk to economic growth. For decades, policy in Canada has emphasized lowering international trade barriers. That strategy made sense for a small, open economy such as Canada’s, particularly when much of the rest of the world was doing the same. But global supply chains now look more vulnerable and protectionism is in vogue, including in Canada’s most important trading partner, the United States.

Reducing the downside risks requires bolstering growth.

Business investment per person in Canada’s labour force has been declining relative to such investment in the United States and other developed countries since the middle of the past decade (Robson and Wu 2021). Canadians need measures to foster jobs, investment and productivity growth to ensure future prosperity and underwrite the tax revenues that will support federal programs and a return to a sustainable fiscal position.

The Importance of Lowering the Debt Ratio

Laurin and Drummond (2021) project that, with a 1.5 percent average real GDP growth rate, a gradual rise in interest rates and modest new spending, the net debt-to-GDP ratio could rise to around 60 percent by mid-century, rather than by the 30-40 percent range presented in the 2021 budget. A ratio around 60 percent would raise risks itself, especially if interest rates are higher, and would mean less flexibility to respond to crises. Younger and future generations of Canadians will need to mitigate and adapt to climate change, population aging and other challenges yet unknown. An indispensable asset for them will be a federal government with the restored capacity to deliver services sustainably.

A key sign of that restored capacity would be a federal debt-to-GDP ratio of around 30 percent – the level that permitted robust responses to the 2008/09 financial crisis and the COVID-19 pandemic. And that level should be reached over a foreseeable horizon, not decades from now. As John Lester notes in a recent C.D. Howe Institute report, “Generations not yet born receive little or no benefit from cushioning the downturn but will pay a cost as long as the debt is rolled over. The increase in debt should therefore be paid down before the next generation starts working and paying taxes” (Lester 2021). A fiscal path with a persistently higher debt ratio puts the burden of the income supports triggered by the pandemic, not on the cohort that benefited, but on future cohorts. This burden would be in addition to the pre-existing fiscal liability future generations face due to population aging and the escalating costs of healthcare (Mahboubi 2019) – when young Canadians’ education and early work experience have already suffered from the pandemic.

Notwithstanding the debt ratio’s value as an indicator of fiscal health and sustainability, experience has taught – a lesson reinforced as recently as the second half of the past decade – that it is not an effective constraint year by year. The debt ratio sanctions ongoing borrowing, relieving spending advocates of the need to justify their proposals against alternative programs or required taxes, and it sanctions ongoing deterioration in the federal government’s net worth, a key indicator of its capacity to deliver services. A debt ratio fiscal constraint also turns out to be asymmetrical: when the economy booms, it allows larger deficits; when the economy slumps, the government abandons it.

Moreover, focusing on the debt ratio appears to promote wishful thinking – notably, projections in which interest rates are forever lower than growth rates. The roots of Canada’s problems in the 1990s were the deficits the federal government started running in the 1970s, when the average interest rate on new federal borrowing was lower than GDP growth. New programs looked cheap relative to taxes paid until the 1980s, when that differential reversed, the debt ratio rose and interest payments grew as a share of the federal budget. The Mulroney and Chrétien governments had to raise taxes and cut spending by multiple GDP points: between fiscal years 1987/88 and 2007/08, Canadians on average paid 16.8 percent of GDP in federal taxes and received programs valued at only 13.9 percent of GDP. This Shadow Budget would produce a surplus by fiscal year 2024/25, protecting Canadians from a repeat of that painful episode.

To set the stage for the measures that follow, we emphasize that the federal government should scrutinize potential new spending more rigorously than in the past. It recently raised Old Age Security (OAS) payments, benefiting a group that has a lower poverty rate than non-seniors. It is supporting childcare programs irrespective of need. COVID-related deaths in long-term care are prompting flows of more resources into institutions, rather than into home care and community-based living. The past provides key lessons, such as the 2006 boost in the Canada Health Transfer, which appears to have increased costs rather than improved services. Higher transfers to the provinces do not guarantee better service to Canadians.

When new spending is justified, this Shadow Budget does not pass the bill to future generations. They will have their own challenges to face – challenges current Canadians have helped create. It would be fairer to pay for new spending and debt reduction with new revenue – either by increasing the Goods and Services Tax (GST), as proposed in this Shadow Budget, or by using additional proceeds from the carbon tax, which is due to rise steeply. Although a resurgence of the pandemic might justify delaying a return to surplus, the logic of intergenerational fairness holds: any increase in borrowing relative to this fiscal plan should be small enough to ensure that the debt ratio continues to fall.

Supporting Economic Growth

The Canadian economy is not suffering from any deficiency of demand that could be addressed by more transfer payments and consumption spending by governments. An inflation rate of around 5 percent is a convincing indicator that demand is outstripping supply. Therefore, the primary focus of the economic program in this Shadow Budget is on boosting the labour force and labour force participation, increasing business investment and raising productivity.

Address Pressure on EI Premiums

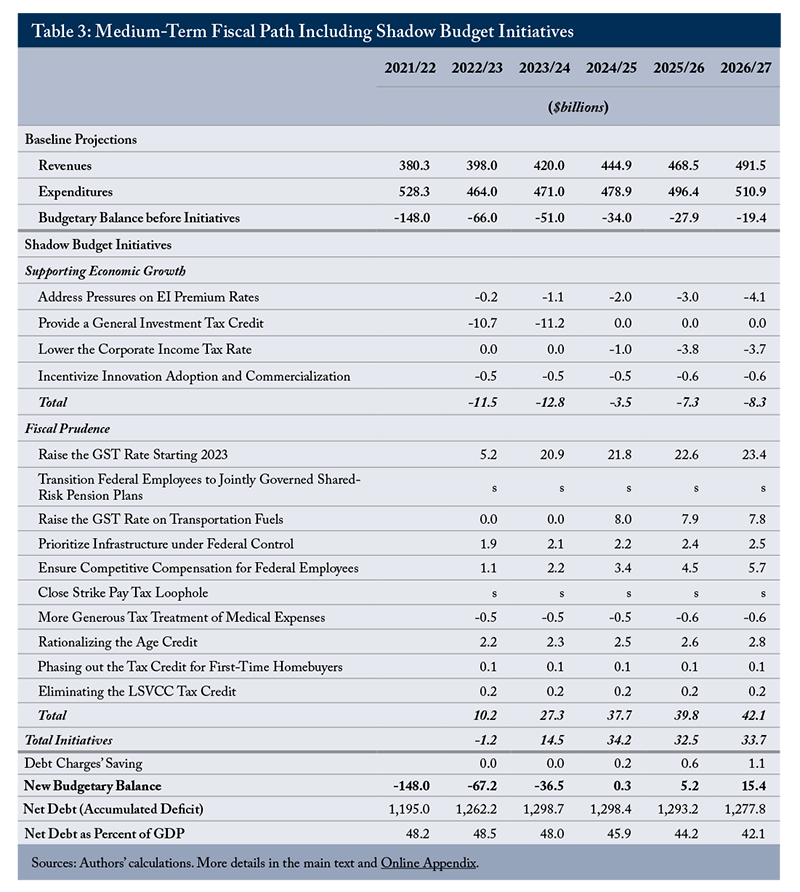

Employment Insurance (EI) contribution rates are set to make the EI operating account’s cumulative balance break even over a seven-year period. In the fall of 2020, the government froze 2021 and 2022 EI premiums at their 2020 level. At the end of 2022, the account is projected to show a $30 billion deficit, to be repaid over the next seven years. This will require EI employee-paid premium rates to increase from their 2022 level of $1.58 per $100 of insurable earnings to $1.83 in 2027 on the employee side, with employer-paid premiums being 1.4 times this amount. To prevent those hikes, this Shadow Budget would credit the EI operating account to cover the annual cost of the further freezing of contribution rates over the projection period. Since premium hikes required by law are already planned in the fiscal framework, this crediting would be expensed annually over the projection period as the premium shortfall adds to the annual deficit.

Provide a General Investment Tax Credit

Canada’s stock of machinery and equipment and intellectual property (IP) products has been growing more slowly than the labour force for years (Robson and Wu 2021), undermining productivity and wages, and causing forecasters, including the Bank of Canada, to mark down their growth projections. This Shadow Budget would implement a temporary general investment tax credit, applying to all investments in depreciable assets, including intangibles, at a rate of 5 percent. It would come into effect on April 1, 2022, and run until April 1, 2024. Its temporary nature would encourage early investment and its neutrality means managers themselves would decide on what types of capital they need and what types of activities they pursue. Its net cost over the projection period would be some $22 billion.

Lower the Corporate Income Tax Rate

Canada is losing its competitive edge in business taxation, notably against the United States (Bazel and Mintz 2017; McKenzie and Smart 2019). Newly proposed rules to limit the amount of interest costs deductible by large firms would exacerbate this problem. This Shadow Budget takes a different tack. It would reduce the corporate income tax rate by two percentage points, from 15 percent to 13 percent, starting in 2025, after the impact of the temporary investment tax credit outlined in the previous section has faded.

Incentivize Innovation, Adoption and Commercialization

This Shadow Budget would establish an “IP Box” tax mechanism whereby income from patents and other intellectual property generated by activity in Canada would face a lower corporate tax rate. This special rate would encourage businesses to pursue commercialization of innovation in Canada (Pantaleo, Poschmann, and Wilkie 2013; Parsons 2011). It would also discourage the shifting of highly mobile IP income to lower-tax jurisdictions. Aiming to arrive at a combined federal/provincial IP Box special rate corresponding to the tentative global minimum rate of 15 percent could contain the fiscal cost of the IP Box without engendering harmful tax competition (Lester, forthcoming). Its initial cost to federal revenues would be around $500 million annually.

Fiscal Prudence

Ensuring that the budget returns to balance and that federal debt grows more slowly than the economy will require important adjustments to major tax and spending programs.

Raise the GST Rate in 2023

Consumption taxes such as the GST harm investment and growth less than do taxes on capital and personal income and are more stable and reliable revenue sources (Dahlby and Ferede 2011). To reiterate, a key motive underlying this Shadow Budget is ensuring that Canadians who benefited from the massive pandemic-related federal spending should help pay for it. That means higher taxes. Higher corporate income taxes would be counterproductive and higher personal income taxes would drive out the talent and wealth we need to move from recovery to expansion. This Shadow Budget would therefore raise the GST rate by two percentage points in 2023, restoring the rate to its level before July 2006.

Transition Federal Employees to Jointly Governed Shared-Risk Pension Plans

This Shadow Budget would initiate a transition of federal employees’ pension plans – notably including the plans for federal members of Parliament – to shared-risk plans in which taxpayers bear less cost and risk, and a joint governance structure gives employees a voice in the long-term sustainability of the plans. This change would have no fiscal cost, but over time it would reduce the fluctuations that appear in the “below the line” adjustment in federal financial statements and resulting unbudgeted changes in federal debt.

Raise the GST Rate on Transportation Fuels

The federal government has committed to increase the carbon tax from the $50 per tonne planned for 2022 to $170 by 2030. In the meantime, an increase in the GST rate applied to transportation fuels would reduce carbon dioxide emissions and bolster federal finances. This Shadow Budget would increase the GST on transportation fuels by ten percentage points, starting in fiscal year 2024/25, by which time we anticipate recent surges in energy prices to have receded. This measure would generate about $8 billion initially, and less later as demand adjusts.

Prioritize Infrastructure under Federal Control

This Shadow Budget would prioritize funding for infrastructure projects under direct federal control, such as investments in capacity and added security for marine, rail, air transportation and military assets. The second phase of the Invest in Canada Plan, which began in fiscal year 2018/19, envisioned about $7.9 billion in grants for provincial and local projects in 2022/23, rising to an extraordinary $11 billion in 2027/28. This Shadow Budget would replace about one-quarter of these amounts with direct federal investments, and thus amortized over a long period, reducing annual planned expenses over the budget horizon by around $2.2 billion.

Ensure Competitive Compensation for Federal Employees

This Shadow Budget would freeze federal departmental operating budgets for wages and salaries at their 2021 levels for five years. Managers would have greater latitude within their budgets to reward high performers and reduce less valuable positions. This approach could achieve a better balance between federal public and private sector compensation (Lahey 2011). The freeze would reduce federal spending by at least $1 billion in fiscal year 2022/23, growing to $5.7 billion in the last fiscal year.

Close the Strike Pay Tax Loophole

An anomalous feature of Canada’s tax system allows some income to escape income tax and to subsidize strikes – likely to be a bigger problem in the next few years, since high inflation fosters labour disputes. Union dues paid by employees are deductible from their taxable income; any returns on those funds invested by the unions escape tax, and amounts paid out in strike pay are not taxable. This tax-free treatment subsidizes activity that harms the Canadian economy (Alarie and Sudak 2006; Kesselman 1999). This Shadow Budget proposes that the government introduce legislation to make strike pay taxable as ordinary income. The revenue impact of the measure would be about $10 million annually.

Provide More Generous Tax Treatment of Medical Expenses

The current medical expense tax credit applies only to expenses exceeding 3 percent of net income or $2,479, whichever is lower, and is calculated at the bottom tax rate. This is inequitable. People who pay tax on income they need to cover non-discretionary costs have lower after-tax discretionary income than people without such costs – an important justification for the non-taxation of employer-paid health premiums. In view of the extra health-related costs many Canadians now face, this tax credit also looks inadequate. This Shadow Budget would lower the threshold on such expenses to 1.5 percent of net income, or $1,240, whichever is lower. This change would help people who cover medical costs directly or through health-related insurance premiums. The estimated fiscal cost of this measure is $500 million per year.

Rationalize the Age Credit

The income tax regime’s age credit is an arbitrary measure – a younger person might have needs as great as, or greater than, those of an older person with a similar income – and the looming increase to OAS for older seniors bolsters the case for rationalizing it. The increase in the medical expense tax credit in this Shadow Budget would help older Canadians who face medical expenses. This Shadow Budget would also reduce the base amount of the age credit from $7,898 to $4,000. This measure would save more than $2 billion annually.

Phase Out the Tax Credit for First-Time Homebuyers

This Shadow Budget would phase out the tax credit for first-time homebuyers. This subsidy increases house prices and induces households to take on excessive debt. Phasing it out would save about $100 million annually.

Eliminate the Tax Credit for Labour-Sponsored Venture Capital Corporations

The tax credit for labour-sponsored venture capital corporations (LSVCCs) distorts saving and investment, and is an inefficient way of spurring innovation (Fancy 2012). The Shadow Budget would eliminate the LSVCC, which would improve the federal government’s bottom line by about $200 million annually.

Tying It Up

Supporting economic growth and restoring fiscal capacity to address population aging, climate change and many other concerns are critical and complementary tasks. This Shadow Budget would address these tasks with measures that would support economic growth both immediately and in the long run and with other measures that would end the deterioration of the federal government’s capacity to provide services, ensuring that public debt is sustainable and fair for future generations.

The 2021 budget contained little to enhance Canada’s growth prospects and much to raise anxiety about mounting debt and exposure to adverse events – notably, rising interest rates (Laurin and Drummond 2021). By contrast, this Shadow Budget would spur business investment and instil confidence in Canada’s fiscal framework.

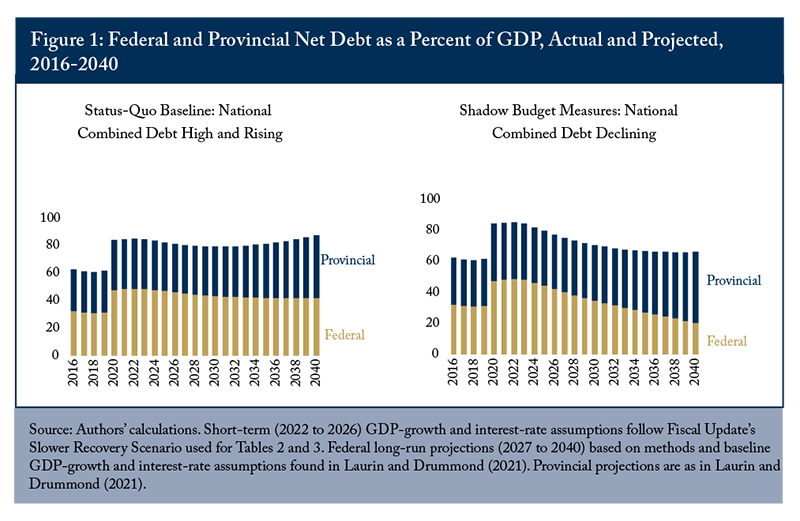

Table 3 shows the impact of the measures in this Shadow Budget out to fiscal year 2026/27. These measures would put the federal government on a path to budget balance within three years and, extrapolating past the five-year budget horizon, on a path to restore its debt-to-GDP ratio to its pre-pandemic level within twelve years (Figure 1). Rather than staying high and potentially rising, the combined federal-provincial net debt ratio would return to its pre-pandemic level, when Canada boasted relatively strong public finances. A lower debt ratio would also instil confidence in Canadian governments’ creditworthiness, limiting upward pressure on interest rates and payments. A prompt end to budget deficits would end the erosion of the federal government’s service capacity, and encourage greater discipline in fiscal decisions.

These measures alone cannot guarantee growth and fiscal stability in the long term. Avoiding counterproductive initiatives is also critical. On the growth side, the federal government has recently proposed rules to limit the deductibility from taxable income of interest paid by large firms (Canada 2022). Limits on interest deductions will generally raise the cost of capital to the firms affected, deterring investment (Mintz 2020). The proposed rules would also distort investment decisions, exacerbating an existing tilt in favour of assets that depreciate rapidly, and against assets with longer lives (Bazel and Mintz 2021). This Shadow Budget would withdraw this proposal.

As for fiscal stability, expensive initiatives recently floated by the federal government – so not yet in the fiscal framework – are a particular threat. This Shadow Budget would rescind these commitments, including the pursuit of a national pharmacare program. The enhanced medical expense deduction in the Shadow Budget would alleviate some of the pressures Canadians experience from healthcare costs. Moreover, governments could enhance drug coverage and affordability through more strategic and less costly initiatives (Wyonch and Robson 2019).

This Shadow Budget also would not introduce a basic income, loosen eligibility for EI or increase the share of earnings that EI covers. Such measures would be inconsistent with containing the growth not only of federal debt, but also of transfer payments that discourage workforce participation, which are inappropriate when demography and the lingering effects of COVID-19 remain drags on economic growth.

In its election platform, the government promised to cut Canada Mortgage and Housing Corporation mortgage insurance premiums by 25 percent. With the housing market already looking like a speculative bubble and households overextended, such a move makes no sense. It flies in the face of normal insurance principles, and would increase the exposure of taxpayers to bad debts on a massive scale. This Shadow Budget would rescind that commitment.

This Shadow Budget’s combination of growth-supporting and debt-limiting initiatives would help Canada recover from the COVID-19-induced recession, support higher living standards in the future and put federal finances back on a sustainable path. The virtuous circle of strong growth and shrinking debt burden would enable Canadians to address the challenges of population aging, climate change and the energy transition, subsequent pandemics and crises we cannot foresee. This is the federal budget Canada needs in 2022.

References

Alarie, Benjamin, and Matthew Sudak. 2006. “The Taxation of Strike Pay.” Canadian Tax Journal. (54) 2.

Bazel, Philip, and Jack Mintz. 2017. “Tax Policy Trends: Whether It Is the U.S. House or Senate Tax Cut Plan – It’s Trouble for Canadian Competitiveness.” Calgary: University of Calgary, School of Public Policy. November.

______. 2021. “The Surprising Investment Impacts from Limiting Net Interest Deductibility.” Intelligence Memo. Toronto: C.D. Howe Institute. June.

Boadway, Robin, and Thorsten Koeppl. 2021. The “Demand Stabilization Mechanism”: Using Temporary GST Cuts as Automatic Fiscal Policy. Commentary 612. Toronto: C.D. Howe Institute. November.

Boadway, Robin, and Jean-François Tremblay. 2016. Modernizing Business Taxation. Commentary 452. Toronto: C.D. Howe Institute. May.

Canada. 2021. “Economic and Fiscal Update.” Ottawa: Department of Finance. December.

______. 2022. “Legislative Proposals Relating To Income Tax Act and Other Legislation.” Ottawa: Department of Finance. February.

Dahlby, Bev, and Ergete Ferede. 2011. What Does It Cost Society to Raise a Dollar of Tax Revenue? Commentary 324. Toronto: C.D. Howe Institute. March.

Fancy, Tariq. 2012. “Can Venture Capital Foster Innovation in Canada? Yes, but Certain Types of Venture Capital Are Better than Others.” E-Brief 138. Toronto: C.D. Howe Institute. September.

Kesselman, Jonathan R. 1999. “Base Reforms and Rate Cuts for a Revitalized Personal Tax.” Canadian Tax Journal 47 (2): 210–41.

Lahey, James. 2011. “Controlling Federal Compensation Costs: Towards a Fairer and More Sustainable System.” In How Ottawa Spends, 2011-2012, ed. Christopher Stoney and G. Bruce Doern, 84–105. Montreal; Kingston, ON: McGill-Queen’s University Press.

Laurin, Alexandre, and Donald Drummond. 2021. “Rolling the Dice on Canada’s Fiscal Future.” E-Brief. Toronto: C.D. Howe Institute. July 29.

Lester, John. 2021. Who Will Pay for the Economic Lockdown? Commentary 594. Toronto: C.D. Howe Institute. March.

Lester, John. Forthcoming. “An Intellectual Property Box for Canada – Why and How?” E-Brief. Toronto: C.D. Howe Institute.

Mahboubi, Parisa. 2019. Intergenerational Fairness: Will Our Kids Live Better than We Do? Commentary 529. Toronto: C.D. Howe Institute. January.

McKenzie, Kenneth, and Michael Smart. 2019. Tax Policy Next to the Elephant: Business Tax Reform in the Wake of the US Tax Cuts and Jobs Act. Commentary 537. Toronto: C.D. Howe Institute. March.

Mintz, Jack. 2020. “Adjusting to Reality: As Proposed, Restricting Corporate Interest Deductibility is Ill-Advised.” E-Brief. Toronto: C.D. Howe Institute. April.

Pantaleo, Nick, Finn Poschmann, and Scott Wilkie. 2013. Improving the Tax Treatment of Intellectual Property Income in Canada. Commentary 379. Toronto: C.D. Howe Institute. April.

Parkinson, David. 2021. “David Dodge’s big issue with the budget isn’t debt, but lack of growth.” Globe and Mail, April 29.

Parsons, Mark. 2011. Rewarding Innovation: Improving Federal Support for Business R&D in Canada. Commentary 334. Toronto: C.D. Howe Institute. September.

Robson, William B.P., and Miles Wu. 2021. “From Chronic to Acute: Canada’s Investment Crisis.” E-Brief 312. Toronto: C.D. Howe Institute. February 4.

United Kingdom. 2020. The Green Book. London: HM Treasury. December.

Appendix

Address Pressure on EI Premiums

A notable unfunded fiscal pressure comes from the employment insurance (EI) program. EI contribution rates are set such that the EI operating account breaks even over a seven-year period. On September 14, 2020, the government froze the 2021 and 2022 EI premium rates at the 2020 level (for employees, $1.58 per $100 in insurable earnings). That implies substantial hikes in EI premiums as of 2023, which will come on top of scheduled increases in Quebec and Canada Pension Plan premiums.

This Shadow Budget would credit the EI operating account to cover the cost of freezing EI contribution rates at their existing level beyond 2022. Since premium hikes required by law are already planned in the fiscal framework, this crediting would be expensed annually over the projection period as the premium shortfall adds to the annual deficit. Preventing a sharp rise in EI premiums would enable employers to retain and hire more workers – a boost that would particularly benefit small businesses, for which payroll taxes constitute a sizable share of operating costs.

Provide a General Investment Tax Credit

Business investment is critical to Canada’s recovery in both the short and long run. Canada’s stock of machinery and equipment and intellectual property (IP) products has been growing more slowly than the labour force for years (Robson and Wu 2021), undermining productivity and wages. Canada’s low business investment has caused forecasters, including the Bank of Canada, to mark down their projections of long-term growth. Ongoing need to keep workers and customers safe, repair supply chains and produce more closer to home will place additional demands on private sector investment in 2022 and beyond.

To help businesses meet this demand, and offset reluctance to invest on the part of businesses uncertain about the economic and policy outlook, this Shadow Budget would implement a temporary general investment tax credit. The credit would apply to all investments in depreciable assets, including intangibles, at a uniform rate of 5 percent. It would come into effect on April 1, 2022, and run until April 1, 2024. Its temporary nature would encourage early investment. The measure also has the advantage of being relatively neutral – letting businesses themselves decide what types of capital they need and what types of activities they will pursue. Its net cost over the projection period would be some $20 billion.

Lower the Corporate Income Tax Rate

Canada improved its tax environment for business investment during the early 2000s, and its relative performance in investment per worker responded, closing the gap with the United States and other industrialized countries. More recently, however, Canada has lost its competitive edge. Other countries have been lowering their corporate income tax rates, and changes in the United States – dropping its corporate income tax rate in 2018 from 35 percent to 21 percent and providing immediate write-offs for many capital investments – dramatically boosted its attractiveness for new equity-financed business investment (Bazel and Mintz 2017; McKenzie and Smart 2019). This Shadow Budget would reduce the corporate income tax rate by two percentage points, from 15 percent to 13 percent, starting in 2025 after impact of the temporary investment tax credit subsides.

A lower corporate income tax rate would provide additional locational incentives for investments and profits in Canada. It would also create favourable conditions for wage increases, since corporate income taxes in a small, open economy like Canada’s mainly lower workers’ wages (Boadway and Tremblay 2016; McKenzie and Ferede 2017). This change initially would reduce federal revenues by $3.8 billion annually. However, as investors and business managers respond positively, the tax base would expand, reducing the net impact on tax revenues over time and boost provincial revenues.

Incentivize Innovation Adoption and Commercialization

Research and development (R&D) expenditures reflect both supply-push and demand-pull drivers. On the supply side, the Scientific Research and Experimental Development tax credit decreases the direct cost of initial knowledge creation. On the demand side, however, Canadian companies show a discouragingly low propensity to incorporate such knowledge, whether it originates in Canada or abroad, in their production. On a per worker basis, Canadian businesses invest only about one-quarter as much in IP products as US businesses do (Robson and Wu 2021).

To address this R&D demand-side shortfall, this Shadow Budget would establish an “IP Box” tax mechanism by which income derived from patents and other IP arising from real activity in Canada would face a lower corporate tax rate – a mechanism similar to that adopted by Saskatchewan and Quebec in recent years. The rationale for such a mechanism is to encourage Canadian businesses to pursue the commercialization of innovation. Evidence suggests that firms would undertake more R&D in Canada if the returns, or the fruits of their efforts, were taxed at a lower rate (Parsons 2011). It would also discourage the shifting of highly mobile IP income to lower-tax jurisdictions. Aiming to arrive at a combined federal-provincial IP Box special rate corresponding to the tentative global minimum rate of 15 percent could substantially reduce the fiscal cost of the IP Box without engendering harmful tax competition (Lester, forthcoming).

The IP Box would have the added benefit of incentivizing Canadian-IP-related production to remain within Canada’s borders, thus capturing much of the beneficial commercialization spillover effects. This measure also would seek to balance the tax benefits of the R&D credit with those related to adopting, commercializing or otherwise employing the new knowledge. Based on the review in Pantaleo, Poschmann, and Wilkie (2013), we estimate the cost to the federal budget initially would be around $500 million annually.

Raise the GST Rate

Consumption taxes are the least distortive to economic growth and, considering Canada’s relatively low reliance on them among industrialized countries, are a superior way to raise needed revenues (FTWG 2020). In comparison with other revenue sources, consumption taxes such as the Goods and Services Tax (GST) do less harm to investment and growth than do taxes on capital and personal income, and are a more stable and reliable source of revenues. Because the GST base is more resilient to rate increases, heavier reliance on the GST by the federal government would do less damage to provincial revenues. To help pay for the massive pandemic-related financial aid to Canadians, this Shadow Budget would raise the GST rate by two percentage points in 2023, restoring the GST rate to its level before July 2006.

Transition Federal Employees to Jointly Governed Shared-Risk Pension Plans

This Shadow Budget would initiate a transition of federal employees’ pension plans to shared-risk plans in which taxpayers do not bear all the risks related to the future cost of these benefits; as well, joint governance would give employee representatives a voice in the long-term sustainability of the plans. The plan for federal members of Parliament, which is completely unfunded and offers retirement benefits far richer than any other plan, would be at the top of the list for this transition. This change would have the important long-term benefit of subjecting public servants and MPs to annual contribution limits more like those that apply to other Canadians – and, over time, would foster more generous limits for the majority of the population that currently has overly limited opportunities to save for retirement. The change would have no fiscal cost over the projection horizon, but, over time, would reduce the fluctuations in net debt that result from changes in the value of pension promises that were unforeseen or that reflect the under-recording of pension benefits as they accrued (Laurin and Robson 2020).

Raise the GST Rate on Transportation Fuels

The government has committed to increase the carbon tax from the $50 per tonne planned for 2022 to $170 by 2030. This increase will require addressing competitiveness issues, possible border adjustments, and consultation and coordination with the provinces.

This Shadow Budget suggests that, in the meantime and at least until the carbon price gets to a more significant level, an increase in the GST rate applied to transportation fuels would provide a powerful means of controlling carbon dioxide emissions. Using the GST in this way would avoid some competitiveness problems, as the tax effectively would be paid only on the net value added when goods and services are purchased by domestic final consumers. Although this approach would attenuate the incentive to reduce CO2 emissions on intermediate activities, it would avoid the distortions that occur when taxes cascade on intermediate inputs bought and sold, but not on internal firm transactions. Increasing the GST on transportation fuels by ten percentage points, starting in fiscal year 2024/25, would give consumers a strong price signal to discourage CO2 emissions. By helping Canada achieve its emission targets at less cost to investment and jobs than a regulatory approach and by financing the government through a relatively growth-friendly tax, this change would support both the environment and the economy. The timing of this measure reflects desire to avoid adding to costs before the recent surge in energy prices has abated. This measure would generate about $8 billion in additional revenues in the first year, with amounts gradually shrinking over time as demand adjusts.

Prioritize Infrastructure under Federal Control

This Shadow Budget would prioritize direct funding for infrastructure projects that the government, on its own, can implement expeditiously. New funds would flow to projects where the national interest makes government involvement uniquely appropriate, such as investments in capacity and added security for marine, rail and air transportation. Unlike transfers that appear as expenses in the short run, these investments would be amortized over the period – typically twenty to thirty years – during which the asset in question would be expected to deliver its services.

The second phase of the Invest in Canada Plan, which began in fiscal year 2018/19, envisioned about $7.9 billion in federal grants in support of provincial and local infrastructure projects in 2022/23, rising to an extraordinarily ambitious $11 billion in 2027/28. Replacing about one-quarter of the amounts budgeted for Phase 2 infrastructure transfers over the projection period with direct investments under federal control, and thus amortized over a long period, would reduce planned expenses by an average of about $2.2 billion annually over the period.

Ensure Competitive Compensation for Federal Employees

This Shadow Budget would freeze departmental operating budgets for wages and salaries at their 2021 levels for five years, giving managers latitude to adjust compensation to better reward higher performers and reduce the number of less valuable positions. This approach could help achieve a better balance between federal public and private sector compensation with a low risk of disruption to public services (Lahey 2011). The freeze would reduce federal spending by at least $1 billion in fiscal year 2022/23, growing to $5.7 billion in the last year of the freeze.

Close the Strike Pay Tax Loophole

This Shadow Budget would fix an anomalous feature of Canada’s tax system that allows some income to escape income tax and that subsidizes strikes. Union dues paid by employees are deductible from their taxable income; any returns on those funds invested by the unions escape tax, and amounts paid out in strike pay are not taxable. This tax-free treatment is unusual. It contrasts strongly with the treatment of ordinary compensation, which attracts tax when it is paid and, if not consumed, yields taxable investment returns. It also contrasts with the treatment of most tax-recognized saving, which avoids taxation up-front, as in a Registered Retirement Savings Plan, or on distribution, as in a Tax Free Savings Account, but does get taxed at least once. Providing a tax preference to income earned when on strike, this tax-free treatment subsidizes activity that harms the Canadian economy (Alarie and Sudak 2006; Kesselman 1999).

This Shadow Budget would introduce legislation to make strike pay taxable as ordinary income. The revenue impact of this measure would vary depending on the number and compensation of employees involved in work stoppages, but usually would be less than $10 million annually.

Provide More Generous Tax Treatment of Non-discretionary Medical Expenses

A key principle in taxing personal incomes is that people who would be equally well off without taxation should be equally well off with it. If people pay tax on income they need to cover non-discretionary costs related to, say, children, healthcare or deductions from employment income, they will have lower after-tax discretionary income than people without such costs. Most personal income tax systems provide exemptions, deductions or credits related to non-discretionary expenses.

Although Canada’s personal income tax system does recognize this principle in part – for example, employer-paid premiums for health and dental plans are exempt from taxable income – its treatment of health-related expenses is overly restrictive. The current medical expense tax credit applies only to expenses exceeding 3 percent of net income or $2,479, whichever is lower, and is calculated at the bottom tax rate. The health impacts of the COVID-19 pandemic have made this restriction especially problematic. This Shadow Budget would lower the threshold on such expenses to 1.5 percent of net income or $1,240, whichever is lower. This change would help people who must cover medical costs directly or through health-related insurance premiums. The fiscal cost of this measure would be about $500 million per year. Employer-paid health premiums would continue to be untaxed.

Rationalize the Age Credit

The income tax regime’s age credit provides a subsidy to seniors who already benefit from a number of federal and provincial transfers and in-kind benefits. As a redistribution measure, the age credit is poorly targeted: at a given income level, a younger person might have needs as great as, or greater than, those of an older person. The increased medical expense tax credit proposed in this Shadow Budget would further lower the need for an age credit. Furthermore, the amount is clawed back on incomes between $38,893 and $90,313, which increases the marginal effective tax rate for such seniors. This Shadow Budget would reduce the base amount of the age credit from $7,898 to $4,000, which is closer to the amount most provinces use for their old age tax credits. This measure would save more than $2 billion annually.

Phase Out the Tax Credit for First-Time Homebuyers

Government measures that increase the demand for housing are problematic, increasing price pressures in markets where housing supply is constrained and inducing households to take on debt they might have trouble servicing in the event of an economic downturn or an increase in interest rates. This Shadow Budget would phase out the tax credit for first-time homebuyers, saving about $100 million annually.

Eliminate the Tax Credit for Labour-Sponsored Venture Capital Corporations

The tax credit for labour-sponsored venture capital corporations (LSVCCs) notoriously distorts saving and investment. In general, venture capital funding spurs innovation, but among the various venture capital funds in Canada, LSVCCs are among the least efficient in this respect (Fancy 2012). In addition, LSVCCs crowd out alternative private venture investments and favour portfolios unsuitable for retail investors. This Shadow Budget would eliminate the LSVCC credit, which would improve the government’s bottom line by about $200 million annually.

Appendix References

Alarie, Benjamin, and Matthew Sudak. 2006. “The Taxation of Strike Pay.” Canadian Tax Journal 54 (2): 426–49.

Bazel, Philip, and Jack Mintz. 2017. “Tax Policy Trends: Whether It Is the U.S. House or Senate Tax Cut Plan – It’s Trouble for Canadian Competitiveness.” Calgary: University of Calgary, School of Public Policy. November.

Boadway, Robin, and Jean-François Tremblay. 2016. Modernizing Business Taxation. Commentary 452. Toronto: C.D. Howe Institute. May.

Fancy, Tariq. 2012. “Can Venture Capital Foster Innovation in Canada? Yes, but Certain Types of Venture Capital Are Better than Others.” E-Brief 138. Toronto: C.D. Howe Institute. September.

FTWG (Fiscal and Tax Working Group). 2020. “Communiqué #3: Permanently Higher Federal Spending Threatens GST Hike.” Toronto: C.D. Howe Institute. November 27.

Kesselman, Jonathan R. 1999. “Base Reforms and Rate Cuts for a Revitalized Personal Tax.” Canadian Tax Journal 47 (2): 210–41.

Lahey, James. 2011. “Controlling Federal Compensation Costs: Towards a Fairer and More Sustainable System.” In How Ottawa Spends, 2011-2012, ed. Christopher Stoney and G. Bruce Doern, 84–105. Montreal; Kingston, ON: McGill-Queen’s University Press.

Laurin, Alexandre, and William B.P. Robson. 2020. “Under the Rug: Pitfalls Abound in Reporting Federal Employee Pension Obligations.” C.D. Howe Institute Intelligence Memo. Toronto: C.D. Howe Institute. December 3.

Lester, John. Forthcoming. “An Intellectual Property Box for Canada – Why and How?” E-Brief. Toronto: C.D. Howe Institute.

McKenzie, Kenneth, and Ergete Ferede. 2017. “The Incidence of the Corporate Income Tax on Wages: Evidence from Canadian Provinces.” SPP Technical Paper. University of Calgary: School of Public Policy. April.

McKenzie, Kenneth, and Michael Smart. 2019. Tax Policy Next to the Elephant: Business Tax Reform in the Wake of the US Tax Cuts and Jobs Act. Commentary 537. Toronto: C.D. Howe Institute. March.

Pantaleo, Nick, Finn Poschmann, and Scott Wilkie. 2013. Improving the Tax Treatment of Intellectual Property Income in Canada. Commentary 379. Toronto: C.D. Howe Institute. April.

Parsons, Mark. 2011. Rewarding Innovation: Improving Federal Support for Business R&D in Canada. Commentary 334. Toronto: C.D. Howe Institute. September.

Robson, William B.P., and Miles Wu. 2021. “From Chronic to Acute: Canada’s Investment Crisis.” E-Brief 312. Toronto: C.D. Howe Institute. February 4.

Veall, Mike. 2020. “Freezing EI Premiums.” Intelligence Memo. Toronto: C.D. Howe Institute. June 5.