From: Brian Lewis

To: Ontario housing observers

Date: May 3, 2023

Re: Make Mine a Double: Ontario’s Housing Supply Targets

The Ontario government has embraced a goal of 1.5 million new homes being added by 2031.

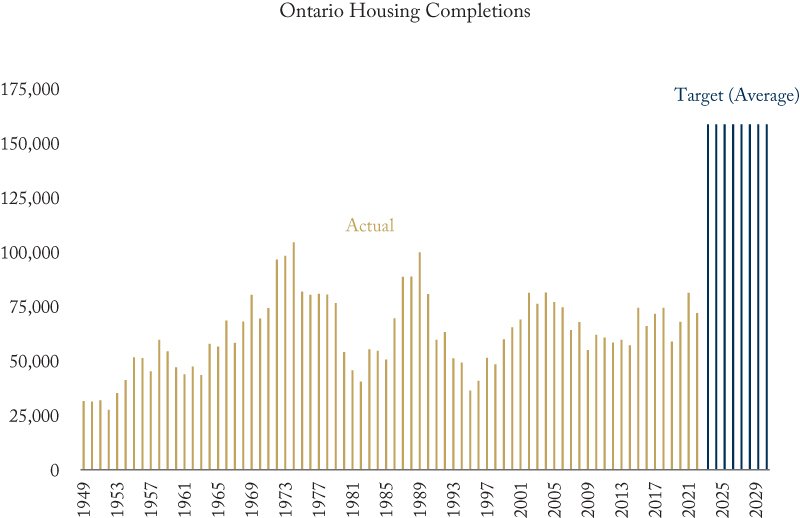

This is incredibly ambitious, requiring housing completions of roughly double their current levels over the next 10 years. Such a significant and sustained increase in output would be unprecedented.

In 2022, the first year for the target, both housing starts (96,000) and completions (72,000) were well below the 150,000 needed. As such, it has become an ever bigger stretch goal after one year, with 158,700 completions per year now required over the next nine years to reach 1.5 million by the end of 2031.

While the target is ambitious, 1.5 million new homes is a reasonable estimate of what’s needed, given the current excess demand for housing and projected population growth. If the province fails to substantially increase housing supply, it will face continued affordability challenges that significantly stress younger people and incentivize them to live elsewhere. As such, the housing supply is a significant risk to the province’s economic prosperity, given human capital's primary importance in driving future growth.

The Ontario government has taken meaningful steps to encourage increased housing construction, informed by the work of the Ontario Housing Affordability Task Force. Reducing regulatory and municipal barriers to housing development is needed to reach these housing supply goals. However, there are hazards related to the effectiveness of the steps taken. For example, municipalities may need more willingness and resources to implement the changes required for these regulatory changes to have the expected or needed impact. Furthermore, community resistance could hamper the effectiveness of these measures. And more important, further steps are needed because significant other obstacles exist: Limited economic capacity and diminishing investment appeal.

It will be very challenging to increase the economic capacity to support more than doubling annual housing completions. Notably, capacity utilization rates in the Canada-wide construction sector are at their highest levels since the late 80s housing boom, indicating little available slack. A primary capacity restraint is finding construction workers, indicated by job vacancies that are two and half times higher, at 6.5 percent, over the pre-pandemic level. Employment in Ontario’s residential building construction sector reached 60,000 workers in 2022, an increase of roughly 10 percent from the previous year. Presumably, the province will need to add another 60,000 workers quickly to achieve its housing supply target.

The government recognizes this and has taken steps to increase the number of skilled tradespeople. Even if those efforts are successful, doubling the pace of housing construction will also require many more highly skilled and educated non-trades people to do planning, architecture, engineering, and project management.

And there are many other constraints. Doubling output will require doubling the amount of raw materials, intermediate manufactured goods and construction equipment. As the 2021 PVC piping shortage demonstrated, new buildings rely on all inputs being available, and the absence of any single component can significantly slow progress.

In addition to these challenges, higher interest rates are a game-changer as they increase the cost of project financing. Elevated interest rates also increase investor returns on relatively safer assets such as bonds and GICs compared to somewhat riskier housing investments. This represents a massive shift for housing. Low rates from 2008 to 2019 fueled housing price appreciation and investor appetite while low-risk alternatives provided meagre returns.

Concerns regarding investment appetite go beyond the implications of higher interest rates. An unintended consequence of policies brought into place to dampen speculative investment and protect tenant rights also serve to make it less attractive for legitimate investment in real estate. Stories are increasingly widespread of small landlords under significant financial stress due to weak regulatory enforcement of renter obligations. Individual investors often face incredibly high marginal tax rates on rental income earnings and limited opportunities to shelter these earnings in ways possible for other investment vehicles.

So what more can policymakers do to get close to their housing target? Here are three pieces of advice.

- Develop some clear and realistic near-term benchmarks to address the skepticism about Ontario’s long-term supply target. These would include expectations for permits, housing starts, housing units in progress and completions over the next three years. Then, track against these benchmarks and report on progress regularly. This would add realism to the government’s 10-year plan and provide more immediate accountability.

- Make better use of existing building capacity. For example, take steps to encourage further conversions of commercial and industrial buildings to residential use. As well, consider options to encourage the supply of resale homes by seniors by offering attractive long-term care options as opposed to the current generally detested “beds.”

- Provide tax incentives for earned rental income to address the increasingly less attractive investment climate for housing. These could be comparable to the treatment of capital gains, helping to offset heightened risks and growing investment disincentives. Also, as steps are taken to protect tenants from bad landlord behaviour, show equal interest in supporting landlords in cases where tenants misbehave.

Brian Lewis is a senior fellow at the C.D. Howe Institute and the Munk School of Global Affairs and Public Policy and former Chief Economist for Ontario.

To send a comment or leave feedback, click here.

The views expressed here are those of the author. The C.D. Howe Institute does not take corporate positions on policy matters.