Summary

The key argument in favour of an Intellectual Property (IP) Box, which taxes the income generated from intellectual property at a special low rate, is that it defends against poaching of highly mobile IP income by low-tax jurisdictions, particularly tax havens. The standard response to this argument has been that IP Boxes will intensify competition for mobile tax bases, which will eventually drive the tax rate on IP income to zero.

However, this counterargument has lost its force because of the general acceptance that preferential tax treatment must be linked to real activity in the implementing jurisdiction and because of the tentative agreement on a global minimum corporate tax rate. With these two developments, an IP Box protects the tax base without engendering tax competition for highly mobile IP income.

An IP Box has two other advantages in the current environment: it encourages additional investment in research and development (R&D) and commercialization activity in the implementing jurisdiction.

There are two key design features that must be adopted to maximize the benefits of an IP Box.

- First, income from all assets developed from R&D performed in Canada, not just patents, must qualify for special treatment.

- Second, qualifying income must include not only explicit royalties and licensing fees, but also implicit IP income embedded in products sold, or in production processes developed from R&D performed in Canada.

A carefully designed IP Box is likely to be a more cost-effective way of promoting innovation by large firms than an increase of equivalent value in the regular Scientific Research and Experimental Development (SR&ED) investment tax credit. The impacts on R&D are likely to be similar, but the fiscal cost would be smaller because of a reduction in outbound profit shifting.

Introduction

An IP Box provides a lower corporate income tax rate on income from patents and other intellectual property.

Without this linkage, or nexus, between preferential income taxation and real activity, IP Boxes can be used to compete for highly mobile income from intellectual property. As a result, IP regimes without a nexus requirement were considered harmful tax practices in the OECD/G20 Base Erosion and Profit Shifting (BEPS) project (OECD 2015).

The Case for an IP Box

The key argument in favour of an IP Box is that it defends against “poaching” of highly mobile IP income by low tax jurisdictions, particularly tax havens. The standard reply to this argument has been that competitive pressures may eventually drive the preferential tax rate down to zero, with harmful consequences for all countries where IP assets are developed. However, this counterargument has lost its force because of the general acceptance of the nexus requirement, which effectively prevents using a preferential tax rate to compete for IP income, and because of the tentative agreement on a global minimum tax rate. With these two developments, an IP Box becomes a second-best method of taxing highly mobile IP income.

There is empirical evidence to support the proposition that a preferential tax regime for IP income reduces profit shifting out of the implementing jurisdiction. Chen et al. (2016) examine the impact of innovation boxes on profit shifting and on real activity using data from western European subsidiaries of European and US multinational enterprises (MNEs). They find some evidence of a reduction in profit shifting when innovation boxes are introduced as well as an increase in employment and wages. Using data on European patents over the 1981 to 2014 period, Gaessler, Hall, and Harhoff (2021) find that preferential tax treatment substantially reduces transfers of patents, and ultimately income, out of the implementing jurisdiction.

A second argument in favour of an IP Box is that it will encourage additional investment in R&D by raising the after-tax return on successful R&D projects. The empirical evidence offers some support for this proposition. In addition to the evidence provided by Chen et al. (2016) discussed above, Mohnen, Vankan, and Verspagen (2017) report that the Dutch patent box had a positive impact on the person-hours allocated to R&D by participating firms. Schwab and Todtenhaupt (2021) examine how multinational firms active in Europe during the 2000-2012 period responded to implementation of a patent box in one of the jurisdictions in which they operate. The authors find that firms increase their patent output in response to the reduction in the after-tax cost of investing in R&D arising from implementation of a patent box.

A third argument in favour of an IP Box is that it can encourage additional commercialization activity. For this to occur, however, all income from qualifying IP assets must qualify for special treatment. Firms with royalty income and other explicit returns to IP assets developed from R&D performed in Canada would not need to undertake commercialization activity in Canada to benefit from the preferential rate. It would be sufficient to book the royalty income in Canada. In contrast, if the return to IP assets is embedded in the price of products sold, the preferential rate can only be accessed if the real activity takes place in Canada.

Additional commercialization activity has several potential benefits. Pantaleo, Poschmann, and Wilkie (2013) draw attention to how co-locating R&D and commercialization activities can lead to favourable agglomeration effects. Many commentators focus on the quality of jobs – particularly relatively high wages – created by innovative firms, implicitly suggesting that subsidy-induced changes in the composition of employment will raise overall income. Balsillie (2021), chair of the Canadian Council of Innovators, highlights the role of above-normal profits, or rents,

The “good jobs” approach contrasts with the conventional economic analysis that market forces allocate capital and labour to their best uses, which implies that policy-induced shifts in the composition of output cannot raise real income. However, markets deviate from the competitive ideal, leaving open the possibility that policy-induced shifts in real activity will improve economic performance. There is abundant evidence of large and persistent productivity differentials across firms in the same industry that are observably similar.

Although none of the evidence is based on an analysis of R&D-intensive firms, it is plausible to argue that a policy-induced increase in commercialization activity in Canada would raise productivity and hence incomes in Canada. However, some caution is appropriate. Card et al. (2018) find evidence that high-productivity firms hire more productive workers and pay wage premiums to all workers, but state that more analysis is required before they could recommend that governments pursue industrial policies in a bid to raise national income. It is difficult to identify firms that are earning rents. Relatively high wages may reflect skill differences rather than rents being shared, and relatively high profits may include compensation for risk. Further, even if some R&D-intensive firms are earning rents and are sharing them with workers, an expansion of the sector may draw workers and capital from other firms that are also earning above-normal profits.

A Comparison with the SR&ED investment tax credit

In contrast to the SR&ED investment tax credit, which is payable when the R&D is performed, the tax benefit from an IP Box is paid only if the R&D has been successfully commercialized. Firms performing R&D do not expect all projects to be successful, so the hurdle rate for investing rises to compensate for unsuccessful projects. An IP Box therefore implicitly subsidizes all R&D performed, not just successful projects. The question remains, however: do firms react the same to an incentive received before they make an investment (ex ante) as to ex post incentives that have the same present value? Both measures raise the expected return on R&D investment by a known amount, so unless a firm is credit-constrained they should have the same impact on investment. Large firms are likely to be able to finance investment with internal cash flow or by accessing financial markets. In contrast, many start-ups and small firms would respond less strongly to an ex post incentive because of limited cash flow and limited access to financial markets.

An IP Box could affect the composition of investment by, for example, restricting the type of IP asset that would qualify for a tax preference. The reduction in the tax rate could also affect the composition of investment. Loss offset provisions (e.g., carry forwards) in the corporate income tax system cause governments to share in both profits and losses. This reduces the variance of returns, which may increase risk-taking. Empirical studies, for example Langenmayr and Lester (2017), find that risk taking rises with the corporate income tax rate. The lower IP Box rate would therefore encourage a shift in R&D spending to lower risk projects.

Not all analysts expect a strong response of R&D to an IP Box. For example, Gaessler, Hall, and Harhoff (2021) conclude that Patent Boxes are a “relatively inefficient” way of stimulating inventive behaviour. This conclusion reflects in part the assumption that only income from patented inventions would be eligible for preferential treatment. Allowing all IP income to be taxed at a lower rate eliminates the incentive to favour patented inventions over other inventions.

The analysis in this section suggests that a preferential tax rate on IP income is likely to be a more cost-effective way to promote innovation by large firms than an equivalent increase in the SR&ED investment tax credit. Cost effectiveness is defined here as the net social benefit per dollar of tax revenue forgone while the net social benefit is defined as the increase in aggregate real income arising from the policy initiative. Knowledge spillovers arising from R&D are an unambiguous social benefit and are likely to be similar per dollar of additional R&D for both measures. An IP Box will be more costly to administer and comply with relative to program benefits than an increase in the SR&ED credit (Box 1) while the other social costs are likely to be similar for both measures. However, the lower fiscal cost of a patent box is highly likely to tip the balance in its favour. The additional commercialization activity arising from an IP Box could provide a further advantage. Since the SR&ED investment tax credit ranks highly in terms of cost effectiveness among economic development subsidies (Lester 2018), an IP Box is certain to compare favourably to other business subsidies.

The benefit-cost analysis presented in Lester (2021) indicates that support for R&D performed by large firms is below its optimal level, which means that additional support would increase the net social benefit.

| Box 1: IP Box Compliance Costs

|

|---|

|

Relatively high compliance costs of IP Boxes are a potential concern. Participants in the preferential IP income regime will have to implement a tracking and tracing regime to demonstrate that income earned is linked to R&D performed and that only qualifying IP income benefits from the preferential tax rate. Identifying embedded income could be particularly burdensome. Fortunately, Canada will be able to benefit from experience in Quebec and other jurisdictions when implementing an IP Box. Complying with the reporting requirements of an IP Box absorbs resources that could have been used productively elsewhere, which reduces the net social benefit of the preferential regime. There is no evidence available on compliance costs for IP Boxes. However, average compliance costs for the regular SR&ED tax credit provide a useful benchmark. These compliance costs represent 4.6 percent of tax credits claimed (Lester 2012) and reduce the SR&ED subsidy rate by the same percentage. |

Choosing the Preferential Rate

The preferential rate on IP income should be set low enough to discourage outbound profit shifting and to make Canada an attractive location for commercialization activities. Almost all the 140 members of the OECD/G20 Inclusive Framework on BEPS, including all tax havens, have agreed in principle to impose a 15 percent minimum corporate tax rate on large MNEs, with a target effective date of 2023 (OECD 2021).

A preferential tax rate on IP income is also intended to affect the location of commercialization activity. Canada’s key competitor for commercialization activity is the US. The relevant comparison tax rate when assessing where to invest to serve the US market is about 26 percent, the combined federal-state rate.

Nevertheless, the IP Box rate should be aligned with the global minimum tax rate. The preferential rate could be set slightly higher than the minimum. Profit shifting could be eliminated with a rate above 15 percent because firms incur costs, including reputational risk, setting up and maintaining the infrastructure required to shift profits (Pantaleo, Poschmann, and Wilkie 2013, 5). However, the tipping point for eliminating profit shifting will be pushed down by the costs incurred by firms to participate in the preferential IP regime.

Federal-provincial Issues

Achieving the target rate through federal action has two key advantages over relying on provincial initiatives. A national program would not create barriers to the interprovincial mobility of R&D, which would arise if provincial programs include a provincial nexus requirement. A national program would also result in lower administration and compliance costs. A federal program could be implemented as a tax credit or as a deduction from taxable income. If the federal government implemented a preferential IP regime with a tax credit, it would bear the entire cost of the program. In addition, provincial governments would receive a windfall tax revenue gain from the reduced outflow of IP profits.

In contrast, implementing the IP Box as a deduction would de facto constrain all provinces except Alberta and Québec to participate in the federal initiative. (Other provinces have signed tax collection agreements that require them to use the same tax base as the federal government.) The federal government could reduce the combined tax rate on IP income in tax collection provinces from about 27 percent to about 16.5 percent by providing a 40 percent deduction from IP income. Saskatchewan already has a preferential regime that reduces the IP income tax rate to 6 percent. With a 40 percent reduction in the tax base, the combined federal-Saskatchewan rate on IP income would be about 13 percent. This is likely to be below the revenue-maximizing rate, so Saskatchewan would have an incentive to raise its preferential IP rate.

Participation by Alberta and Quebec, which have not signed tax collection agreements, would be optional. No special considerations arise for Alberta, but Quebec also has a preferential IP regime. Quebec’s regime taxes selected IP income earned in Quebec at 2 percent, a 9.5 percentage point rate reduction from the standard rate for large firms. If the federal government provided a 40 percent deduction, reducing the federal rate to 9 percent, the combined rate in Quebec would fall to 11 percent. Quebec would have an incentive to increase its preferential rate, particularly if the effective tax rate on some MNEs operating in the province were to fall below 15 percent.

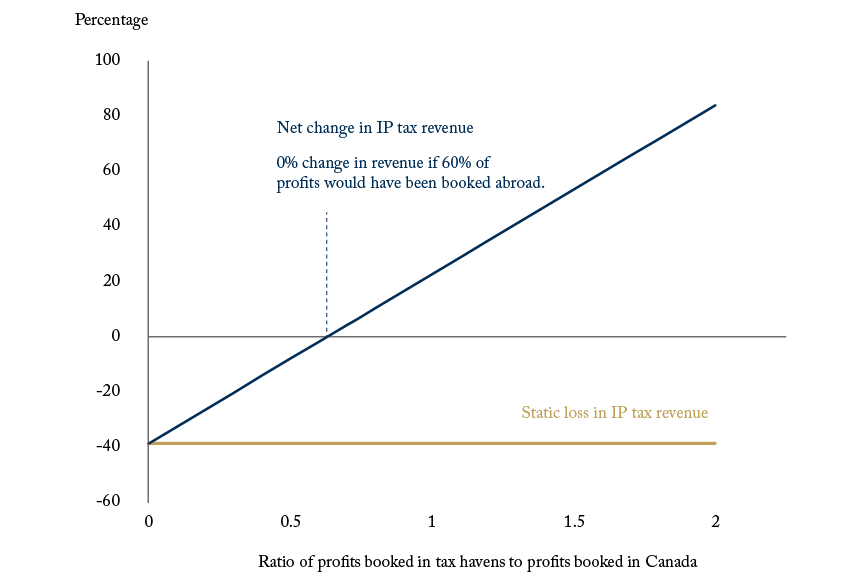

If reducing the tax rate on IP income to 16.5 percent is low enough to eliminate IP profit shifting, the impact on the fiscal cost of the preferential regime could be substantial. The net fiscal cost is the loss of tax revenue on IP profits booked in Canada less the revenue gain on profits that would have been shifted to other jurisdictions.

In the absence of a global minimum tax, Canada’s key competitor for mobile IP income would be Barbados. The corporate income tax rate schedule in Barbados is regressive. The rate on the first million Barbados dollars (C$630,000) of taxable income is 5.5 percent, falling to 1 percent for taxable income exceeding 30 million Barbados dollars (C$19.7 million). In addition, Barbados has a tax treaty with Canada that facilitates profit shifting.

Figure 1: Percentage Change in Tax Revenue Arising from an IP Box

Federal Government and Tax Collection Agreement Provinces – 10.4 Percentage Point Rate Reduction

Source: Author’s calculations based on assumptions about where IP profits are booked.

Other Design Features of an IP box

The 2015 OECD report on harmful tax practices (OECD 2015) sets out guidance for determining the income that may be taxed at a preferential rate (Box 2). The guidance is flexible enough to capture virtually all the income generated from successful R&D projects. The OECD recommendations have been almost universally accepted.

In addition to requiring a linkage to R&D performed in Canada, a well-designed IP Box would apply the preferential tax rate to the income that arises from all assets created by performing R&D, as permitted in the OECD guidance. IP income is both explicit, arising from royalties and other licensing arrangements, and implicit, arising from the in-house commercialization of IP and from IP assets used to reduce in-house production costs.

| Box 2: OECD Guidance on Preferential IP Regimes

|

|---|

|

Intellectual property assets qualifying for preferential treatment comprise patents and other assets that are functionally equivalent to patents. The OECD guidelines specifically mention copyrighted software, utility models, protection granted to plant and genetic material, orphan drug designations, and extensions of patent protection as assets that are functionally equivalent to patents. Correspondence with OECD officials has confirmed that this list is not exhaustive. Notably, assets developed from R&D and protected by trade secrecy are qualified assets. This is an important consideration because a substantial fraction of inventions is protected by trade secrecy and such assets can be assigned or licenced to other parties, much like patents. The broad definition of qualifying assets is, in principle, particularly beneficial for smaller firms who have a lower propensity to patent inventions. However, it may be difficult for smaller firms to demonstrate that assets not protected by patents qualify for preferential treatment. As a result, inventions by smaller firms that could be patented (i.e., they embody ideas that are non-obvious, novel, and useful) may be certified as qualifying assets by a government agency that is independent of the tax administration. In Canada, inventions resulting from R&D can be protected by patents, data protection for innovative (orphan) drugs under the Food and Drug regulations, Certificates of Supplementary Protection for patented drugs, software copyright, plant breeders’ rights, and trade secrecy. It is therefore reasonable to conclude that all successful R&D projects will result in qualifying IP assets. Note that while copyrighted software, which is generally the result of R&D, is a qualified asset, other copyrighted assets are not. Marketing-related assets such as trademarks are not considered qualifying IP assets since they are not developed from R&D. Income derived from qualifying assets may include royalties, capital gains and other income from the sale of the asset, and “embedded” income from the sale of products and the use of processes directly related to the qualifying IP asset. Income qualifying for the preferential rate must be net of expenditures incurred in the same year to earn that income. The nexus requirement is implemented by applying the share of qualifying expenditures on R&D in total R&D expenditures to qualifying income. Jurisdictions may adopt their own definitions of qualifying expenditures, subject to the general constraint that they include only the types of spending that typically qualify for R&D tax credits. R&D outsourced to unrelated parties may be included in qualifying expenditures. In addition, a portion of the cost of acquiring IP assets and R&D outsourced to related parties may be included in qualifying expenditures. The adjustment is capped at 30 percent of qualified R&D spending, with the further constraint that the nexus ratio cannot exceed unity. However, jurisdictions outside of the European Union may include all R&D outsourced to related parties resident in the implementing jurisdiction. The modified nexus guidance contains provisions to prevent disadvantaging firms that undertake R&D that cannot be linked to a specific IP asset. The nexus ratio can be increased by including “general and speculative R&D” in qualifying spending on R&D as well as in total R&D. Without this adjustment, the nexus ratio would decline and only part of income from IP assets would benefit from a lower tax rate for firms undertaking general and speculative R&D. |

Implicit IP income is described as “embedded” IP income in the OECD guidance. Excluding embedded income from preferential treatment would cause distortions in the type of R&D undertaken and affect the decision to protect intellectual property with patents or by other means.

The OECD guidance allows some exceptions to the nexus requirement. For jurisdictions outside of the European Union:

- R&D outsourced to unrelated parties may be included in qualified spending, while R&D outsourced to related parties may be included only if the performer is in the implementing jurisdiction.

- Acquired IP and R&D outsourced to related parties not in the implementing jurisdiction can be included in qualifying expenditures, capped at 30 percent of otherwise qualifying R&D spending.

Consistent with the SR&ED tax incentive, qualified spending should include only R&D performed in-house or outsourced to unrelated parties resident in Canada. Acquired IP should qualify only if it is developed from R&D performed in Canada. Further, since income from the sale of the asset would be taxed at a preferential rate, allowing the purchaser of IP developed in Canada to benefit from the lower rate would amount to double-dipping. Either the seller or the buyer should benefit from the preferential tax regime, but not both.

The OECD guidance requires that the preferential rate be applied to qualifying income net of expenses incurred in the same year. Expenses incurred during the commercialization phase are therefore deducted at the incentive rate

There is no OECD guidance on the treatment of existing IP. Countries may choose to include existing IP in qualifying assets or to link qualifying IP to R&D performed after the implementation date. The impact on R&D will not change with the inclusion of existing IP. However, there will be a windfall tax reduction on IP profits booked in Canada and a tax revenue gain on repatriated IP profits. If profits from newly created IP are shifted abroad in the same proportion as profits from existing IP, including existing IP will raise the absolute value of the net fiscal cost or gain by a constant multiple as the ratio of profits shifted abroad rises relative to domestic profits.

| Box 3: Effective R&D Subsidy Rate from an IP Box

|

|---|

|

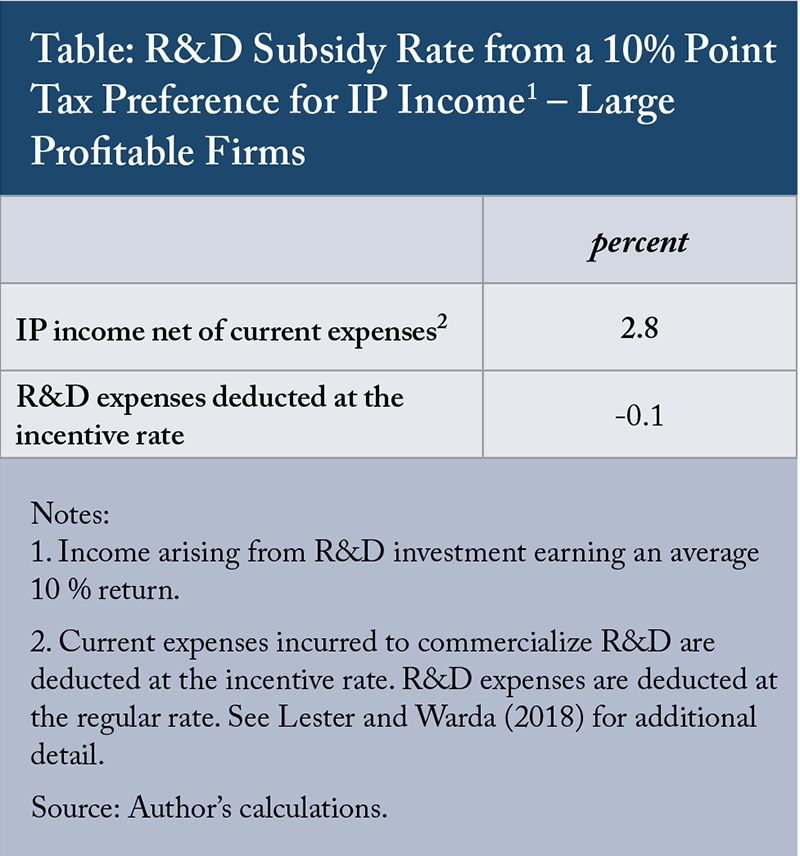

An IP Box implicitly subsidizes R&D by reducing the tax rate applied to the income it generates. Lester and Warda (2018) develop a methodology to calculate this implicit subsidy in a user cost of capital framework. Assuming a 10 percent average rate of return on R&D investment, a two-year lag between performing the R&D and receiving commercialization income, and that the tax preference applies to all IP developed from R&D, a 10 percentage point tax preference for IP income would reduce the user cost of R&D capital by 2.8 percent (see Table). Assuming the average rate of return on R&D is 15 percent rather than 10 percent increases the implicit subsidy rate to 3.2 percent. By way of comparison, the federal 15 percent investment tax credit available to large firms reduces the user cost of R&D capital 12.1 percent. The calculation is made for profitable firms for both measures. The Table also shows that deducting R&D expenses at the incentive rate rather than the regular corporate income tax rate would eliminate the implicit subsidy. Immediate deductibility of R&D expenses reduces the user cost of R&D capital 8.6 percent when net income is taxed at the regular rate of 26.2 percent. A 16.2 percent incentive rate reduces the benefit of expensing by 2.9 percentage points after adjusting for the time lag in applying the incentive rate. |

How should small firms be included in the preferential regime?

Small businesses should be encouraged to participate in the preferential IP regime by adopting the simplified approach permitted under the OECD guidance to determining qualifying IP assets for small firms. Some small firms could benefit from both an IP Box and the enhanced SR&ED tax credit (Box 4). Since support for small firms now exceeds the socially optimal level, the extra benefit should be offset by a reduction in the rate for all recipients of enhanced benefits.

Conclusion

An IP Box would encourage firms to undertake more R&D and to commercialize more of it in Canada. If the tentative agreement to set a global minimum corporate income tax rate is ratified by enough countries, setting the preferential rate at or slightly above the global minimum rate could eliminate outbound shifting of IP profits, which would substantially reduce the fiscal cost of the IP Box. A national program would be more efficient than separate provincial initiatives. Further, since provincial governments would receive a windfall revenue gain from decreased outbound profit shifting, there is a strong case for the federal government to implement an IP Box using a deduction, which would reduce the tax base of provinces that have signed a tax collection agreement with the federal government. Participation by Quebec and Alberta, which have not signed tax collection agreements with the federal government, would be at their discretion.

| Box 4: Including Small Firms in the Preferential IP Regime

|

|---|

|

Firms with up to $10 million in capital are eligible for a refundable 35 percent federal SR&ED investment tax credit. This enhanced rate is reduced to the regular 15 percent as capital rises to $50 million. Firms with up to $10 million in capital and $500,000 in net income benefit from the special low income tax rate for small business, which is phased out as capital rises from $10 to $15 million. Firms that receive the enhanced SR&ED tax credit while paying the general corporate income tax rate would benefit from an IP Box, while firms paying the special low rate, which averages 11.7 percent including both federal and provincial taxes, would not. The benefit-cost analysis presented in Lester (2021) shows that adding to the already high level of support for R&D performed by small firms would harm rather than help economic performance. A second issue is whether small firms (i.e., firms not paying the general corporate income tax rate) should be encouraged to participate in the preferential regime. One way to encourage participation would be to adopt the OECD guidance allowing firms with less than $11 million in revenue to use a less rigorous method than large firms to determine qualifying IP assets (Box 2). However, increased participation by small firms may not pass a benefit-cost test. Small firms are less likely than large firms to increase R&D spending in response to a backend subsidy and profit shifting would not reduce the fiscal cost of the tax preference. On the other hand, increased participation would encourage additional commercialization, in part by making takeover targets less likely to leave Canada. Adopting the OECD guidance could be seen as a quid pro quo for reducing the enhanced SR&ED rate. Another way to encourage small firms to participate in the preferential regime would be to further reduce the special low income tax rate for small business as it applies to IP income. This initiative does not have much to recommend it. In general, small firms are less likely than large firms to adjust R&D spending in response to a back-end subsidy and the low cap on the income eligible for the small business rate further weakens this response. |

In addition to aligning the preferential rate with the global minimum tax rate, the cost effectiveness of an IP Box will be maximized if:

- Qualified spending includes only R&D performed in-house or outsourced to unrelated parties resident in Canada and acquired IP developed from R&D performed in Canada.

- Income from all IP assets created from R&D, not just patents, qualifies for the preferential rate.

- Embedded IP income qualifies for the incentive rate.

- There is no recapture of R&D deductions.

A carefully designed IP Box would be a more cost effective way to stimulate innovation by large firms than an increase of equal value in the regular SR&ED investment tax credit. However, increased support for innovation by larger firms would be good public policy, so the IP Box should be implemented without reducing the regular SR&ED tax credit.

References

Balsillie, Jim. 2021. “Testimony to the Standing Committee on Industry, Science and Technology.” House of Commons. https://www.ourcommons.ca/DocumentViewer/en/43-2/INDU/meeting-32/eviden….

Boadway, Robin, and Jean-Francois Tremblay. 2017. “Policy Forum: The Uneasy Case for a Canadian Patent Box.” https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2962318.

Card, David, Ana Rute Cardoso, Joerg Heining, and Patrick Kline. 2018. “Firms and Labor Market Inequality: Evidence and Some Theory.” Journal of Labor Economics 36 (S1): S13–70.

Chen, Shannon, Lisa De Simone, Michelle Hanlon, Rebecca Lester, and others. 2016. “The Effect of Innovation Box Regimes on Income Shifting and Real Activity.” http://web.stanford.edu/~lnds/CDHL_7_25_2016.pdf.

Evers, Lisa, Helen Miller, and Christoph Spengel. 2015. “Intellectual Property Box Regimes: Effective Tax Rates and Tax Policy Considerations.” International Tax and Public Finance 22 (3): 502–30.

Gaessler, Fabian, Bronwyn H. Hall, and Dietmar Harhoff. 2021. “Should There Be Lower Taxes on Patent Income?” Research Policy 50 (1): 104129.

Green, David A. 2015. “Chasing after “Good Jobs.” Do They Exist and Does It Matter If They Do?” Canadian Journal of Economics/Revue Canadienne d’économique 48 (4): 1215–65.

Klemens, Ben. 2016. “A Boxing Match: Can Intellectual Property Boxes Achieve Their Stated Goals?” Browser Download This Paper. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2822575.

Langenmayr, Dominika, and Rebecca Lester. 2017. “Taxation and Corporate Risk-Taking”. The Accounting Review 93 (3): 237–66. https://doi.org/10.2308/accr-51872.

Lester, John. 2018. “Tax Incentives for Business Investment: Do They Work?” In Reforming the Corporate Tax in a Changing World, edited by Bev Dahlby, 259. Canadian Tax Foundation and the School of Public Policy, Calgary.

__________. 2021. “Benefit-Cost Analysis of Federal and Provincial SR&ED Investment Tax Credits.” University of Calgary School of Public Policy Research Paper 14 (1). https://www.policyschool.ca/wp-content/uploads/2021/01/Tax-Credits-Lester.pdf.

Lester, John, and Jacek Warda. 2020. “Enhanced Tax Incentives for R&D Would Make Americans Richer.” Information Technology & Innovation Foundation. https://itif.org/publications/2020/09/08/enhanced-tax-incentives-rd-would-make-americans-richer.

Mohnen, Pierre, Arthur Vankan, and Bart Verspagen. 2017. “Evaluating the Innovation Box Tax Policy Instrument in the Netherlands, 2007–13.” Oxford Review of Economic Policy 33 (1): 141–56.

OECD. 2015. “Countering Harmful Tax Practices More Effectively, Taking into Account Transparency and Substance, Action 5 – 2015 Final Report, OECD/G20 Base Erosion and Profit Shifting Project.” Organisation for Economic Co-operation and Development Publishing, Paris France. https://www.oecd-ilibrary.org/docserver/9789264241190-en.pdf?expires=1637150916&id=id&accname=guest&checksum=0E823AB3DBCAB6114755AB0D1B0A298B.

———. 2021. “Statement on a Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy.” https://www.oecd.org/tax/beps/statement-on-a-two-pillar-solution-to-address-the-tax-challenges-arising-from-the-digitalisation-of-the-economy-october-2021.pdf.

Pantaleo, Nick, Finn Poschmann, and Scott Wilkie. 2013. Improving the Tax Treatment of Intellectual Property Income in Canada. Commentary 379. Toronto: C.D. Howe Institute. http://papers.ssrn.com/sol3/Delivery.cfm?abstractid=2303819.

Schwab, Thomas, and Maximilian Todtenhaupt. 2021. “Thinking Outside the Box: The Cross-Border Effect of Tax Cuts on R&D.” Journal of Public Economics 204: 104536.