From: William B.P. Robson and Miles Wu

To: Canadians Concerned about Prosperity

Date: February 2, 2022

Re: Canada’s Investment Imperative: Stronger Business Investment. Can We Get It?

The Bank of Canada’s latest Monetary Policy Report, issued with its interest rate decision last week, highlighted the importance of business investment to Canada’s economy in two ways.

One was front and centre in the report. The Bank sees stronger investment as contributing to growth in 2022 and 2023 – as it conspicuously did not in 2020 and 2021.

The other was more subtle, but vital. How fast spending can grow over time without producing more inflation and triggering painful increases in interest rates depends on business investment’s ability to raise productivity and potential growth – this year, in 2023, and for years to come.

We want the Bank’s prediction of stronger business investment to come true. Near term, more investment will support output and jobs – all the more important if consumers flag and governments acknowledge limits to their spending and borrowing. Longer term, investment equips Canadian workers to raise their output. A growing stock of machinery, buildings, engineering infrastructure and intellectual property products means workers are getting more tools that let them produce, compete and earn higher wages. That is good for all kinds of reasons – among them, that faster-growing productive capacity makes it easier for the Bank to get inflation back to 2 percent.

And the Bank’s prediction might come true. Demand is growing as we and the rest of the world recover from COVID. Workers are scarce. Interest rates are still low. The Bank’s survey shows that businesses plan to invest.

But other indicators point in a less happy direction. The C.D. Howe Institute’s monitoring of the business capital stock per member of Canada’s workforce shows a decline – not just since COVID hit, but going all the way back to 2015. That means less productive capacity per worker, which is a key reason why surging spending since early 2020 has resulted in less real growth, and more inflation, than we expected or wanted.

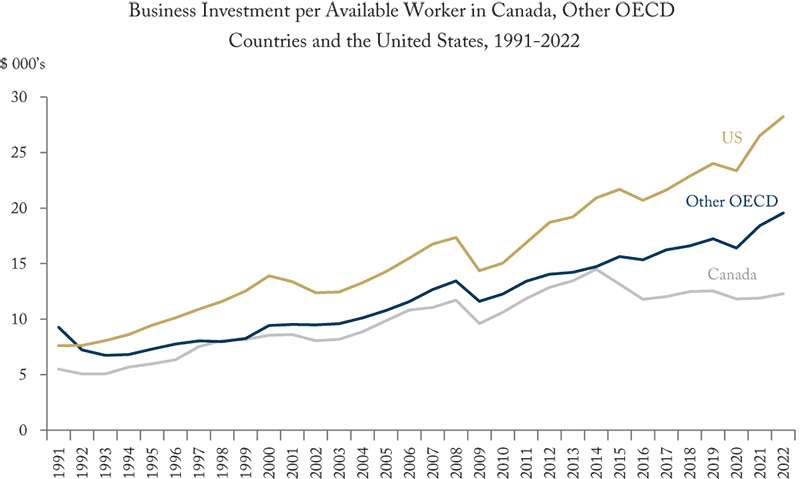

Worse, weak investment is a peculiarly Canadian problem. Data from the Organization for Economic Co-operation and Development (OECD)’s December 2021 Economic Outlook suggest that businesses in Canada invested about $12,000 per available worker last year. By contrast, businesses in other OECD countries, excluding the United States, invested about $18,000 per available worker. US businesses invested almost $27,000 per available worker.

That means that, for every dollar of new capital enjoyed by the average worker in the entire OECD in 2021, the average Canadian worker enjoyed only 56 cents. And for every dollar of new capital enjoyed by the average US worker, Canadian workers enjoyed only 46 cents – less than half as much.

The OECD also expects an uptick in investment in 2022. Their data suggest that Canadian business will invest some $13,100 per available worker this year. More is better, but this is not nearly enough to close the gap with other countries. The same numbers suggest that businesses in other OECD countries, excluding the United States, will invest about $19,600 per available worker, and business in the United States will invest about $28,400 per available worker.

These numbers tell us that other countries, most notably the United States, have better prospects for immediate recovery from the COVID-induced recession. Canada is one of just two OECD countries where business investment per available worker is lower than it was six years ago. These numbers also tell us that other countries, again, most notably the United States, have better prospects for long-term growth. Their workers will enjoy faster increases in productivity and wages. And their economies can grow faster without more inflation – and with interest rate increases smaller than the Bank of Canada may need to impose to get inflation down again.

How can we improve our prospects? A good start would be to change what has not been working. Canada’s federal government has stoked demand with unprecedented peacetime spending and borrowing. That has boosted consumption – but it has also boosted inflation, and contributed to a sense that policymakers care far more about immediate gratification than they do about long-term prosperity. We should also remember that the decline in our capital stock per worker predated COVID. It started in 2015, after more than a decade during which we narrowed the gap between investment per worker in Canada and investment per worker in other countries.

More investment-friendly tax, trade and regulatory policies worked before. They can work again. They would help business investment in Canada realize the promise in the Bank’s Monetary Policy Report. Canadian workers will get the capital and technology they need to prosper. And Canada’s economy can grow faster, with less threat of inflation, and less prospect of a painful tightening of monetary policy.

William B.P. Robson is CEO of the C.D. Howe Institute, where Miles Wu is a Research Assistant.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the authors. The C.D. Howe Institute does not take corporate positions on policy matters.