The Study in Brief

- In the fall of 2023, the Alberta government released a report proposing the creation of an Alberta Pension Plan (APP) funded initially by the province’s withdrawal from the Canada Pension Plan, taking with it $334 billion in assets.

This E-Brief examines the financial assumptions of the proposed APP, assesses their reasonableness, and outlines the risks and consequences of the departure for Alberta and other provinces. First, it outlines some basic aspects of the CPP that are relevant to the possibility of Alberta leaving the CPP. Then, it examines the financial consequences of the claim, both for the new APP and the truncated CPP. Finally, it offers thoughts on the risks an APP might face, assuming the province withdraws a more reasonable amount from the CPP.

This E-Brief examines the financial assumptions of the proposed APP, assesses their reasonableness, and outlines the risks and consequences of the departure for Alberta and other provinces. First, it outlines some basic aspects of the CPP that are relevant to the possibility of Alberta leaving the CPP. Then, it examines the financial consequences of the claim, both for the new APP and the truncated CPP. Finally, it offers thoughts on the risks an APP might face, assuming the province withdraws a more reasonable amount from the CPP.

- Among the findings: 1) The numbers don’t add up. If other provinces use the same rationale for Alberta’s current proposed withdrawal, the claims on CPP assets would be more than 100 percent. 2) Alberta’s tally of contributions made minus benefits paid to its citizens ignores labour mobility. People can work in Alberta and make contributions there but later move to another province and collect benefits there. 3) Alberta’s demographics, with its younger, higher-earning workforce, are now favourable to keeping contribution rates relatively low. But over decades, demographics can change significantly, undercutting the province’s assumptions about future contributions. 4) Finally, there are major unanswered questions about the governance of the APP.

- The author concludes that the creation of an APP will involve taking on a good deal of risk for relatively small gains that are uncertain over the long term.

- The debate over whether Alberta should withdraw from the Canada Pension Plan (CPP) is not a recent one. It has resurfaced on several occasions since the beginning of this century with proponents of Alberta leaving the CPP advocating replacing it with an Alberta Pension Plan (APP). The issue arose most recently last September when the Government of Alberta released a report prepared for it by the actuarial firm LifeWorks. (By the time the report was released, LifeWorks had been acquired by Telus Health (TH), and I will refer to it as the TH report.) According to the report, if Alberta withdraws from the CPP, it is entitled to receive more than half (53 percent) of CPP assets. Not surprisingly, this claim has elicited vigorous reaction from critics.

This E-Brief will raise serious concerns about the TH report’s suggested Alberta asset allocation. But I have no concern about the actuarial methods, assumptions and computations in that report. In these respects, they are consistent with the federal Office of the Chief Actuary.

The author thanks Alexandre Laurin, William B.P. Robson, Benjamin Dachis, Duncan Munn, Charles DeLand, Keith Ambachtsheer, David Dodge, Barry Gros, Malcolm Hamilton, Eric Monteiro, James Pierlot, Trevor Tombe, Ed Waitzer and anonymous reviewers for helpful comments on an earlier draft. The author retains responsibility for any errors and the views expressed.

Introduction

This E-Brief analyzes those criticisms and, more broadly, the TH report itself. In some passages, I draw on work by University of Calgary economics professor Trevor Tombe. But the E-Brief’s focus is the TH report itself. References to Tombe’s work are intended to add context and insight but no attempt is made to provide a thorough analysis of Tombe’s work.

I will explain how Alberta’s claim on 53 percent of CPP assets was established and why it is a problematic claim. I will also offer an explanation of its financial consequences, both for a new APP and the remaining CPP. I will then offer thoughts on what the APP might face in the absence of a large withdrawal of CPP assets - a more likely outcome than the 53 percent. Before concluding, I will identify some additional issues related to the creation and operation of an APP.

But before I get to all of that, I will establish a general framework for the discussion by walking through some basic CPP aspects that are relevant to a potential Alberta withdrawal.

Framework: a few CPP basics

The CPP collects contributions and pays benefits based on earnings from employment and self-employment in all provinces except Quebec, which has always run its own plan – the Quebec Pension Plan (QPP).

From 1966, when the CPP was created, until 1997 the plan was financed largely on a pay-as-you -go (pay-go) basis. Therefore, most contribution revenue was paid out immediately in benefits and administrative expenses. A big fund and investment income had little role to play in financing CPP benefits. In this type of arrangement, the number of people receiving benefits compared to the number paying contributions plays a very important role in determining how much has to be contributed. An aging society increases the number of beneficiaries compared to contributors and pushes up the contribution rate.

In 1997, the plan governors decided to accelerate the rate at which CPP contributions were increased to a level above what was needed to pay current benefits. The idea was to build up a reserve fund that would generate enough investment income so that contributions would not have to increase in response to population aging.

In 2016, federal and provincial finance ministers agreed to increase CPP benefits. Contribution rates associated with the added payouts would be phased in from 2019 to 2025 while the enhanced benefits would be phased-in over 40 years starting in 2019. Amendments to the CPP in the late 1990s had required that any new CPP benefits beyond the 2019 base benefits be fully funded and the additional benefits will be fully funded. Given the relatively small size of the additional benefits and their recent creation, they are a minor consideration in the possible creation of an APP. For that reason, they are largely ignored in the TH report and will be in this E-Brief as well.

The more than $500 billion now managed by the CPPIB largely reflects the contributions and investments to fund the base benefits. It reflects the ramping up of the contribution rate so that returns on the larger fund could stabilize the contribution rates over the longer term. Nonetheless, the base CPP remains in large measure a pay-go plan. According to the 31st CPP Actuarial Report by the Office of the Chief Actuary (OCA 2022), the invested assets of the base CPP amounted to $544 billion at the end of 2021. But the liabilities that have accrued by current participants in the base plan are $1,686 billion resulting in a $1,142 billion shortfall. This shortfall will be covered by direct transfers from contributors to beneficiaries in the years ahead. The transfers in the years ahead are accounted for in the current contribution rate.

In fact, Alberta, or any province, can withdraw from the CPP. That right is clearly established in Section 3 of the CPP Act.

These procedural requirements are reflected in the TH report; it does most of its financial calculations on the assumption that notice would be provided on Jan. 1, 2024, with the APP beginning to function in 2027. Unless otherwise noted, the dollar figures in the TH report included in this E-brief are the projected 2027 dollar figures. (The dollar numbers cited in Tombe are 2025 estimates).

As for the substantive conditions, a province that withdraws from the CPP must have a plan in place that provide “comparable benefits” to the CPP. Second, the province must assume its pension payout liabilities incurred up to the time of its withdrawal from the CPP.

These seemingly straightforward conditions require some elaboration.

Regarding the first substantive condition, two things should be noted. First, the degree of difference between the CPP and a plan established by a province leaving the CPP that would allow the latter to be considered comparable has never been tested in court. Very small differences in benefit design have always existed between the CPP and the QPP. The outer boundary on providing comparable benefits is not clear.

Second, if a plan is comparable at the time it withdraws from the CPP, the question arises whether it must remain comparable after the withdrawal. The TH report says on several occasions that comparability need not be maintained in the future. Still, as noted below, there may be practical – non-legal – reasons for maintaining comparability.

The CPP Act also includes a section dealing with what has to be paid to a province that withdraws from the CPP and assumes responsibility for benefits accrued by its residents up to the time of withdrawal. This section lies at the heart of the dispute over the size of the claim that Alberta is making on CPP assets.

The 53 percent claim

Section 113 (1) through 113(3) of the CPP Act deals with the payment to a province that is leaving the CPP. Section 113(2) provides for a payment amounting to:

A) contributions made based on employment in the province over the years, plus

B) investment returns that are derived from the contributions referred to in A,

Minus

C) benefits that accrued over the years based on employment in the province that is leaving the CPP, plus

D) a share of administrative costs that reflects the share of total contributions to the Plan over the years made in the province that is leaving the CPP.

In discussing the application of this formula to the amount that should be paid to Alberta, the TH report says:

A literal reading of the legislation (Section 113(2) of the CPP Act) as written implies that investment returns should only be applied to CPP contributions, and not to benefit payments and CPP administration costs. Applying this literal reading of the CPP Act would result in an unrealistically large Base asset transfer figure of $637 billion as of December 31, 2021 (117% of Base CPP assets as of that date), which our model projects to grow to approximately $747 billion (118% of Base CPP assets) as of January 1, 2027. An alternate and reasonable interpretation is to apply investment returns to the net cash flows of contributions less benefit payments and CPP administration costs. This alternate interpretation has been used for the purposes of this report. (p. 15.)

TH’s “alternate and reasonable interpretation” leads it to the conclusion that $334 billion should be paid to Alberta.

Two things are striking about this reasoning. The first is the wide range of estimates that emerge from the application of Section 113(2). The amount of the transfer based on the “more reasonable” approach is less than half the result based on the literal approach. Moreover, Tombe suggests an even wider range of possible transfers based on 113(2). On his analysis, $150 billion should be paid to Alberta.

The other thing that is striking about the TH passage just cited is that it imposes a judgment about what is and is not a reasonable transfer amount. I return to the issue of a reasonable solution below.

Part of the reason for the wide range of possible transfers arising from the application of Section 113(2) is ambiguity surrounding items B and, to a lesser degree, C in the formula.

Up until 1997, the income referred to in item B was made up almost entirely of interest payments on non-marketable provincial government bonds that were purchased by the CPP Investment Fund.

The enlargement of the CPP fund and its increased importance in financing base benefits led to its investment in a diversified portfolio of marketable assets. Nonmarketable provincial bonds now play little or no role in financing CPP benefits. The clear link that used to exist between the sources of investment income and specific provinces has been lost.

This history provides some context for looking at very different approaches taken by the TH report and Tombe in making B operational. The TH report creates a hypothetical APP account. It credits to the account CPP contributions made in Alberta. It subtracts from it the benefits payments and administrative costs attributable to Alberta. It then applies CPP investment returns to the balance. It does this for every year of the CPP’s existence. As noted, this leads to a proposed $334 billion transfer – 53 percent of CPP assets as of Jan 1, 2027.

Tombe, by contrast, builds up a suggested transfer by aggregating the components in the formula. For B he takes the total amount of CPP investment returns that have accumulated over the years and allocates to Alberta a portion of the assets that is proportionate to its share of aggregate contributions. As noted, this leads to a proposed $150 billion transfer.

Both the TH report and Tombe note that there is a problem with item C in the formula. The problem stems from the fact that the available data on the province where CPP benefits are paid cannot be properly linked to the province where the contributions that give rise to them were made. A person might spend some part of their working career in Alberta and then move to another province where they receive their benefits. In cases like this, the available data would credit the contributions to Alberta but the benefit based on those contributions would be recorded in the province to which the person moves. Clearly, the opposite could also happen. It is not possible at present to accurately quantify the impact of these movements.

The TH report identifies the problem in C as one requiring further refinement.

Comments on an earlier draft of this E-Erief expressed the hope that an application of Section 113(2) would lead to a clear and incontrovertible answer as to the amount that should be transferred to Alberta should it create an APP. But the ambiguities that arise in applying the formula in 113(2) are enough to make it clear that that is unlikely. The need for a value judgment on what is reasonable accentuates the unlikely nature of an easy determination of what should be transferred.

What is a “reasonable” transfer?

The TH report abandons its initial calculation of the transfer to Alberta in favour of something “more reasonable.” This raises the obvious question of what a reasonable settlement would look like. I would suggest three related standards when thinking about a reasonable settlement.

- It should be reasonable for all provinces, not just the one leaving the plan.

- The assets payable to a single province that leaves the CPP should be neither more nor less than what it would receive if all nine participating provinces were to withdraw from the CPP at the same time. There should be no reward for being first leaver.

- The settlement for all provinces contemplated in point 2 should be limited to CPP’s total assets.

The calculation in the TH report does not meet these standards. Indeed, based on its formula, Ontario, BC and Alberta could claim all CPP assets and leave other provinces with negative balances (Tombe 2023). If Alberta were to leave the CPP with 53 percent of its assets, the incentives for Ontario and BC are clear: leave the plan now. It is worth noting, too, that neither the federal government nor the provinces have direct financial responsibility for contributing to the CPP. As a result, it would seem that the only practical way to make up negative balances would be to increase contributions paid by individual employees remaining in the CPP.

Among APP advocates, the leave rationale is frequently expressed in terms of Albertans paying more into the CPP than they get back in benefits. Looking beyond the problematic lack of data that links CPP contributions by province to benefits paid by province, the available data nevertheless confirm this concern, if seen in isolation.

Before looking at the specifics of Alberta’s situation, it is worth noting that thanks to the buildup of CPP assets to move to steady state funding, all provinces combined have been paying more into the CPP than they have been taking out in benefits.

Currently, the base CPP is close to a pure defined benefit (DB) plan that promises a retirement benefit (plus survivor, disability and children’s benefits) based on age and a person’s earnings history. Any such plan would involve cross-subsidies among plan members within and between cohorts. This is true of workplace DB pension plans as well as the CPP. Because the base CPP is still largely funded on a pay-go basis, Alberta is a source of cross subsidies at this time thanks to its younger, higher paid and more fully employed population. These attributes of the Alberta population give it a higher ratio of contributors to beneficiaries and contributory earnings to benefit payments.

A clear question that arises is why a jurisdiction that is a source of cross-subsidies might want to remain in a group that is pooling risks. The answer lies in the reality that pension plans are a mix of investment and insurance products. A jurisdiction that is a source of cross-subsidies at one moment in time may find itself on the receiving end of cross-subsidies in the future as its relative fortunes decline. It is a bit like paying premiums for home and auto insurance. You pay the premiums and hope you never collect. (More will be said about Alberta’s risks below).

Part of the reason for Albertans paying more in than they get out may reflect the current problematic lack of clear linkage between where contributions are made and where benefits are paid.

It is important to note that the current situation of Albertans paying more in than they receive from the CPP does not arise because individual Albertans with a particular level of earnings, gender and age are treated any differently than people in similar circumstances elsewhere in Canada. As noted above, it stems from the fact that in the aggregate, Albertans are younger, higher paid and more fully employed than Canadians in general.

APP and CPP: after a transfer

The TH report provides a good deal of analysis of the minimum contribution rates for the APP and CPP after the proposed $334 billion asset transfer. The minimum contribution rate (MCR) combines a steady-state rate, which is the lowest rate that will remain stable over the longer term, with any payments required to amortize the cost of a past service benefit improvement. The minimum contribution rate is estimated by the Office of the Chief Actuary and is made public in each triennial actuarial report on the CPP.

In view of what follows, it is important to note several things about the CPP’s MCR. The base CPP has a legislated contribution rate of 9.9 percent shared equally between employers and employees. As long as the MCR stays below the legislated rate no change is needed in the legislated rate. But if the MCR rises above the legislated rate and federal and provincial finance ministers cannot agree on an alternative, a default position in the CPP Act is triggered. The default provides for eliminating the price indexation of benefits currently in pay and for contribution rate increases. The default applies until a future actuarial report indicates that the MCR has dropped below the legislated rate.

At present, the CPP MCR includes a small amortization payment resulting from a benefit improvement made some years ago. It amounts to 0.02 percentage points and will be fully amortized in 2034. Currently, the MCR is 9.56 percent but will drop to 9.54 percent when the amortization payments end. The latter number is used in the TH report.

In the TH report, the MCR for an APP is estimated at 5.91 percent, which is well below the 9.9 percent legislated rate and the 9.54 percent MCR for the base CPP. The case for an APP is often made based on its demographic and labour market characteristics. But the following passage from the TH report is instructive:

The Base minimum contribution rate for an APP is significantly lower than the CPP Base minimum contribution rate due in large part to the size of the estimated initial asset transfer …. In addition, the current ratio of Alberta contributors to Alberta beneficiaries is higher than that of the ratio of CPP contributors to CPP beneficiaries due to a younger population and historically higher employment. As such, under an APP, we expect that the returns on the initial assets will fund a significant portion of future benefits and, even under a reduced minimum contribution rate, an APP will experience positive net inflows (i.e., contributions will exceed benefit payments and expenditures) over the short and medium terms, allowing for a quicker accumulation of assets under an APP. However, we observe that, although the pay-as-you-go rate for a Base APP is initially lower than that of the CPP, we expect this rate to catch up with the CPP pay-as-you-go rate based on the assumptions used in this analysis, as the age-dependency ratio in the Alberta population would eventually catch up with the rest of Canada. (p. 13.)

Therefore, the demographic and labour market advantages are real, but a major reason for the big reduction in the MCR for an APP is the size of the asset transfer from the CPP. With the transfer of $334 billion, TH estimates the ratio of APP assets to expenditures would be 28.9. This compares with a current ratio for the CPP of 8.4 and 5.6 after the transfer. The TH report suggests that such a large ratio of assets to expenditures creates the possibility of a more fundamental revision of the APP financing that would move it more fully in a pre-funded direction. In such a context, investment returns play a greater role and demographic variables a smaller role in APP finances than would be the case with a smaller transfer.

The TH report estimates that with its recommended asset transfer, the MCR of the remaining CPP will increase from 9.54 percent to 10.36 percent. The 10.36 rate is higher than the legislated rate. As noted above, unless federal and provincial finance ministers agree to an alternative solution, contribution rates will increase, and the price indexing of pensions in pay will be suspended.

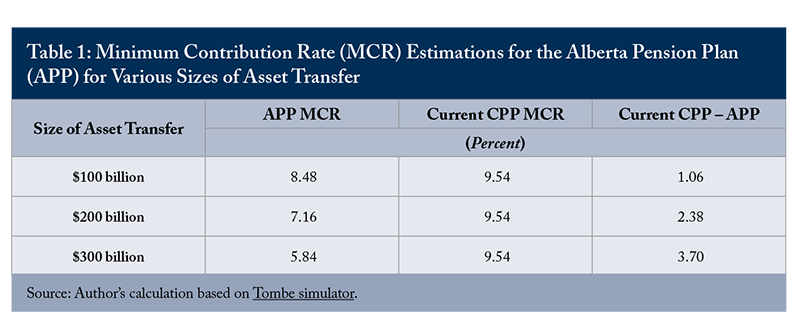

Looking beyond the TH report, the impact of the size of the asset transfer on the APP MCR can also be illustrated using a simulator developed by Tombe. In the table below, based on Tombe’s work, the MCR for the APP is shown with varying levels of asset transfer. The difference between the MCR for the APP and current CPP is shown in the right-hand column. Clearly, the APP’s ability to deliver comparable benefits to the CPP at a lower contribution rate is strongly influenced by the size of the asset transfer.

Demography – proceed with caution

Because the CPP base benefits are still financed largely on a pay-go basis, the CPP contribution rate is influenced significantly by demographic variables. This reality is most clearly reflected in TH’s estimates of the CPP pay-go contribution rate, which ignore the investment income generated by the fund. Over the 30-year period to 2052, the TH report estimates that the CPP rate definitely would be higher than the APP rate. But from 2052 to 2092, the report predicts the two rates as quite close and virtually identical at the end.

As per the TH scenario, the APP would start its life with a pay-go cost advantage. But it would also take on benefit promises that have to be met over a time frame of 60 years and more. The histories of both the CPP and the QPP highlight the fact that betting on long-term demographic futures can be risky business.

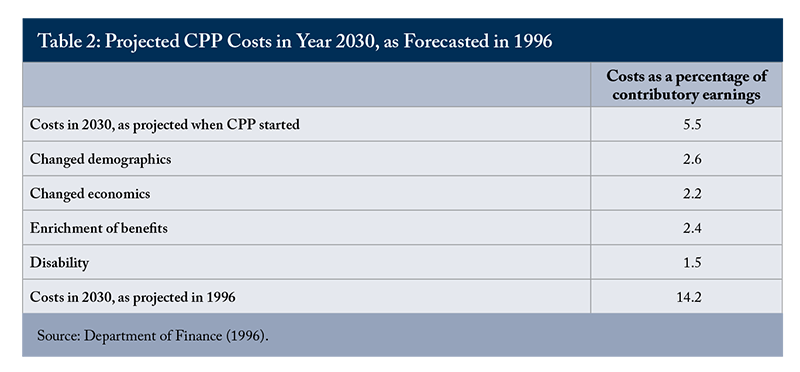

Indeed, in the mid 1990s, the CPP was approaching its 30th anniversary. A debate leading to the change in financing methods was underway. In the midst of it, the federal and provincial governments published a consultation paper, An Information Paper for Consultations on the Canada Pension Plan (Department of Finance 1996). The paper included the following table that was designed to show the factors that caused the estimated pay-go cost in 2030 as estimated in the mid 1990s to be so much higher than when the plan was launched.

Several factors led to the near tripling of the estimated pay-go rate, with unanticipated demographic change leading the way.

At the time that the CPP and QPP were being planned, the governments of Canada and Quebec were quite naturally preparing cost estimates of their proposed plans that included demographic estimates. A key demographic variable was the ratio of people over 65 to those aged 20 to 64. At the time, 1964, the Quebec ratio was lower than Canada’s ratio, and Quebec’s analysis had it staying that way over the next 30 years. For its part, Canada foresaw the ratios equalizing at that point.

As events worked out, any demographic advantage that Quebec might have had in the mid 1960s disappeared with the passage of time. Quebec has had to raise its QPP base contribution rate to 10.8 percent in order to maintain the very similar benefits to the CPP.

The Quebec experience is a cautionary tale for Alberta. There are no guarantees that a demographic-based advantage at a particular moment will last. In Alberta’s case, much of its demographic advantage comes from international and interprovincial migration – its fertility and mortality rates are roughly similar to those for the entire country.

Interprovincial migration to Alberta can be very volatile. Net migration into the province dropped from more than 35,000 in the period 2012 to 2014 to a net outflow of more than 15,000 in the period 2015 to 2017. A sustained drop can eliminate Alberta’s demographic advantage.

In the near future, it is likely that an APP that provides benefits equivalent to the CPP will have a lower pay-go contribution rate than the CPP. But it is also true that an APP will have a narrower economic base than the CPP and will be more vulnerable to both short and long-term setbacks. The potential advantage in the short-term needs to be set against the risks associated with a less diverse economic base and a smaller population base. The creation of an APP would involve a marked reduction in risk diversification. (Risk diversification would be further reduced if the fund backing an APP was heavily invested in Alberta, as some APP advocates have proposed).

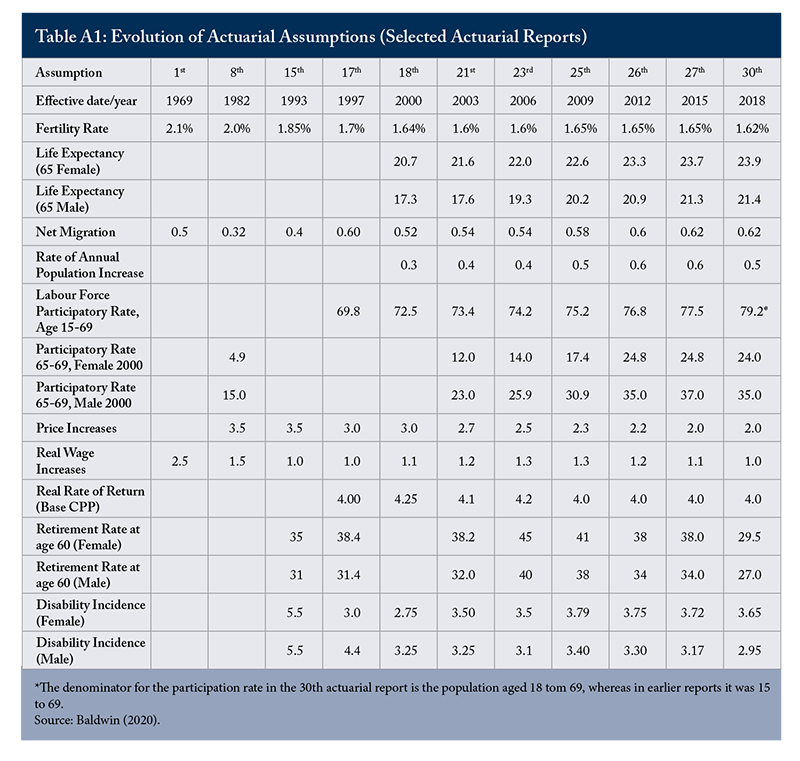

A somewhat wider review of the risks in financing a plan like the base CPP is provided in Sources of Comfort and Chills: What We Can Learn from CPP Valuation Reports (Baldwin 2020). It highlights the uncertainties involved in operating such a plan and includes a table that traces key actuarial assumptions from the late 1970s and early 1980s to 2018. The assumptions included demography (fertility rates, life expectancy) and the future of the labour market, investment returns, incidence of CPP claims, etc. In almost all these areas, Baldwin points out that the future as perceived when reports were written was quite different from reality. The demographic assumptions have evolved in a higher-cost direction. The discrepancies do not arise from any weaknesses in actuarial practice in the past, but from the reality that social and economic activity evolves in ways that are not predictable.

CPP some additional considerations

In considering the creation of an APP, there are three aspects about the CPP that merit further thought.

One CPP beneficial feature is that it facilitates labour mobility. This is an important issue in Alberta for reasons noted above. As can be seen in the relationship between the CPP and QPP, it is possible to work out portability arrangements that support mobility. But these arrangements will be easier to work out the more similar plans are. This is an important consideration in thinking about the design of an APP. (The ability to work out portability arrangements will also depend on the temperature in Alberta’s relationship with the federal government and other provinces).

Another positive CPP feature is that it provides retirement income that is relatively predictable and will last a lifetime. One hopes an APP would do the same. But for employees who have average to higher earnings, the CPP when coupled with Old Age Security (OAS) benefits will not be enough to allow retirees to maintain their standard of living in retirement. OAS and CPP benefits will need to be supplemented by income from other sources.

Traditionally, workplace pension plans have helped people bridge the gap between what is available from OAS and CPP and what is needed. Since the 1990s, there has been a notable transition among private-sector workplace pension plans from defined-benefit pension schemes to capital accumulation plans (Laurin and Turpie 2023). These arrangements typically come with unpredictable benefits and frequently incur higher administrative costs. This transition has predominantly affected private-sector employees.

This shift in workplace pension plans suggests two things. First, if an APP is to be created, it should provide relatively certain benefits like the CPP. Second, if the Government of Alberta wants to help all Albertans have an adequate retirement income, it may be more helpful to think about creating a supplement to the CPP rather than replacing it with an APP.

The CPP’s sheer size is also one of its strengths. Size is typically associated with lower administrative costs, a wider range of investment opportunities and lower investment management costs per dollar invested in an asset class.

Other issues that need resolution

The TH report provides specific information on several financial issues related to creating an APP. But it also raises important unresolved issues. Some of these need resolution by the Government of Alberta – preferably before Albertans are asked to vote on whether to leave the CPP for an APP.

As noted, in order to leave the CPP, the Government of Alberta will need a plan with comparable benefits in place. But the TH report notes that Alberta is not bound to have a comparable plan once the APP has been created. It is crucial for the Government of Alberta to clarify its long-term plans regarding the APP’s design. Will it maintain a plan that is similar to the CPP, or will it change course as some politically prominent Albertans have suggested? Voters should know what they are getting into not just at the moment of separation, but over the longer term. The answer may have an impact on the APP’s portability and labour flows into Alberta.

In a similar vein, the TH report focuses its financial analysis on the MCR. It notes that a legislated rate similar to that in the CPP might be created but does not opine on whether a legislated rate should be established. Again, this ought to be clarified along with related financing rules before a promised referendum is held on creating an APP. If the MCR rises above the legislated rate, do defaults similar to those in the CPP come into play and, if so, what are the default provisions?

It is also vitally important to know how an APP will be governed. Will it be governed as an internal government function, or will it have an arm’s length structure? Will non-government stakeholders have a role in APP governance? Will the investment function fall directly under the general plan governance structure, or will it be a separate entity with its own structure? Will the investment function be delegated to the Alberta Investment Management Corporation and if so, does its mandate and governance structure need revision?

These governance and management issues are very important. If an APP is governed as an internal government function, there is a risk of instability in the plan as governments change party hands, and the constellation of stakeholders with influence changes. The same holds true for the investment function. Again, these issues should be addressed before people are asked to vote on whether to leave the CPP for an APP.

Unfortunately, Bill 2, The Alberta Pension Protection Act tabled in the fall of 2023, does not address these issues. It establishes that any transfer from the CPP will be used solely to provide benefits under an APP, and that benefits under an APP will be equal to or greater than CPP benefits and that contributions may be lower. However, the Bill’s main focus is to establish that a referendum may be called on Alberta leaving the CPP, and that its results will be declared binding or not prior to the referendum.

Conclusions and recommendations

The question whether Alberta should leave the CPP in favour of an APP has consequences that may extend beyond Alberta and, as a result, non-Albertans will opine on it. From my vantage point, it looks like the creation of an APP will involve taking on a good deal of risk for relatively small gains that are uncertain over the long term. In addition to the financial risks associated with the APP itself, there is some potential risk to interprovincial labour mobility, which is important to Alberta’s ability to meet its labour supply needs. Nonetheless, it is a choice that Albertans have to make. One would hope that if Albertans are asked to vote on leaving, they will have the answers beforehand to the questions posed above.

The question of how much should be paid to Alberta if it leaves the CPP has more direct and potentially quite difficult implications for what is left of the CPP. Therefore, it has attracted a good deal of attention in public discourse outside of Alberta and in this E-Brief.

With respect to the amount of the payment to Alberta, two things should be clear from the foregoing. First, Section 113(2) of the CPP Act lacks clarity on key provisions. It can yield a range of possible conclusions on the amount that should be paid to Alberta. It is inevitable that the final conclusion will be reached through a negotiating process. Second, the need of the TH report to move from its conclusion based on a literal reading of the Act to a “more reasonable” conclusion suggests that discretion anchored in some notion of what is reasonable will be required to resolve the issue. Deciding on the amount to be paid to Alberta is not just an actuarial math problem.

In November 2023, federal and provincial finance ministers met and addressed the APP issue. They agreed that the Office of the Chief Actuary should opine on the amount to be paid to Alberta. I have the utmost respect for the work of the OCA. But it is the responsibility of government leaders to clarify what is reasonable. I have offered a view on this. I make no pretence that this is the last word on the matter, but something of this sort is necessary to guide the math.

It should be clear, too, that while there may be an understandable desire to have a solution that can be rationalized by Section 113(2), it is impossible to arrive at a solution that satisfies all definitions of the size of transfer that follows. Reaching a conclusion with this problematic section in place creates a situation where it will be hard to explain to the current populations of Alberta and Canada how the amount was arrived at. Furthermore, it will not provide a clear precedent should another provincial withdrawal from the CPP occur in the future.

As federal and provincial finance ministers move toward a commonly accepted view of what is a reasonable transfer to Alberta, they should amend or replace Section 113(2) so that it clearly spells out how the amount of the transfer is established. While such action would have the unfortunate appearance of changing the rules in the middle of the game, the current problem is that the game lacks clear rules. Accountability to today’s public and facilitating precedent for the future would be enhanced by a clear Section 113(2) that yields a reasonable result.

That is not the case for Alberta’s current proposal. To review the main findings of this E-Brief:

1) The numbers don’t add up. If other provinces withdrew comparable amounts to Alberta’s proposed withdrawal of $334 billion, or 53 percent of the CPP’s assets, there won’t be enough money to go around. If Alberta takes this path, large provinces like Ontario and BC would be incentivised to withdraw their money right away.

2) Albera’s tally of contributions made minus benefits paid for its citizens ignores labour mobility. People can work in Alberta and make contributions there, but later move to another province and collect benefits there. There is also the issue of creating portability between provinces.

3) Alberta’s demographics, with its younger, higher-earning workforce, are now favourable to keeping contribution rates relatively low. But over decades, demographics can change significantly, undercutting the province’s assumptions about future contributions.

4) Finally, there are major unanswered questions about the governance of the APP. If an APP is managed as an internal government function, there is a risk of instability in the plan as governments change party hands and the constellation of stakeholders with influence changes. The same holds true for the investment function.

The conclusion: it appears the creation of an APP will involve taking on a good deal of risk for relatively small gains that are uncertain over the long term.

Appendix:

References

Baldwin, Bob. 2020. Sources of Comfort and Chills: What We Can Learn from CPP Valuation Reports. Commentary 587. Toronto: CD Howe Institute.

Department of Finance. 1996. An Information Paper for Consultations on the Canada Pension Plan. Ottawa.

Kay, John, and Mervyn King. 2020. Radical Uncertainty: Decision-Making Beyond the Numbers. New York and London: WW Norton and Company.

Laurin, Alex, and George Turpie. 2023. “Strengthening Retirement Income Security: Fairer Tax Rules and More Options Needed.” E-Brief. Toronto: CD Howe Institute.

LifeWorks. 2023. Alberta Pension Plan – Analysis of Costs, Benefits, Risks and Considerations. Government of Alberta.

OECD. 2015. Pensions at a Glance 2015. OECD and G-20 Indicators. Paris.

Office of the Chief Actuary (OCA). 2022. 31st Actuarial Report on the Canada Pension Plan. Ottawa.

Robson, William B.P. 1996. Putting Some Gold in the Golden Years: Fixing the Canada Pension Plan. Commentary 76. Toronto: C.D. Howe Institute.

Tombe, Trevor. 2023. “The Alberta Pension Advantage: A Quantitative Analysis of a Separate Provincial Plan.” A working paper accessed on the Social Science Research Network website at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4576950.

This E-Brief is a publication of the C.D. Howe Institute.

Bob Baldwin is Chair of the Pension Policy Council of the C.D. Howe Institute. He has many years of experience as a researcher and writer on pension issues, as well as in various aspects of pension plan management.

This E-Brief is available at www.cdhowe.org.

Permission is granted to reprint this text if the content is not altered and proper attribution is provided.

The views expressed here are those of author. The C.D. Howe Institute does not take corporate positions on policy matters.