To: Canadian Fiscal Observers

From: Munir A. Sheikh

Date: January 30, 2024

Re: The Question isn’t “Do we need tax reform?” It is “What kind?”

Fifty years ago, the Carter Commission recommended comprehensive tax reform whose unifying vision was an ideal tax system. His principal objective was equity, followed by a secondary objective of the reform’s impact on the economy.

On equity, Carter believed: “The first and most essential purpose of taxation is to share the burden of the state fairly among all individuals and families.” And, according to Carter, this fair share was determined by: “If economic power is increased it does not matter in principle whether it was earned or unearned, from domestic or foreign sources, in money or in kind, anticipated or unanticipated, intended or inadvertent, recurrent or non-recurrent, realized or unrealized.”

Carter’s actual proposals deviated considerably from this academic view considering real-life constraints. For example, under his proposals: Capital gains tax was based on realization, rather than accrual, because of valuation and liquidity challenges, and taxation of imputed rents was not proposed because of the challenge of administering such a system (some politics too?).

Carter also developed a progressive personal income tax structure grounded in the view that non-discretionary expenditures were related to the level of income and family responsibilities and estimated functional relationships in that regard. While this sounds scientific, it is in fact arbitrary.

The 1971 reforms five years after the Carter report, which also used inputs from parliamentary committees and Canadians (through comments on the 1969 White Paper), further moved the needle away from the textbook understanding of an ideal tax system to a world of realism.

What is Carter’s legacy?

First, a more comprehensive tax base that included the taxation of capital gains for the first time. Second, improved integration of corporate and personal tax systems, but double taxation remains. Third, increases in exemptions and deductions to achieve social objectives such as retirement savings, charitable donations, childcare, employment, and moving expenses. And, finally, the exercise combined tax reform with tax cuts over several years to make tax changes palatable.

Many old tax issues haven’t gone away such as the double taxation of some forms of investment income, tax treatment of international income, which is a permanent challenge, and the taxation of capital gains. On the latter, some want a higher inclusion rate, a la Carter; others fret about the economic rationale for taxation (penalty on after-tax savings).

I would argue for two things: First, it is time for another round of tax reform; but, in contrast to Carter, we need to focus on the tax system’s negative impact on Canadian economic performance rather than strive for an ideal tax system. Another key difference would be a selective focus on major tax issues that likely affect economic performance, rather than a comprehensive review of the entire system.

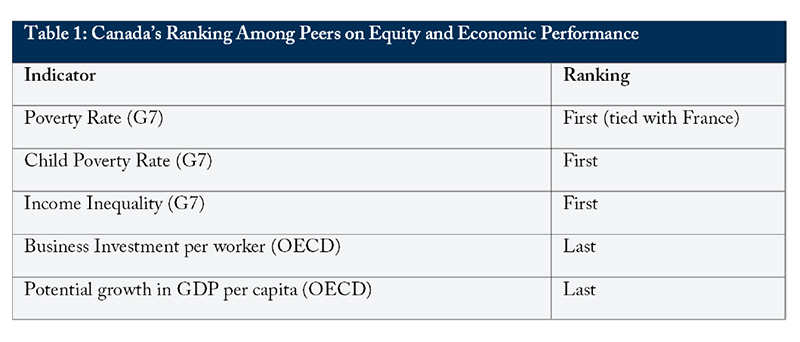

Table 1 clearly shows that, among its peers, Canada is at the top in achieving equity objectives and at the bottom, now and long into the future, in achieving desirable economic outcomes.

Source: Munir A Sheikh, Half a Century after Carter, paper presented at the C.D. Howe Institute Tax Reform Conference June 14-15, 2023.

Source: Munir A Sheikh, Half a Century after Carter, paper presented at the C.D. Howe Institute Tax Reform Conference June 14-15, 2023.

In view of this combination of our equity and economic outcomes, we need to look at our tax system and determine how it could contribute to better economic performance. As a starting point, we should implement changes that can improve economic outcomes without adversely affecting equity. Beyond that, we need to ask whether a shift is needed in the equity and productivity trade-off given our current extreme standings among our peers. Some candidates for an examination of key tax issues should include:

- The Tax mix: The carbon tax design for revenue neutrality should be changed to reduce the most distortionary taxes, unlike the current federal system. As well, there should be an increased reliance on HST and lower income taxes.

- Marginal effective tax rates: They could be over 100 percent at this time.

- Marginal tax rates: They have now reached 55 percent.

- Tax expenditures: They number over 275.

Beyond this, there is a need to establish a principles-based fiscal anchor, replacing the accounting-based anchors such as balanced budgets and debt-GDP ratios. That is needed to ease pressure on marginal tax rates to rise over time. The economics profession has no fiscal anchor grounded in economic principles. The accounting-based fiscal anchors are blown away in times of crisis, rather than serve as anchors.

One proposal is to develop an anchor I call “net economic public debt,” which is the difference between public debt and income-generating public investments. As I will outline tomorrow, its long-term value would be zero and it would fluctuate between positive and negative values during episodes of business cycles.

Munir A. Sheikh, former chief statistician of Canada is an adjunct research professor of economics at Carleton University.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the author. The C.D. Howe Institute does not take corporate positions on policy matters.