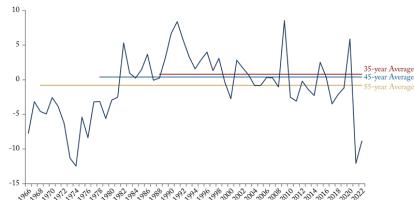

While the total mortgage bill for Canadian households as a percentage of disposable income has remained steady between 1990 and 2016, the shift from interest-dominant to principal-dominant payments means that households are more vulnerable.

In this edition of Graphic Intelligence we show the evolution of mortgage payments in Canada since 1990. As the graph above shows, the share of disposable income going towards mortgage payments has remained virtually unchanged, though its composition has not.

The result is increased risk to the economy since rising interest rates could increase total mortgage costs, and negative economic shocks can potentially be exacerbated by principal-dominant debt and housing wealth that may not be there to compensate.

To learn more about the impacts of these risks to household spending and how the Bank of Canada and governments at all levels should respond, read Spendthrifts and Savers: Are Canadians Acting Like they are “House Poor” or “House Rich”?