February 25 – Budget debate anxiety over cities’ fiscal health tells a misleading story, according to a new report from the C.D. Howe Institute. In fact, Canada’s biggest municipalities were in robust health in the run-up to 2020. The 31 largest by population tallied an aggregate surplus of over $10 billion in 2019.

In “Puzzling Plans and Surprise Surpluses: Canada’s Cities Need More Transparent Budgets,” William B.P. Robson and Miles Wu look at the annual budgetary projections for spending and the bottom line in the 31 municipalities over a decade (2010 to 2019) and compare them to the results reported in those municipalities’ year-end financial statements.

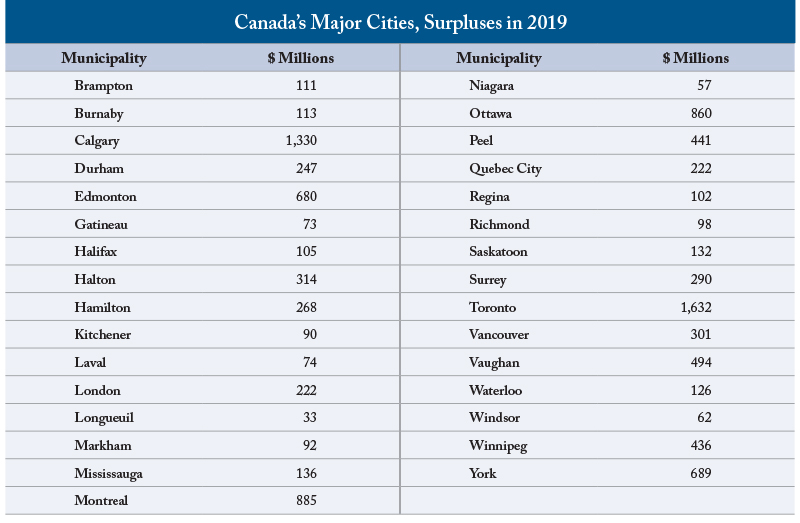

Their financial statements reveal that Canada’s biggest cities and municipalities ran large surpluses, with Toronto leading the pack with a $1.6 billion surplus, followed by Calgary at $1.3 billion. Montreal’s surplus was $884 million, and Ottawa’s $860 million.

“Canada’s cities went into the troubles of 2020 in much better fiscal shape than is commonly appreciated,” said Robson. “That is good. What is less good is that these surpluses are completely at odds with peoples’ understanding and the anxiety of the budget debates. More transparent budgets would enhance Canadians’ confidence in their cities’ finances.”

In most of these 31 municipalities, the authors contend, simply finding comparable numbers about spending plans is tough. Less than one-half of them produce budget documents with numbers presented on the same basis – using public sector accounting standards (PSAS) – as the presentation in their year-end financial statements.

Readers of non-PSAS budgets who compared spending plans to the expenses reported after year-end would typically conclude that the budget projections were badly at variance with the results – with a difference averaging 7.6 percent annually over the 10 years. In most cities, presenting budgets with non-PSAS accounting is a major contributor to these discrepancies. Critically, such municipal budgets show investments in capital assets like buildings, sewers and transit on a cash, upfront basis while the financial statements amortize the cost over years. Comparing budgets on a PSAS basis to year-end results yields an average annual gap between plans and outcomes that is considerably smaller: 3.9 percent. Robson and Wu observe that if cities used the same accounting in budgeting as in reporting, they would likely invest more in infrastructure, and match taxes to services delivered better than they do now.

Robson and Wu urge all municipalities to highlight the same PSAS-consistent revenue, expense and bottom-line numbers in their budgets that they already use in their financial statements. Other information – notably separate operating and capital budgets and other information mandated by provinces or demanded by voters can still appear in budgets, but the PSAS-consistent numbers would provide a fuller picture of their municipality’s activities and costs, and facilitate comparisons between budgets and results.

For more information contact: William B.P. Robson, CEO; Miles Wu, Research Assistant; or David Blackwood, Communications Officer, the C.D. Howe Institute, 416-873-6168, dblackwood@cdhowe.org

The C.D. Howe Institute is an independent not-for-profit research institute whose mission is to raise living standards by fostering economically sound public policies. Widely considered to be Canada's most influential think tank, the Institute is a trusted source of essential policy intelligence, distinguished by research that is nonpartisan, evidence-based and subject to definitive expert review.