Weakness in Canadian GDP since the Bank of Canada began raising its policy rate in March 2022 has spurred much talk of the possibility of a recession.1At a meeting in early 2024, the Council weighed the evidence of a recession having occurred in the past two years and whether current conditions could presage one.

The Business Cycle Council (BCC) of the C.D. Howe Institute is an authoritative arbiter of business cycle dates in Canada. This Communiqué comments on the last two years of data, including the current state of Canada’s economy, and whether the BCC’s definition of a recession has been met at any point over this timeframe.

According to the Council’s methodology, as outlined in a December 2017 publication, a recession is a pronounced, persistent and pervasive decline in real economic activity. The Council considers several variables in making recession determinations.2 First, a decline in quarterly GDP, measured by total expenditure on goods and services, of at least one quarter is a necessary minimum for a recession. If whatever is provoking the slowdown in economic activity does not lead to at least one quarter of outright decline, it has not produced the cutbacks one expects to see when studying business cycle downturns. Second, the decline in economic activity must either be large or be accompanied by weakness in contiguous quarters, implying a net contraction, or at least stagnation, in the economy over a two-quarter period. Third, the decline must be broad in nature – that is, experienced by more than one or two industries.

The latest available data show that the Canadian economy did not fulfil these conditions in 2022 or 2023.

Monthly GDP by industry fell in January, April, October and December 2022, and again in April, June, July, September, and December 2023.3 But, except for January 2022 and July 2023, employment rose in each of those months.4

Quarterly GDP by expenditure decreased in the last quarter of 2022 and in the third quarter of last year. The BCC’s measure of breadth, a diffusion index, dropped just below 50, to 48.9, in the fourth quarter of 2022, meaning more industries than not experienced downturns. However, the declines were mild at 0.1 percent for each quarter. Moreover, employment increased in both quarters. In both cases, the quarters of a shrinking economy were bracketed by quarters of growth. Additionally, the cumulative growth of GDP over the two-quarter periods that included the negative quarters was positive.5 We judge that these downturns were not persistent enough to be called recessions.6

Looking ahead, the C.D. Howe Institute’s leading economic activity index has been declining steadily since the Bank of Canada began tightening monetary policy, and now sits approximately at the level it was at in March 2021 when inflation was last at target – a sign of continuing economic weakness. The Council is closely monitoring developments in economic data and stands ready to meet to discuss a recession call if GDP shrinks more, or for longer, or more broadly in the months ahead.

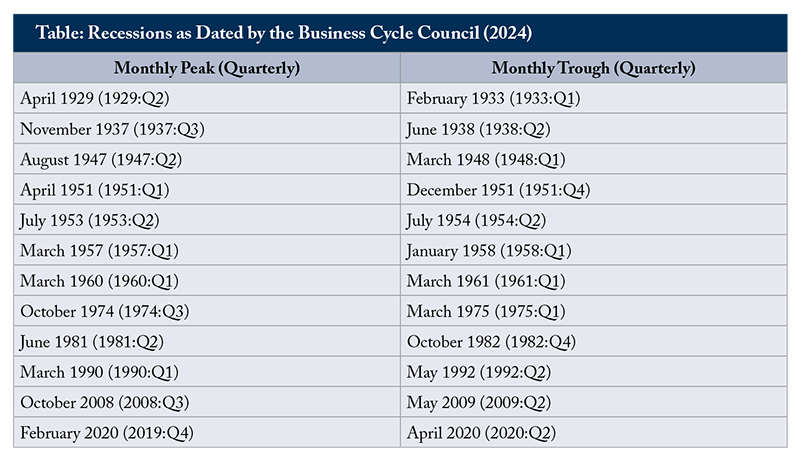

The following table7 gives the list of historical recessions since the Great Depression.

So Far, So Good: C.D. Howe Institute Business Cycle Council Declares Recession Avoided in 2022, 2023

Members of the C.D. Howe Institute Business Cycle Council

Members of the Council participate in their personal capacities, and the views collectively expressed do not represent those of any individual, institution, or client.

Steve Ambler, Co-Chair, Professor, Université du Québec à Montréal; David Dodge Chair in Monetary Policy Council, C.D. Howe Institute.

Jeremy Kronick, Co-Chair, Associate Vice President, Director of the Centre on Financial and Monetary Policy, C.D. Howe Institute.

Michelle Alexopoulos, Professor of Economics, University of Toronto.

Ted Carmichael, Founding Partner, Ted Carmichael Global Macro.

Philip Cross, Former Chief Economic Analyst, Statistics Canada.

Stephen Gordon, Professor of Economics, Université Laval.

Eric Lascelles, Chief Economist, RBC Global Asset Management.

Stefane Marion, Vice President & Chief Economist, National Bank of Canada.

Angelo Melino, Professor of Economics, University of Toronto.

- 1 In December 2022, all six of the major Canadian chartered banks were predicting at least one quarter of negative growth (decline) in GDP in 2023. Three of the six were predicting two consecutive quarters of negative growth. According to their most recent forecasts, only the National Bank of Canada is predicting any quarters of negative growth in 2024 (in the second and third quarters).

- 2 In particular, two quarters of negative GDP growth are neither necessary nor sufficient for the BCC to label a downturn a recession, despite the misconception that this constitutes the “official” definition of a recession. There is no such thing. Notably, the BCC judged in December 2018 that the two-quarter downturn of 2015 was not pronounced – in an employment sense – or pervasive enough to be called a recession.

- 3 Statistics Canada, Table 36-10-0434-01, accessed March 5, 2024.

- 4 Statistics Canada, Table 14-10-0310-01, accessed March 5, 2024.

- 5 See Statistics Canada, Table 36-10-0104-01.

- 6 The GDP numbers for 2022 and 2023 are subject to revision by Statistics Canada. If there are important downward revisions to GDP, the Council will revisit the downturns which occurred in 2022 and 2023.

- 7 Available online at https://www.cdhowe.org/sites/default/files/attachments/pages/mixed/Rece….