The Study In Brief

This E-Brief analyzes the expected fiscal and behavioural consequences of the significant reforms proposed for the Alternative Minimum Tax (AMT) in the 2023 federal budget.

This E-Brief analyzes the expected fiscal and behavioural consequences of the significant reforms proposed for the Alternative Minimum Tax (AMT) in the 2023 federal budget.- The 2023 budget asserts that the “AMT will more precisely target the very wealthy.” Our findings indicate that the new AMT regime will primarily fall on individuals who report occasional instances of very large capital gains – exceeding $500,000 – in a year.

- High-income individuals often make generous charitable donations. Our estimates indicate that about 10 percent of the overall value of charitable donations and almost half of the overall value of donations of publicly listed securities will be impacted by the reduced tax incentives for charitable giving in the proposed AMT. These provisions might disproportionately damage the charitable sector when compared to the slight increase in tax revenues we project they will generate, and need reconsideration.

- Our main conclusion is clear: the proposed AMT regime will primarily increase the tax burden on very large capital gains and charitable donors, albeit clumsily. And if the government intends to target large capital gains and charitable donations, it should instead approach this goal directly and transparently, in a way that the public can discuss and debate, rather than surreptitiously.

We extend our gratitude to Brian Ernewein for his previous support and collaborative efforts on a related presentation and intelligence memo, along with his insightful feedback. Our thanks also go to Daniel Schwanen, Mawakina Bafale, Heather Evans, Gerald MacGarvie, William Molson, Nick Pantaleo, Kevin Wark and anonymous reviewers for their helpful comments on the review draft of this report. Any errors, along with the analysis and conclusions presented herein, are solely our responsibility.

Introduction

On March 28, 2023, Finance Minister Chrystia Freeland tabled the latest federal budget which included a series of reforms to the Alternative Minimum Tax (AMT).

This E-Brief investigates who would be targeted by the AMT reforms, how much more they would pay, how much more tax revenues will be raised and how potential behavioural responses would affect the fairness and effectiveness of the proposed tax change.

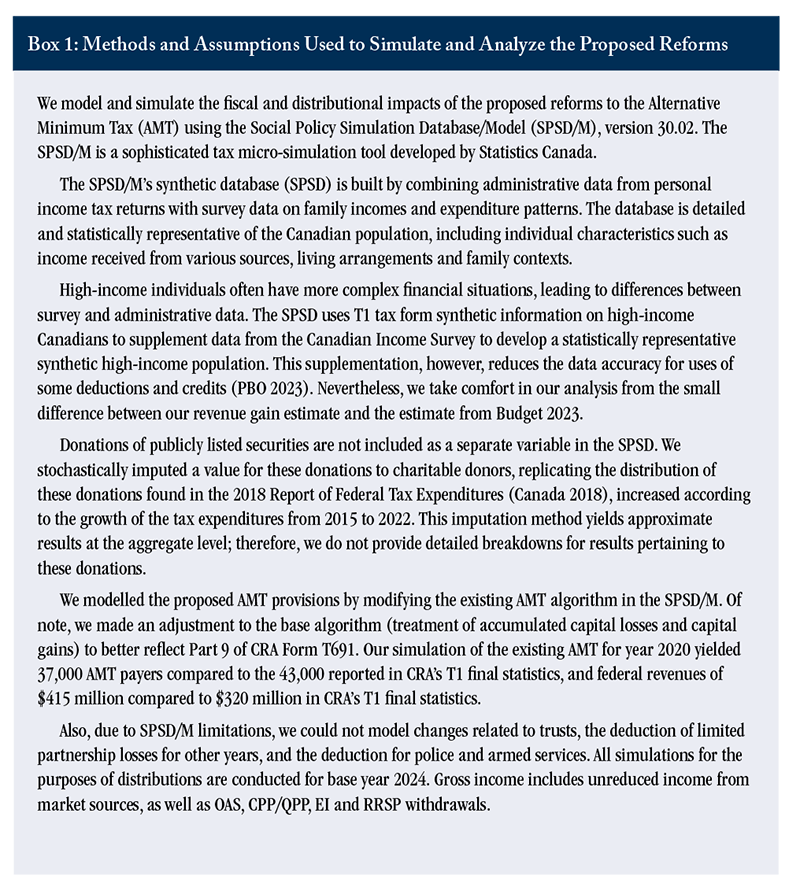

Most of the analysis presented relies on modelling using Statistics Canada’s Social Policy Database and Model (SPSD/M). Box 1 provides a detailed explanation of the methods and assumptions that we used to perform our analysis.

The AMT: Purpose and History

An AMT is calculated alongside the regular income tax, and taxpayers must pay whichever amount is higher between the two. Nearly everyone’s regular income tax surpasses the amount determined under the AMT, so only relatively few end up paying the AMT.

Canada’s AMT was introduced in the 1985 federal budget and came into effect in 1986. The government aimed to boost tax revenues to combat the deficit. At the time, the use of tax deductions and exemptions dominated the personal income tax system. Indeed, by 1984 only 60 percent of total assessed personal income was deemed taxable. Personal exemptions accounted for a significant portion of the remaining 40 percent (Canada 1987).

A federal discussion paper identified that 8 percent of high-income tax filers paid less than 10 percent of their gross income in taxes in 1982 (Canada 1985). The dividend tax credit, the capital gains exclusion, the deduction for carrying charges exceeding investment income, the investment tax credit and negative net rental income from multiple-unit residential buildings were key factors reducing tax liabilities for these high-income filers (Canada 1985).

The 2022 federal budget offered a comparable assessment. It stated that 18 percent of those earning more than $400,000 in 2019 paid an average federal personal income tax rate of only 10 percent or less, with 28 percent facing an average rate of 15 percent or less. The only reason provided for this finding was that these high-income tax filers “make significant use of deductions and tax credits and typically find ways to have large amounts of their income taxed at lower rates” (Canada 2022).

Ernewein, Laurin, and Dahir (2023) found that the 50 percent capital gains inclusion rate and the lifetime capital gains exemption accounted for nearly three-quarters of the cases where higher-income individuals had an average federal tax rate below 15 percent in 2019. Registered Retired Savings Plan (RRSP) contributions and charitable donations also contributed notably. Indeed, the primary causes of these low average tax rates stem from widely used and accepted income tax provisions.

The proposed AMT regime intends to limit or eliminate the effect of many tax exemptions, deductions and credits available under regular tax rules. These proposed restrictions might not necessarily relate to aggressive tax planning, but instead might reflect the application of standard – and typically accepted – tax provisions. Hence, the justification for a reformed AMT based strictly on fairness remains unclear. If the government truly believes that tax filers misuse or overuse certain tax preferences, like partial capital gains inclusion or charitable giving incentives, it can directly restrict their application and clarify its stance on how exactly these provisions are being improperly utilized or excessively claimed for the public to debate.

Proposed AMT: A Description

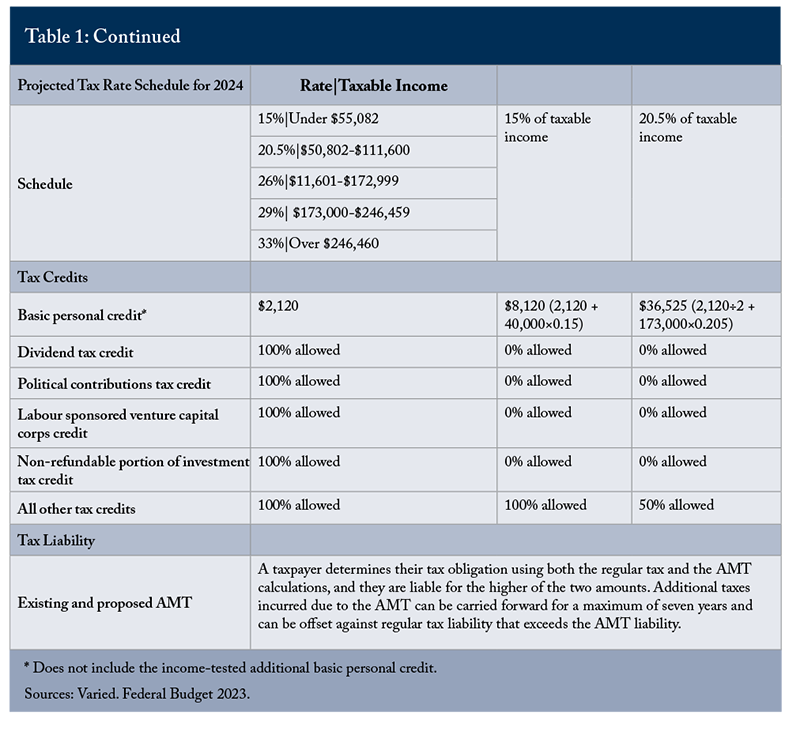

The proposals would increase the alternative basic personal exemption from $40,000 to the inflation-indexed threshold of the second-to-top tax bracket, projected to be $173,000 in 2024. Additionally, the proposals would raise the alternative tax rate from 15 percent to 20.5 percent, aligning it with the rate of the second federal income tax bracket.

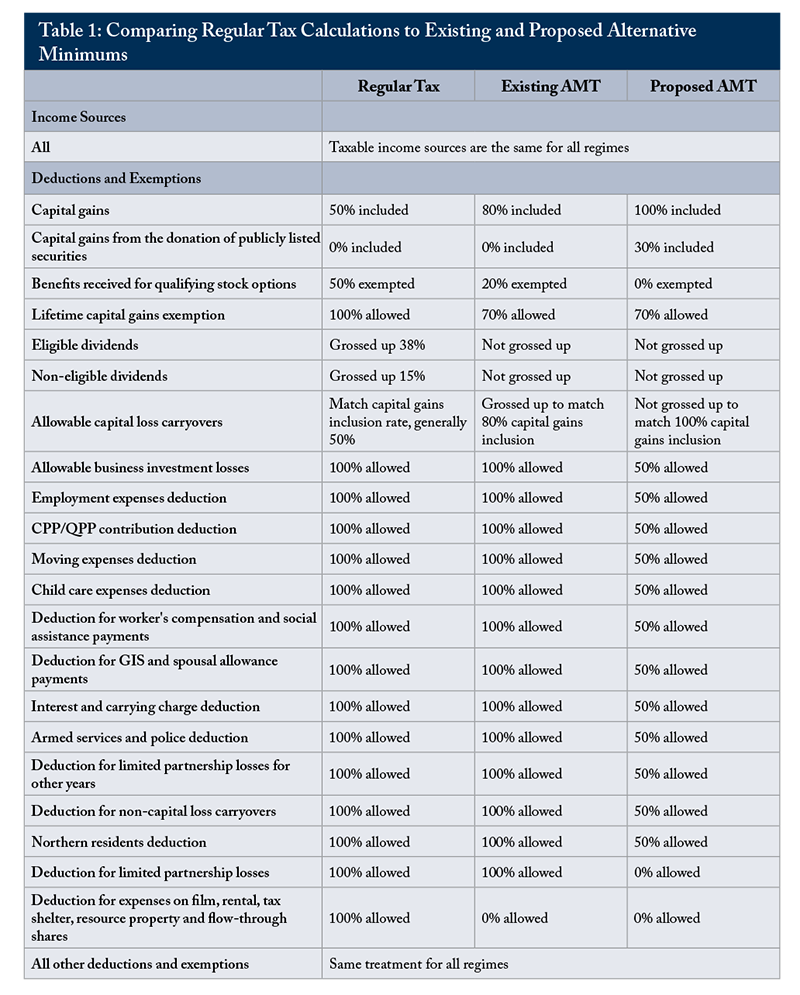

Table 1 summarizes the alternative tax calculations under the existing and proposed AMT compared to regular tax calculations.

Taxable income sources are the same for the three income tax calculations, but deductions and exemptions vary. Capital gains tax treatment varies notably between the regular tax, existing and proposed AMT regimes. Under the regular tax, 50 percent of capital gains are included in taxable income, while the existing AMT includes 80 percent. The proposed AMT is stricter, including 100 percent of capital gains. Additionally, capital gains resulting from the donation of publicly listed securities (PLS) are fully exempt under both the regular tax and the existing AMT, but the proposed AMT would tax 30 percent of these gains.

The benefits received for qualifying stock options, which are exempted at 50 percent under the regular tax, see a sharp reduction in the existing and proposed AMT, with the latter offering no exemption at all. The dividend tax credit is also eliminated for both AMT calculations.

The proposed AMT will only allow half the value of deductions for a wide range of items, from child care expenses to moving costs. Furthermore, the proposed AMT framework significantly curtails deductions for both capital and non-capital losses, deviating from fundamental principles of income taxation.

As already mentioned, both AMT regimes adopt a flat tax rate.

In the regular tax system, numerous tax credits may substantially decrease basic tax payable. While both the existing and proposed AMT disallow a number of tax credits, the proposed AMT casts a much larger net. It permits the claim for only 50 percent of the value of almost all tax credits. A significant example of this is the charitable donations tax credit, where for the same donation, only half the credit that could be claimed under the regular tax calculation can be claimed under the proposed AMT.

The Newly Proposed AMT Regime: Who is Impacted and by How Much?

In this section, we examine the potential triggers of AMT liability, look at the targeted individuals, estimate the additional amount they might owe and project the potential increase in tax revenues.

Who: Mostly Individuals with Large Capital Gains

Few individuals currently face the AMT burden. From 2011 to 2020, on average, only 0.14 percent of all tax filers – 43,200 taxpayers in 2020 – paid extra taxes because of the AMT. The roster of those affected by the AMT probably changes considerably each year. When the federal government introduced the AMT in the mid-1980s, its longitudinal data analysis showed that fewer taxpayers with consistently high incomes paid minimal or no tax over extended periods compared to the much larger number of those with occasional high incomes in a single year (Canada 1985).

Under current rules, about half of AMT payers would earn less than $300,000 in 2024. The proposed AMT would target those with much higher incomes. About two-thirds of AMT payers would report gross incomes above $600,000, and almost all (95 percent) would earn more than $300,000.

Perhaps most interestingly, the higher exemption in the proposed regime would exclude some 83 percent of AMT payers under current rules. However, the proposed changes that deny certain credits, deductions and exemptions would work in the opposite direction, bringing many more filers under the AMT umbrella. Overall, these changes would decrease the number of tax filers subject to the AMT by approximately 20 percent.

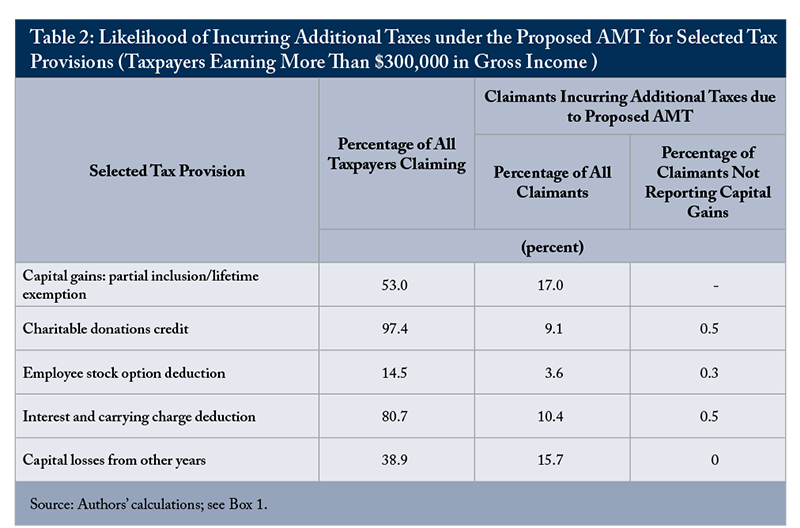

On closer examination, realized capital gains significantly influence whether a taxpayer will owe additional taxes under the proposed AMT. Table 2 details the characteristics of high-income taxpayers, representing nearly all of the proposed AMT payers. This table focuses on specific tax provisions, selected because they account for the majority of the increased tax liabilities.

About half of high-income individuals – those earning more than $300,000 annually – declare capital gains, and most make charitable donations. Many also take the employee stock option deduction, deduct interest and carrying charges or carry over capital losses from previous years. The likelihood of incurring additional taxes due to the proposed AMT ranges from 17 percent of high-income individuals claiming the partial capital gains inclusion to some 4 percent of those claiming the employee stock option deduction. However, for those not declaring capital gains, the chance of incurring AMT under the proposed regime drops to less than one percent. Clearly, declaring capital gains stands out as the primary trigger for the proposed AMT.

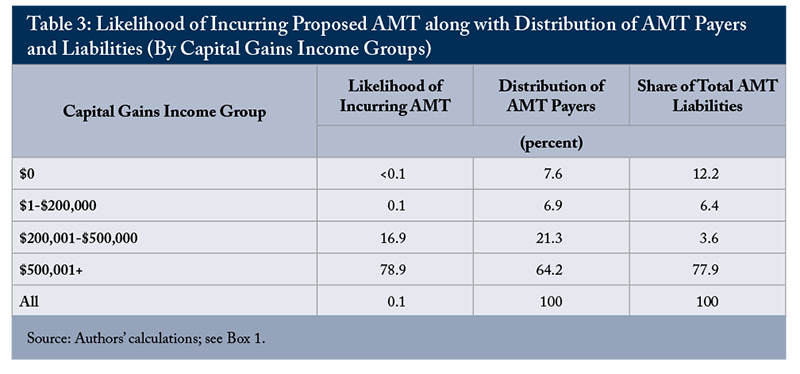

Under the proposed regime, nearly 92 percent of AMT payers would report capital gains (Table 3). Yet, the probability of incurring AMT is virtually nonexistent for those declaring capital gains of less than $200,000. However, this risk rises sharply with the value of reported capital gains. Specifically, individuals declaring more than $500,000 in capital gains would face close to an 80 percent chance of incurring AMT. These individuals would also account for nearly 80 percent of all AMT liabilities, as illustrated in Table 3.

These findings suggest that the proposed AMT narrowly targets those with substantial capital gains, as nearly 80 percent of its revenue would derive from these individuals. Since those reporting significant gains also report the majority of all annual gains, the AMT would encompass about 40 percent of the total value of all reported capital gains within a year.

How Much: Average Tax Rates for AMT Payers Would Increase

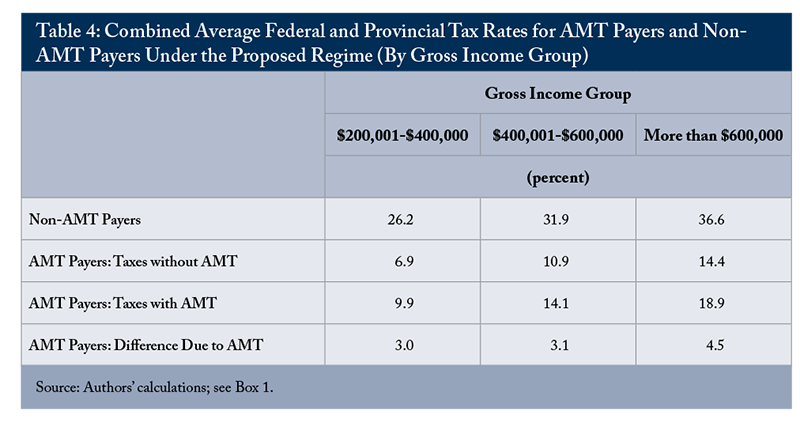

The proposed AMT would levy additional taxes on a significant portion of reported capital gains, yet the rise in the top effective capital gains tax rate would be relatively small. Therefore, AMT payers would experience what looks like a small uptick in their average tax rates on gross income when viewed in absolute terms. However, this tax increment is significantly larger in relative terms, given that AMT payers initially have lower average tax rates.

Table 4 shows average tax rates for individuals by gross income groups relevant for the proposed AMT, combining both federal and provincial rates. Average tax rates for non-AMT payers rise from 26.2 percent to 36.6 percent. AMT payers typically exhibit much lower average tax rates, mainly due to the half-inclusion of capital gains. The application of the AMT raises their average tax rates by 3-to-4.5 percentage points, which equates to an overall increase of more than 30 percent.

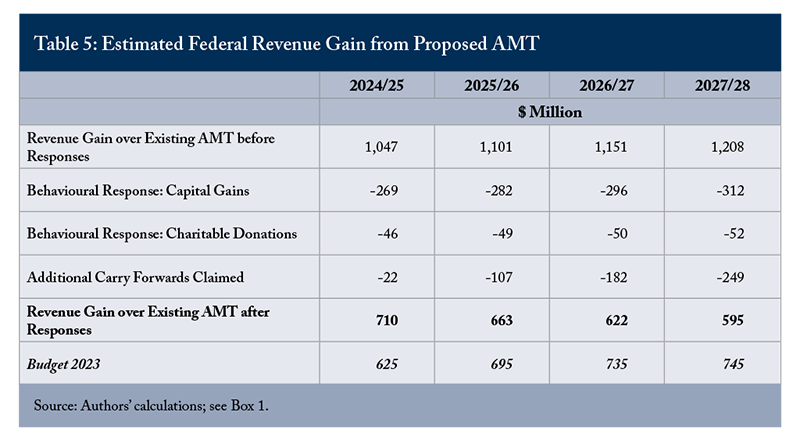

The 2023 budget estimated the federal government would gain $625 million in additional revenue from the AMT reforms in 2024/25, increasing to $745 million by 2027/28. This estimation includes an allowance for taxpayer behavioural responses and revenues lost due to the probable future use of additional AMT carry forwards.

Our own modelling of the proposed AMT (Box 1) initially yields an estimated revenue gain of $1,047 million for the 2024/25 fiscal year before accounting for any behavioral responses. However, we make three adjustments to this estimate.

Firstly, as the new AMT regime significantly targets capital gains recipients, we expect a decline in capital gains realizations as a response. In our model, we base our capital gains response on the median responsiveness to change in the capital gains tax rate found in a literature review by the US Congressional Research Service (CRS 2021).

Secondly, we account for the probable response of charitable donors to an increase in the after-tax cost of their donations. We provide details on our methodology in the upcoming section, which specifically addresses the AMT’s impact on reducing charitable donations.

Thirdly, we also subtract the potential increase in the use of AMT carry-forwards due to the increase in additional AMT incurred. The resulting revenue gain accounting for these three adjustments declines from $710 million in 2024/25 to $595 million in 2027/28 (Table 5).

As a result, our estimated revenue gains, while lower and decreasing, remain comparable to the projections in Budget 2023.

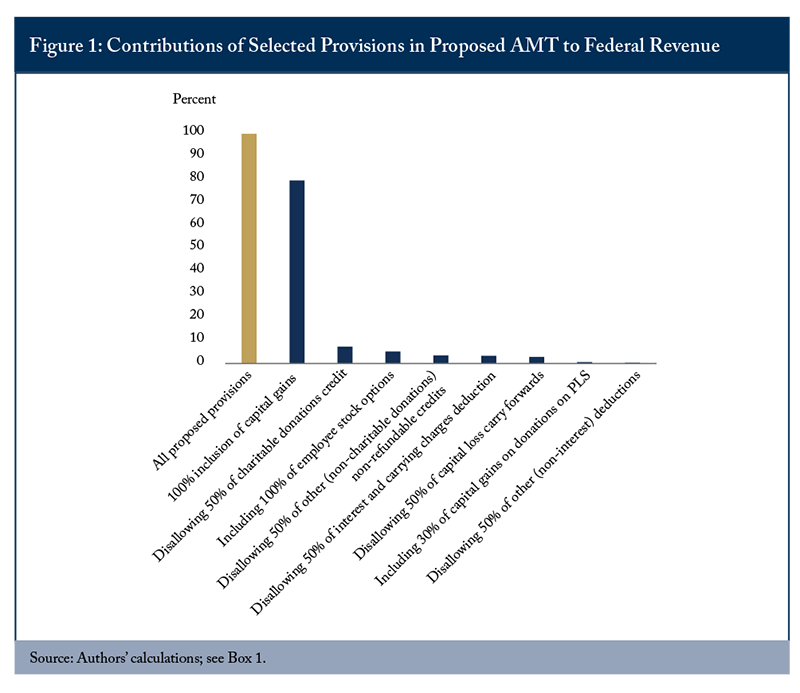

Figure 1 presents a breakdown of our revenue estimate, highlighting the contributions from the alternative treatment of key exemptions, deductions and credits in the proposed AMT. If we maintain the capital gains inclusion rate at its ordinary 50 percent under the proposed AMT, but keep all other AMT parameters constant, the AMT’s revenue collection would decrease by about 80 percent.

The next major proposed AMT change involves cutting the charitable donations tax credit in half, which is responsible for a little over 7 percent of proposed AMT revenues. When combined with the 30 percent inclusion of capital gains on donations of publicly listed securities, charitable donation provisions contribute a total of 8 percent to the estimated revenue generated under the proposed AMT. Together, these new provisions concerning capital gains and charitable donations would make up nearly 90 percent of the total proposed AMT revenues.

Policy Discussion

The official objective behind the AMT is to ensure a fair tax contribution from all individuals and entities. What is not clear is how disallowing the use of entirely legitimate tax provisions like loss utilization, tax credits for charitable donations and partial inclusion of capital gains enhances fairness. The new regime would primarily target occasionally large capital gains and, to a lesser extent, charitable giving.

It is highly probable that sophisticated taxpayers would adopt a variety of tax strategies to diminish the impact of the proposed AMT changes, especially in relation to occasionally large capital gains and donations. Therefore, less informed taxpayers or those unable to manage a capital gains event would likely bear the brunt of the new rules. As a result, the Conference for Advanced Life Underwriting has advocated for the implementation of a three-year carry backward option for AMT recovery, in addition to the existing seven-year carry forward provision (CALU 2023). Introducing a three-year “look back” option would provide some degree of relief – and fairness – to less sophisticated taxpayers caught off guard by the new rules.

Taxing Large Lumpy Capital Gains by Stealth

New revenues from the reformed AMT would overwhelmingly rely on capital gains – especially larger gains. Individuals who declare substantial capital gains in a given year will most probably find themselves subject to the reformed AMT (Table 3).

The government has not given a policy explanation for the implicit focus on capital gains. There are sound policy justifications for the partial inclusion of capital gains. Capital gains on shares originate out of retained profits that bore taxes at the corporate level or they may represent the present value of future earnings. Exempting a portion of the gains at the personal level avoids double-taxing these profits. Providing favourable tax treatment to capital income increases prospective after-tax gains from risk-taking and entrepreneurial activities, the life blood of innovative ventures.

Partial inclusion of capital gains taxes also encourages the flow of capital from long and entrenched holdings in appreciated shares and properties to more productive or innovative ventures. Not to mention the fact that large capital gains tend to be associated with very long holding periods, and reduced taxation of the gains grossly compensates for the tax imposed on the inflationary portion of the gains. In almost all OECD countries, individuals across the income distribution face lower effective tax rates if they receive at least some of their income from capital gains, compared to exclusively from wages (OECD 2023).

Proponents of increased capital gains taxation in Canada argue for enhanced equity and fairness. They also aim to curtail complex tax planning and avoidance strategies that convert regular income into capital gains to benefit from the partial inclusion. Additionally, they see capital gains as a promising revenue source for the government (Boadway 2021, Kesselman 2023).

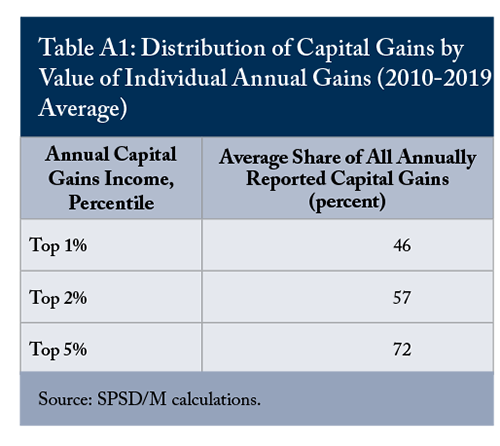

However, capital gains exhibit significant lumpiness at the top. Year over year, a handful of capital gains recipients represent the majority of total reported gains. Appendix Table A1 shows the distribution of average capital gains from 2010 to 2019, segmented by the value of individual annual gains. The concentration of capital gains at the top of the distribution is striking. On average, each year, the top 2 percent of individuals reporting capital gains generate about 60 percent of the overall value of all reported capital gains.

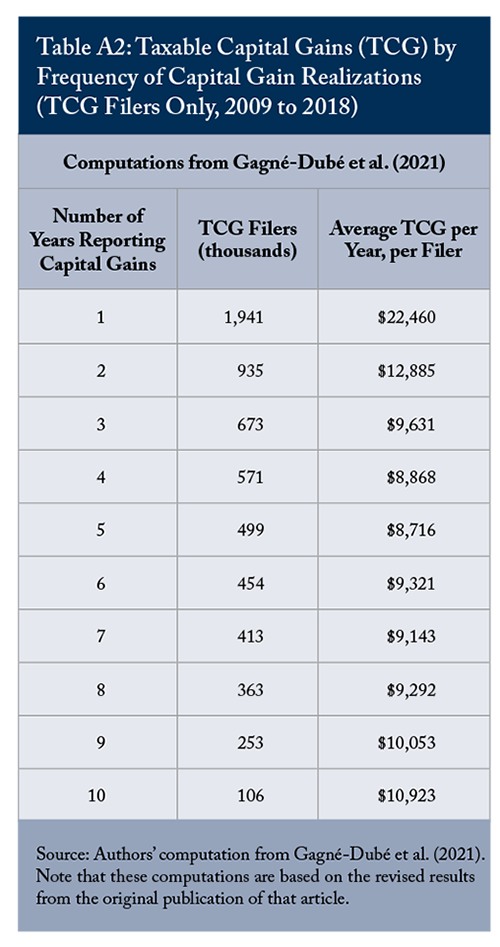

For the purposes of the AMT, it matters whether these few very large annual gains are repeatedly enjoyed by the same subgroup of tax filers over the years, or whether they are infrequent events. Gagné-Dubé et al. (2021) look at the frequency of capital gains realizations over the 2009-to-2018 period (computations are shown in Appendix Table 2). Average annual taxable gains are notably lower for recipients who report gains over multiple years compared to those who report gains for a single year. This observation, combined with the pronounced concentration of annual reported gains at the upper end of the distribution each and every year (Table A1), suggests that it is rare for a taxpayer to report more than one annual gain at the very top of the annual distribution (e.g., more than $500,000) over a decade – even among those who have declared capital gains in multiple years.

So capital gains tend to be quite unevenly distributed, and the proposed AMT directly targets this lumpiness. The rationale for targeting exceptionally large capital gains more than smaller ones, especially when smaller gains are frequently realized over multiple years, is not immediately apparent. If the intention is, indeed, to target large capital gains, the government should state it.6 The main advantage of transparency is that it allows for better public discussions and debates in Parliament. Behavioural distortions and negative economic impacts of heavier capital gains taxation could be debated and weighed against the alleged unfairness.

The proposed AMT is an awkward attempt, at best, to impose heavier taxation of capital gains. By disallowing half of prior-year capital loss offsetting, the AMT artificially inflates the net capital gains of taxpayers – a form of double taxation – penalizing those who might have a mix of good and bad years. Knowing they may not be able to offset all future gains with past losses might deter some investors from taking risks or investing in assets where the return is uncertain.

Moreover, the additional tax depends on both the size of the yearly gains and the amount of ordinary income earned in the year. Taxpayers with sizable ordinary income may pay less (or avoid altogether) additional tax liabilities on the capital gains, while others with more modest ordinary incomes will pay more.

There will be a strong motivation for individuals to align the realization of capital gains with years of significant ordinary income or to distribute realizations over multiple years to prevent exceptionally high gains in a single year. Additionally, owners of financial assets and real properties may be encouraged to form corporations to maintain the benefit of the partial inclusion rate, which remains accessible to corporations.

Impact on Charitable Giving

The proposed AMT introduces two provisions targeting charitable giving: it disallows half of the charitable donation tax credit and includes 30 percent of capital gains on donations of publicly listed securities. We calculate that the proposed AMT would likely capture just under 10 percent of the overall value of charitable donations and almost 50 percent of donations of publicly listed securities.

Charitable donations respond significantly to tax incentives. When tax incentives raise (or lower) the after-tax cost of a donation, individuals might give less (or more) or donate a smaller (or larger) amount. Many economic studies have examined the sensitivity of charitable donations to changes in their after-tax cost, known as the price elasticity of donations. Studies generally find a negative price elasticity of charitable giving, though the specific magnitude varies. A cautious approach would use an elasticity of minus one, meaning a 1 percent rise in the price of giving (from reduced tax incentives) could lead to a 1 percent decline in donations.

Hossain and Lamb (2012) report a Canadian elasticity of -1.68; a 2016 study by Finance Canada found a Canadian elasticity of -1.1 (Canada 2016). We cautiously use a price elasticity of -1.1 to estimate the potential response of charitable donations to the substantial reduction of tax incentives under the AMT.

Our analysis suggests that the proposed AMT could decrease the overall value of charitable donations in Canada by 4 percent. Donations of publicly listed securities might see a decline of 22 percent.

Such a 4 percent decline in overall charitable donations could severely harm the charitable sector. In 2021, this would have equated to almost $500 million less in donations.

Disallowing half of the charitable donation tax credit under the AMT and including 30 percent of capital gains on donations of publicly listed securities would generate only some $60 million in additional AMT taxes after accounting for the behavioural reaction. These provisions might inflict disproportionate harm on the charitable sector relative to the modest additional tax revenue they produce. These changes merit a serious reconsideration.

Conclusion

The proposed AMT reforms heavily depend on a small number of occasional, very large capital gains realizations to yield much of its revenues. The government’s focus on capital gains should be explicitly stated, and its rationale explained. The fact that much of the burden of the proposed AMT would fall on very large capital gains also lacks a clear policy explanation. Indeed, if intentional, the government should explain the logic behind prioritizing exceptionally large occasional gains over frequently recurring smaller ones.

Additionally, the AMT’s stance on charitable donations may considerably dampen charitable giving. Tax incentives play a crucial role in donation behaviours, and a reduction in these incentives, as proposed by the AMT, might result in a 4 percent decline in overall charitable donations – a blow to the charitable sector that the minimal additional tax revenues raised could hardly justify.

The rationale and consequences of the proposed AMT reforms need to be more clearly articulated. If the government still wants to tax large capital gains and reduce the tax incentives for charitable donors, it should express these goals explicitly and transparently in a manner conducive to being discussed and debated publicly, rather than by stealth.

Appendix

References

Blakes. 2023. “2023 August 4 Draft Legislation: Selected Tax Measures.” Bulletin. August. Available at blakes.com.

Boadway, Robin. 2021. “Options for the Reform of Capital Gains Taxation.” Perspectives on Tax Law & Policy. Canadian Tax Foundation. September.

Canada. 2022 Budget. Department of Finance Canada. April

______. 2023 Budget. Department of Finance Canada. March.

______. 1985. “A Minimum Tax for Canada.” Department of Finance. May.

______. 2016. “Report on Federal Tax Expenditures – Concepts, Estimates and Evaluations 2016: Part 9.” Department of Finance. February.

______. 2018. “Report on Federal Tax Expenditures – Concepts, Estimates and Evaluations 2018.” Department of Finance. April.

______. 1987. “The White Paper Tax Reform 1987.” Department of Finance. June.

Canada Revenue Agency (CRA) T1 Statistics. 2011 – 2020. Accessed at: https://www.canada.ca/en/revenue-agency/programs/about-canada-revenue-agency-cra/income-statistics-gst-hst-statistics/t1-final-statistics.html

Conference for Advanced Life Underwriting (CALU). 2023. “Letter to Finance relating to draft legislation released on August 4, 2023 as it pertains to the application of the Alternative Minimum Tax (AMT) rules.” Available at calu.com.

Congressional Research Service (CRS). 2021. “Capital Gains Tax Options: Behavioural Responses and Revenues.” Washington D.C. January.

Ernewein, Brian, Alexandre Laurin, and Nicholas Dahir. 2023. “A New Alternative Minimum Tax for Canada?” Intelligence Memo. Toronto: C.D. Howe Institute. March.

Gagné-Dubé, Tommy, et al. 2021. “Policy Forum: The Real Concentration of Capital Gains in Canada – A Longitudinal Analysis.” Canadian Tax Journal. 69(4): 1175-1192. January.

Hossain, Belayet, and Laura Lamb. 2012. “Price Elasticities of Charitable Giving Across Donation Sectors in Canada: Is the Tax Incentive Effective?” International Scholarly Research Network. 2012(421789): 1-6. December.

Kesselman, Jonathan Rhys. 2023. “Pathways to reform of capital gains taxation in Canada.” Finances of the Nation Commentaries. 3(5): 1-68. March.

Organisation for Economic Co-operation and Development (OECD). 2023. “The taxation of labour vs. capital income.” OECD Taxation Working Papers. March.

Parliamentary Budget Office (PBO). 2023. “Changes to the Alternative Minimum Tax as Proposed in Budget 2023.” September.