From: Alexandre Laurin

To: Finance Minister Chrystia Freeland

Date: October 13, 2021

Re: The Impact of Taxpayers’ Reaction to a Capital Gains Tax Increase

Government deficits have fueled calls for heavier taxation of capital gains in recent years. I estimated the increase in personal tax revenues from increasing the capital gains inclusion rate from its current 50 percent of gains to two thirds, three quarters, and 100 percent in the most recent issue of Perspectives on Tax Law & Policy.

Capital gains taxation distorts investor behaviour. First, capital owners tend to delay the sale of appreciated assets and thereby defer the accompanying tax liability – the so-called “lock-in effect.” Second, capital gains taxes can also discourage entrepreneurial activity and early-stage investing because they reduce the after-tax return from risky equity-financed investment on exit. The tax code’s partial inclusion rate attenuates these impacts by encouraging more investors from realizing accrued gains.

There is a rich literature quantifying the reaction of tax filers to capital gains tax increases. The response is measured through the elasticity of capital gains taxation – a measure of how changes in the rate affect capital gains realizations. For example, an elasticity of -0.5 would indicate that a 10-percent increase in the capital gain tax rate produces a 5-percent fall in capital gain realizations. The most influential elasticity results study the reaction of US taxpayers.

Jane Gravelle, a respected Congressional Research Office author and capital tax specialist, provides an excellent overview of US tax elasticity coefficients in a 2021 report. She reports the results of nine econometric studies, along with her own estimates and those by her office. All results are for a permanent, long-run reaction and thus exclude transitory effects of tax changes on realizations. The median elasticity, estimated at a 22-percent tax rate (the higher the tax rate, the greater the sensitivity), is -0.5. In other work, she concludes that this elasticity level should be the upper bound for tax analysts to use in evaluating the tax revenue response to rate changes. Consistent with her finding, a newer estimate found an elasticity ranging from -0.3 to -0.5.

But US elasticity estimates likely overstate the Canadian sensitivity because of the differing treatment of capital gains at death in both countries. Canadian economists opine that the magnitude of the permanent elasticity in Canada is probably small.

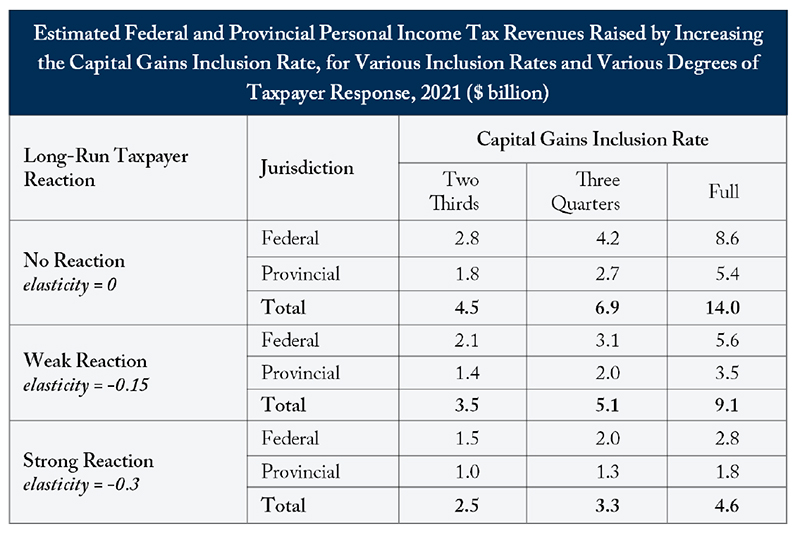

Using Statistics Canada’s Social Policy Simulation Database and Model, I estimate personal income tax revenue raised by a capital gains tax increase for three long-term elasticity scenarios: “no reaction,” “low reaction,” and “high reaction”.

The high reaction assumption is set at the lower response level used in the US (-0.3) to reflect Canada’s likely lower elasticity, while the low assumption is set at half of that value.

The “no response” scenario is unrealistic, but it is a useful benchmark. Raising the personal capital gains inclusion rate to two thirds, three quarters, or 100 percent would produce total estimated federal and provincial personal tax revenues of $4.5 billion, $6.9 billion, or $14 billion, respectively, assuming that taxpayers do not react.

A weak taxpayer reaction would reduce capital gains tax revenues raised by the increase from 23 to 35 percent, depending on the degree of the tax increases. A stronger taxpayer response would reduce revenues raised by 46 to 67 percent.

The greater the increase in the capital gains inclusion rate, the larger the impact of the taxpayer response.

Policymakers considering an increase in the capital gains inclusion rate should take behavioural responses into account. Even a weak taxpayer response would have a material impact on collections. Tomorrow, in a second part, we take a look at the income profile of capital-gains tax filers.

Alexandre Laurin is Director of Research at the C.D. Howe Institute.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the author. The C.D. Howe Institute does not take corporate positions on policy matters.