Fiscal COVID: The Pandemic’s Impact on Government Finances and Accountability in Canada

- Beyond its damage to Canadians’ health and their economy, COVID-19 strained public finances, and both highlighted and exacerbated gaps in governments’ accountability to legislators and voters.

- Spending by all senior governments jumped in the 2020/21 fiscal year – up 7 percent on average across provinces and territories, and up more than 70 percent for the federal government. Although federal direct transfers and indirect support through other programs buoyed provincial and territorial revenues, higher expenses boosted accumulated deficits across the board, with the federal government in particular borrowing enough to impair its capacity to deliver services in the future.

- Stewardship of public funds during the pandemic was lax. Some governments delayed their 2020/21 budgets until late in the fiscal year, and the federal government presented no budget at all. The completeness and quality of information about COVID’s impact in governments’ public accounts varied widely. Comparisons of that limited information show major differences among governments’ spending on healthcare and other programs, including health spending unrelated to the pandemic, that are hard to explain with reference to COVID’s health or economic impacts.

- Although many provinces and territories finished 2020/21 with surprisingly strong revenues and bottom lines, the debt-financed federal spending that supported them is winding down. Restoring fiscal health will require discipline, and COVID revealed that fiscal accountability in times of crisis is inadequate. Legislators should insist on timelier, fuller, and more reliable fiscal information in the future.

The authors thank Alexandre Laurin, Nick Pantaleo, Tom Wilson and anonymous reviewers for comments on an earlier draft. The authors retain responsibility for any errors and the views expressed.

Introduction and Overview

The COVID-19 pandemic had huge impacts on human health and the world economy. Its impacts on public finances were also huge. Moreover, an investigation of its impact on public finances highlights problems with the timeliness, fullness and reliability of the information Canada’s senior governments give their legislatures and the public – in general, and in times of crisis particularly.

A few numbers from the public accounts of Canada’s senior governments show the scale of COVID’s fiscal impact. The 2020/21 fiscal year began on April 1st, 2020, barely more than two weeks after the declaration of a pandemic. The expenses of Canada’s senior governments – the federal government, provincial governments and territorial governments together – amounted to $1,140 billion that year, $309 billion higher than in 2019/20. The unweighted average increase in spending by provinces and territories between 2019/20 and 2020/21 was 7 percent.

Revenues held up quite well – while the aggregate revenues of senior governments were lower in 2020/21 than the year before, most governments experienced increases. The net effect of much higher expenses and little change in revenues was a $368 billion increase in their accumulated deficits – the measure of debt (including capital assets) that is the standard measure of fiscal capacity in Canadian public sector accounting standards. The unweighted average increase in provincial and territorial accumulated deficits was equal to 5 percent of their 2019/20 expenses. The federal government’s accumulated deficit ballooned by $327 billion in 2020/21, an amount equal to 90 percent of its 2019/20 expenses. Adding that to the all-government average raises the average deterioration to more than 11 percent of expenses.

Such a major crisis should prompt governments to provide legislators and citizens with extensive information about its fiscal impact: how it affected previous plans, and how it affected their results afterward. While a number of governments provided information as their responses developed and reported on COVID’s impact on particular revenues and expenses, comparisons to pre-COVID plans and information in public accounts published after fiscal year-end fell well short of that expectation. Some problems with the information governments provide in their budgets and fiscal projections, as well as in their public accounts and financial statements, are longstanding (see for example, Robson and Wu 2021a). Others were worse in 2020/21.

Senior governments should present budgets well before the April 1st start of their fiscal years. In 2020/21, that would have given a clean pre-pandemic baseline, since the declaration of the pandemic and the beginning of lockdowns occurred in mid-March. Historically, many have not presented timely budgets, but 2020/21 was unusually bad. When the pandemic hit, the federal government proposed legislation that would have let it tax, spend and borrow without parliamentary oversight until the end of 2021. Although that overreach proved too much to sustain, it sidestepped Parliament by presenting no budget for 2020/21. Several provinces delayed their budgets for months. For this investigation, we use earlier fiscal updates and budgets to get an idea of what some governments planned before COVID hit. That kind of workaround should not be necessary: governments should give legislators information that is clear, complete, and timely enough for them to cast informed votes on fiscal plans.

After year-end, the financial statements in governments’ public accounts should provide information to help legislators and voters understand what happened, and how it differed from plans. Such analyses are all the more desirable when a crisis has pushed results as far off track as COVID did, yet most governments provided little systematic information on how the pandemic affected overall revenue, expense and surpluses or deficits, or even how it affected key programs. Because health-related expenses are a natural focus of our investigation, we reference compilations from Statistics Canada and the Canadian Institute for Health Information (CIHI) for potential insights into why COVID affected various governments differently. Our scan of spending against health and economic developments across the country raises as many questions as it answers, such as why many governments, including the federal government, showed large increases in non-COVID-related health spending.

Legislative oversight of government spending is fundamental to parliamentary government. While a crisis such as the COVID pandemic should and will force governments to adjust spending and adapt their fiscal frameworks, it accentuates, rather than reduces, the need for elected representatives to understand and approve those changes. Elected representatives need clear baselines: budgets that are not timely, complete or clear impede their understanding of governments’ plans and ability to hold them to account. They need clear reporting: missing or obscure information in public accounts undermines their ability to understand what happened, and correct problems revealed by variances from plan. The COVID crisis not only undermined the capacity of Canada’s senior governments to deliver services in the future, it also demonstrated the fragility of fiscal accountability under stress.

Legislators and Canadians generally should demand budgets and public accounts that are timelier, fuller and more reliable. Those demands should be louder, and legislators should be more insistent, when a crisis throws fiscal plans badly off course. Better information alone cannot guarantee better fiscal management in the future. But it is an essential foundation that needs reinforcing.

The Big Picture

Future historians of public finances in Canada will see from a glance at the aggregate numbers in senior governments’ public accounts that something remarkable happened in the 2020/21 fiscal year – the year that ran from April 1, 2020, to March 31, 2021. Their spending, most notably federal spending, jumped as never before in peacetime. The bottom lines of many – with the federal government again being the most notable – deteriorated on a scale not seen in decades.

Revenues, Expenses and Surpluses or Deficits in 2020/21 Relative to 2019/20

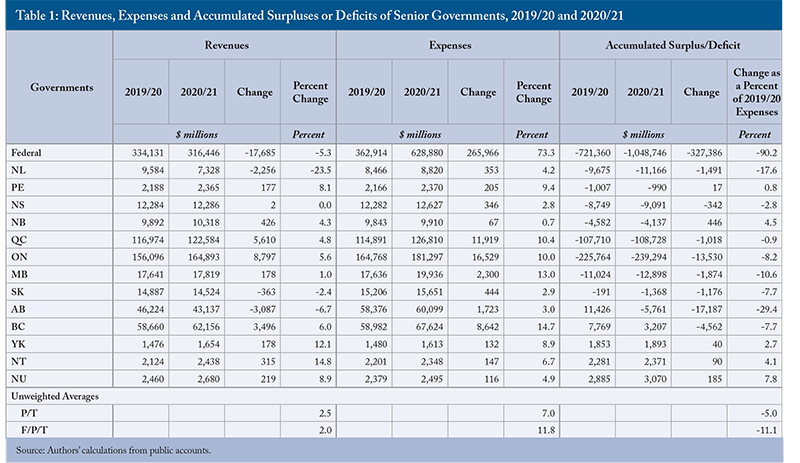

The key aggregate numbers – the revenues, expenses and accumulated surpluses or deficits of the federal, provincial and territorial governments in 2019/20 and in 2020/21 – appear in Table 1.

Revenues: The unusual experience of 2020/21 is least evident in revenues. Some provinces reported declines: Saskatchewan (2 percent), Alberta (7 percent), and Newfoundland and Labrador (24 percent).

Notably, however, notwithstanding the pandemic’s negative impact on output and spending, and depressed prices for many natural resources, the majority of governments reported higher revenues in 2020/21. The average change across all provincial and territorial governments was an increase of 2.5 percent – thanks in large part to, federal transfers and COVID-related support programs that supported spending and tax bases. Adding the federal government’s decline lowers the average, but it is still positive: a 2.0 percent increase.

Expenses: 2020/21’s unusual nature jumps out in terms of expenses. All senior governments spent more, and some spent way more. The average increase across all provinces and territories was 7 percent. The federal government was in a category of its own. Its expenses were more than 70 percent higher in 2020/21 than in 2019/20 – a percentage increase so large that showing the GST Credit as an expense, as would be proper, would barely affect it. The federal government boosted transfers to provinces and territories as part of its response to COVID, so summing across all governments involves some double counting. But since each government runs its own programs, it is noteworthy that including the federal increase raises the all-government average increase to almost 12 percent.

Bruised Bottom Lines: 2020/21 also jumps out from changes in senior governments’ accumulated surpluses or deficits.

Off Course: 2020/21 Results Relative to Plans

Changes in revenues, expenses, and net worth are a vital start in assessing fiscal performance during the pandemic year. These are the reported, audited results, providing key information about governments’ use of resources and their future capacity to deliver services.

For a legislator or citizen trying to assess how COVID affected a government’s fiscal position, however, they are only a start. What if COVID had not happened? Governments anticipated various changes in revenue and spending before the pandemic. How did 2020/21’s results compare to pre-pandemic plans?

Governments that presented budgets well before the April 1st start of their fiscal years, as they should, provide pre-pandemic baselines. COVID’s potential health and economic threats were not evident until well into March of 2020.

The federal government produced no budget for 2020/21. This unprecedented failure – both by the government for not presenting a budget, and by federal parliamentarians for letting it happen – meant Canadians got no formal federal fiscal plan for 2020/21. A legislator or other interested person looking for a pre-COVID baseline would need a workaround. The federal Economic and Fiscal Update released in the middle of December 2019 provided aggregate revenue, expense and deficit projections for 2020/21. We use those for our comparisons of results to projections.

Ontario did not produce its 2020/21 budget until May of 2020. That is also a signal lapse: governments should present budgets before money is committed and spent. Since the pandemic had altered the outlook by May, a person looking for a pre-COVID baseline would need a workaround. For Ontario also, the previous fiscal update – its Fall Economic Statement released at the end of October 2019 – is a reasonable source for pre-COVID projections.

Saskatchewan did not produce its 2020/21 budget until June of 2020 – inconsistent with proper accountability, and unsuitable for a pre-COVID baseline. Its fiscal update for 2019/20 included no projections for 2020/21. In Saskatchewan’s case, we resort to 2020/21 projections released in a companion document to its 2019/20 budget for our pre-COVID baseline. However, the budget-consistent numbers in the companion document are aggregates only, with no details of revenue and expense.

Newfoundland and Labrador produced its 2020/21 budget very late: the end of September 2020. Prince Edward Island did not produce its 2020/21 budget until the second half of June. Neither’s 2019/20 fiscal update contained projections for 2020/21. Nor did their 2019/20 budgets. These lapses mean that no one – legislators, us, nor anyone else – can make these comparisons for Newfoundland and Labrador or PEI.

The Northwest Territories poses a different problem. Although its 2020/21 budget appeared on time, that budget used different accounting than its financial statements (Robson and Wu 2021a). That discrepancy undermines comparisons between dollar amounts in projections and results and will limit our investigation of some COVID impacts.

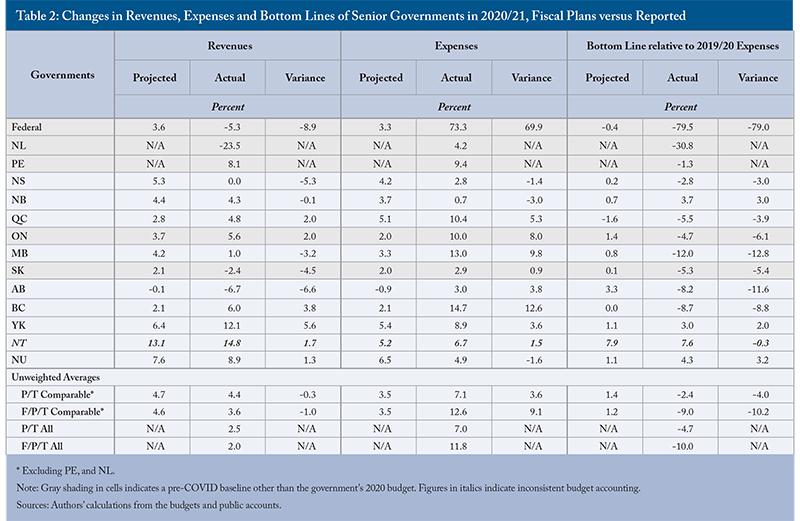

Those caveats noted, we present the comparisons we can make in Table 2. We show percent changes rather than levels. Percent changes mitigate the distortions from the Northwest Territories’ inconsistent accounting, and reduce complications that arise from revisions to governments’ 2019/20 numbers between the time they made their budget projections for 2020/21 and the time they published their public accounts for that year.

The table shows the numbers for governments that presented timely budgets that allow proper comparisons to results in cells shaded blue. It shows the numbers for the Northwest Territories in italics to flag the accounting discrepancy. The cells containing numbers for governments for which we used earlier documents as workarounds are shaded gray. Since PEI and Newfoundland and Labrador provided no numbers suitable for comparisons, their projections display NA, and we omit their numbers from the averages labelled “comparable.”

An Overview of Projections vs. Results: Starting with revenues, most governments budgeted (in pre-COVID budgets) or projected (in fiscal updates or previous budgets) higher revenues in 2020/21 than in 2019/20. The average projected increase across the provincial/territorial governments – except PEI and Newfoundland and Labrador, for which we have no projections – was 4.7 percent. The average reported increase, again excluding PEI and Newfoundland and Labrador, was 4.4 percent. The federal government’s shortfall was considerable: it projected a 3.6 percent increase and reported a 5.3 percent decline – somewhat exaggerated by its inappropriate netting of the GST credit against revenue. Yet half of the 12 provinces and territories for which we can make the comparison reported more growth in revenue than projected, making COVID seem, from an aggregate revenue point of view, strangely benign.

Turning to expenses versus projections, most governments’ pre-COVID plans prefigured higher spending in 2020/21 than in 2019/20. The average projected increase across all of them – except PEI and Newfoundland and Labrador – was 3.5 percent. Against those projections, the average 7.1 percent increase in expenses reported by the provincial and territorial governments represents a material overshoot – 3.6 percentage points. The federal government projected an increase of 3.3 percent and recorded an increase of 73.3 percent. Add that, and the all-government average increase goes to 12.6 percent, a 9.1 percentage-point overshoot.

Comparing projected and reported changes in bottom lines, we see that 10 of the 12 governments that produced useable numbers projected positive swings in their bottom lines – a larger surplus, a smaller deficit, or a swing to surplus from deficit – between 2019/20 and 2020/21.

Historically, Canada’s senior governments have tended to materially overshoot their revenue and expense projections (Robson and Wu, 2021b). During the 20 fiscal years before 2020/21, the average difference between projected and actual revenues across all the governments was 2.3 percent annually, and the average difference between projected and actual expenses was 2.0 percent annually. That record provides some context for the 2020/21 results. If some governments were privately expecting a positive revenue “surprise”, the results were worse than the variances alone suggest. With respect to expenses, some provincial and territorial governments might have projected less than they actually expected to spend, which would make some of the 2020/21 overshoots slightly less extraordinary. On the whole, though, COVID-19 was a shock of a different order than anything over the previous 20 years – notably for the federal government, which responded to COVID with in-year spending increases far beyond anything that had occurred in decades.

What Just Happened? Governments’ Public Accounts Skimpy on the Fiscal Impact of COVID

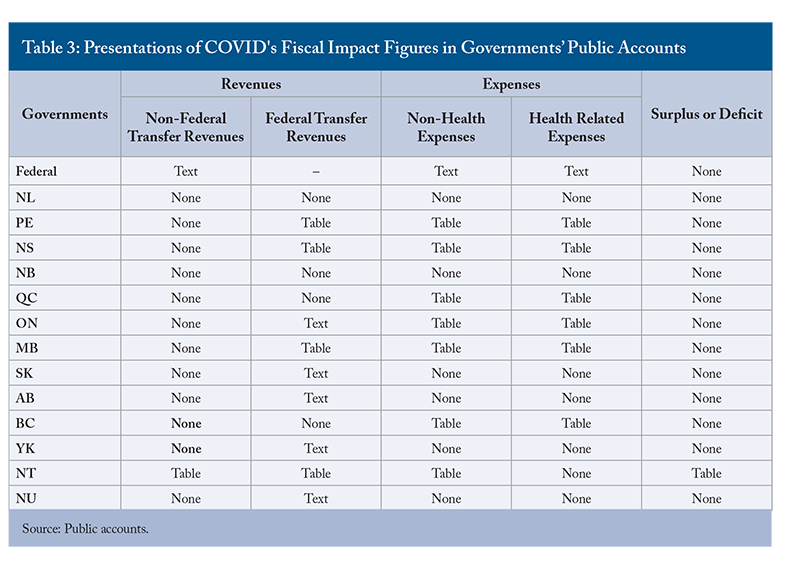

COVID had such huge impacts on government finances that a legislator or other reader of federal, provincial and territorial public accounts for 2020/21 might expect its effects on revenues, on expenses, especially on health, and on the bottom line to be central exhibits. A key reason for providing such information is that it helps people understand how much the shock contributed to variances to plans, as well as the nature of the government’s responses. Disappointingly, however, the public accounts for that year typically did not provide systematic and comprehensive information (Table 3).

While all governments cited COVID in discussing variances in their public accounts, few had dedicated sections explaining COVID’s full impact on revenues and expenses. Most presented partial information in one section one way, and other partial information in a different section another way. Looking across governments, presentations on COVID’s impact were markedly inconsistent. In nearly every case, a diligent reader of a government’s public accounts main volume would have emerged frustrated.

Leaders by Example: Only one of Canada’s senior governments showed systematic numbers on COVID’s impact on revenue. Only six provided systematic numbers for its impact on health and other expenses.

The Northwest Territories stood out for providing a single table with estimates of COVID’s impact on all revenues and expenses in the notes to its financial statements. Unfortunately, the table omitted a key item of interest: COVID’s impact on health spending particularly. Prince Edward Island, Nova Scotia, and Manitoba presented tables summarizing COVID’s impact on federal transfer payments, and on health and non-health expenses, but not on aggregate revenues. Ontario provided information on federal transfer payments in text commentary, and tables showing COVID’s impact on expenses, including on health. Quebec and British Columbia provided tables showing COVID’s impact on some categories of expense, including health.

The federal public accounts did not provide COVID impact numbers in tables. It provided some expense numbers, and qualitatively discussed most revenue measures, in the text. Its only revenue impact numbers were for the misclassified GST credit. Saskatchewan, Alberta, Yukon and Nunavut provided federal transfer revenues in text or footnote commentary only. Newfoundland and Labrador, and New Brunswick, provided no numbers on COVID’s impact in their public accounts.

Variances to Plan by Major Item

Since legislators or other interested persons seeking to understand COVID’s impact on various elements of revenue and expense could not find a complete presentation in the public accounts of any government except the Northwest Territories, they might resort to comparing pre-COVID plans to results in more detail.

We have already noted some problems with pre-COVID projections: PEI and Newfoundland and Labrador presenting their 2020/21 budgets and their 2019/20 fiscal updates too late to provide pre-COVID projections, and the Northwest Territories using different accounting in its budget than in its financial statements. Going deeper brings a further problem to light: a frustrating lack of detail on categories of revenue and expense.

The fiscal updates we resorted to for governments that presented budgets late or not at all provided less information than budgets likely would have. The federal fiscal update in 2019, for example, did not project health spending specifically. New Brunswick’s 2020/21 budget presented estimates for categories of revenue for the prior year, but not for categories of expense. Saskatchewan’s companion document to the 2019/20 Saskatchewan budget we use for Saskatchewan’s pre-COVID baseline provided no details in its projections.

What does the available information reveal? We look first at non-interest revenues – that is, revenues excluding investment income – then at non-interest (program) expenses, then at net debt-servicing costs, and finally at bottom lines.

Changes and Variances in Revenues

A key distinction for provincial/territorial governments is between revenues they raise themselves from taxes and fees – “own-source revenues” – and transfers from the federal government. With COVID lockdowns and low commodity prices pushing revenues down and Ottawa ramping up spending, we can expect different patterns in the two categories.

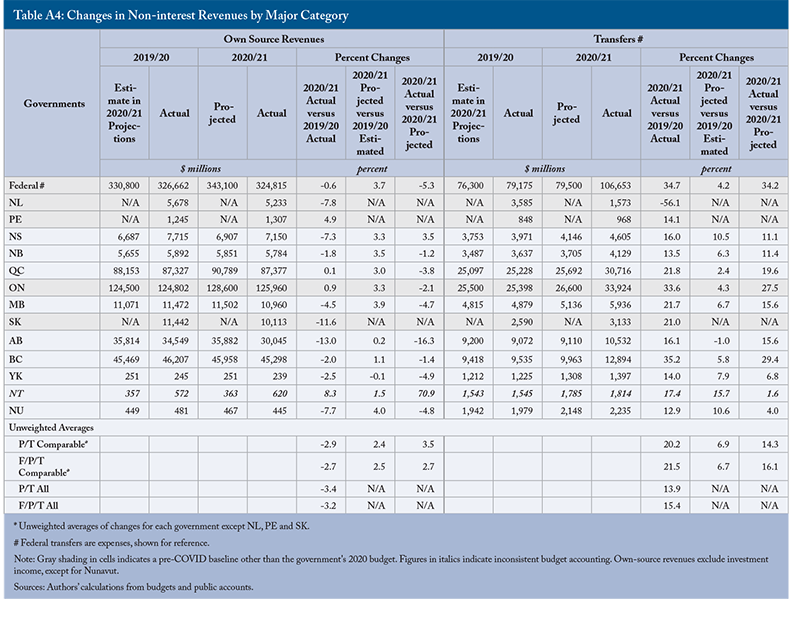

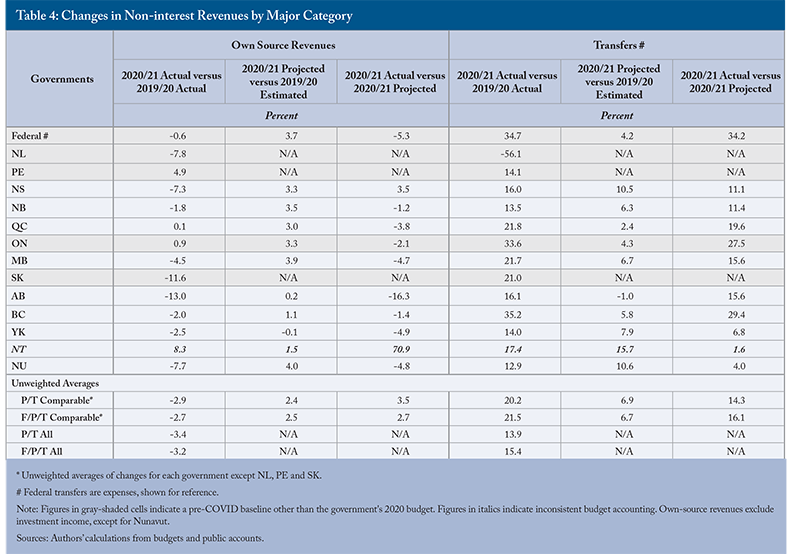

The prior-year, projected and reported amounts for own-source revenues and intergovernmental transfers appear in Table 4. Again, we show figures for governments with inconsistent accounting in italics and figures for governments without suitable 2020 budgets in gray-shaded cells. Because it is convenient to see the federal government’s transfers alongside the provincial and territorial receipts, rather than in a separate table, Table 4 shows them also as a memo item (they are expenses, not revenues, for the federal government).

Own-source Revenues Excluding Investment Income: These revenues were lower in 2020/21 than in 2019/20 for 10 of the 14 governments. Saskatchewan and Alberta suffered the largest declines. We note again that the federal government’s practice of netting the GST Credit against revenue exaggerates its decline. The average decline in these revenues across all 14 governments was 3.2 percent; among those for which we can make comparisons to projections (that is, not Newfoundland and Labrador, PEI or Saskatchewan), the average decline was 2.7 percent.

These revenues also fell short of projections for most of the governments for which we can make the comparison (not Newfoundland and Labrador, PEI or Saskatchewan). Comparing projected versus reported percent changes, we see that most governments projected increases in own-source revenues – 2.5 percent on average. Especially if they privately expected actual revenues to exceed the published projections, as history suggests they might have, the average decline of 2.7 percent – a shortfall of 5.2 percent relative to projections – was a sharp one.

Federal Transfers: The federal government’s major transfers to other governments were way up in 2020/21 – more than one-third more than in 2019/20, and more than one-third above what its 2019 Fall Update projected. The difference between the 4.2 percent increase in these transfers prefigured in the Update and the increase that actually occurred reflects the size of the federal government’s COVID-related grants. Every province and territory except Newfoundland and Labrador (which had received the large Atlantic Accord transfer in 2019/20) experienced a double-digit percent increase in federal transfers in 2020/21. The provinces and territories for which we can make the comparisons projected healthy increases in federal transfers – 6.9 percent on average. Those same provinces and territories experienced an actual increase averaging 20.2 percent – 13.3 percentage points better than projected.

Variances in Program Expenses by Government

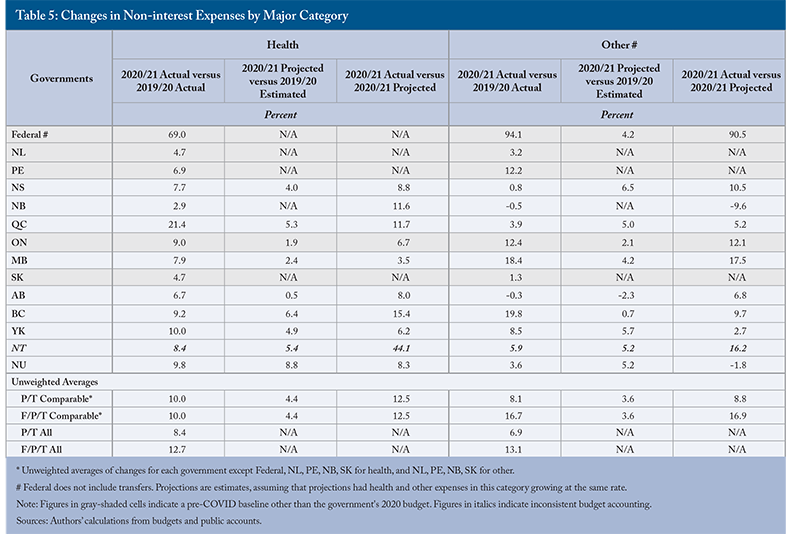

On the expense side, legislators and citizens would probably want to see projections and results for healthcare-related expenses and other expenses separately.

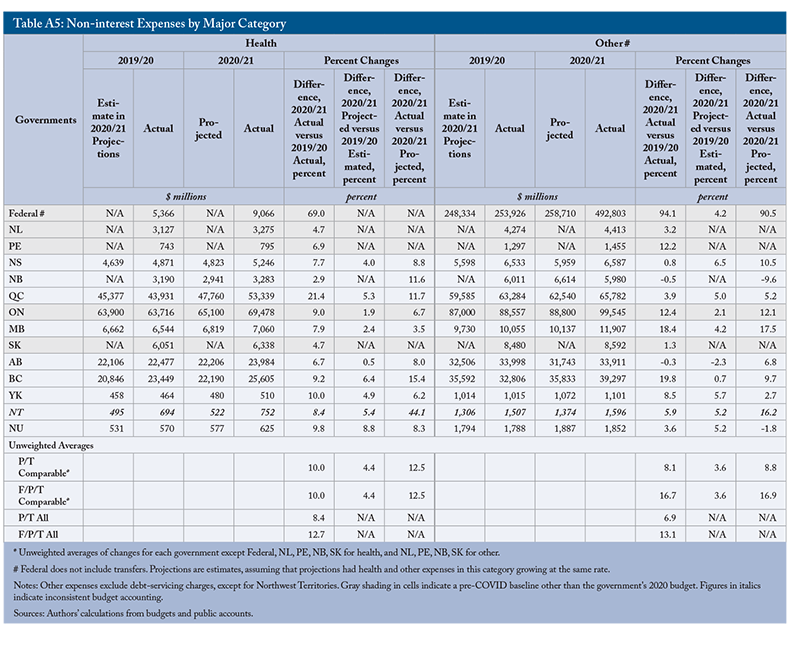

Health Expenses: Not surprisingly, expenses under the health heading were markedly higher everywhere in 2020/21 than in 2019/20. The increase among provincial and territorial governments was 8.4 percent. Ottawa’s direct spending on health was much smaller, as a share of its total expense, than was the case for provinces and territories, which means that the COVID-related increase in it, though relatively small in dollar terms, was very large – almost 70 percent – in percentage terms. Adding that raises the all-government average to 12.7 percent.

Gaps in the data make generalizing about variances from projections hard: We have no projections for health spending from the federal government, Newfoundland and Labrador, PEI, New Brunswick or Saskatchewan. Among the nine governments we can compare, the projected increase in health spending averaged 4.4 percent, and the reported increase averaged 10.0 percent, for an average overshoot of 5.6 percentage points. Governments have tended to overshoot their projections on health expenses (Robson 2020) as they have tended to overshoot their expense projections generally, but COVID’s impact shows in the size of the 2020/21 overshoots. A remarkable feature of the health expense figures is the variation in increases and overshoots across governments – a point we return to in looking at health impacts and economic variables later.

Other Program Expenses: Most governments also recorded hefty increases in other program (non-interest) expenses. The average increase from 2019/20 across the provinces and territories was 6.9 percent. Only New Brunswick and Alberta recorded declines in non-health program expenses.

Because non-health program expenses are a residual, we can only make reported-to-projected comparisons for the governments that published projections for health expenses. Among the provincial/territorial governments we can compare, the average projected increase in non-health programs averaged 3.6 percent and the actual increase averaged 8.1 percent, for an average overshoot of 4.5 percentage points. Since governments typically overshoot their expense projections, not all of this overshoot stands out as unusual. What does stand out, as in the comparison of increases and overshoots in health spending, is variation across governments, with non-health program spending growing modestly and/or undershooting in New Brunswick, Quebec and Alberta, and growing faster and/or overshooting in Nova Scotia, Ontario, Manitoba, and British Colombia.

We do not have health expense projections for the federal government, and therefore cannot produce exact projections for its non-health expenses. But federal direct health expenses are quite small: $5.4 billion out of total non-interest, non-transfer expenses of $254 billion in 2019/20. So a reasonable guess at the growth rate of health expenses underlying the 2019 Fall Update’s numbers would produce a serviceable estimate of the growth rate of everything else. For example, subtracting reported 2019/20 health expenses from non-interest, non-transfer expenses estimated in the Update, and assuming that all non-interest, non-transfer expenses were projected to increase at the same rate in 2020/21, yields a projected increase in non-transfer program expenses, excluding health, of 4.2 percent in the Update, which is the number we show in Table 5.

The reported increase in federal non-transfer program expenses excluding health in 2020/21 was 94.1 percent. Ottawa responded to the pandemic by boosting spending on many existing income-support programs and adding new ones. Among the boosted programs were seniors’ benefits, employment insurance benefits, and child benefits. (It also boosted the GST Credit – which, as we have noted, it inappropriately shows as lower revenue rather than higher expense.) Among the new programs were the Canada Emergency Response Benefit and the suite of Canada Recovery Benefits that succeeded it (Finance Canada 2021, pp. 20-22) and the Canada Emergency Wage Subsidy.

Federal spending also grew in areas less obviously related to COVID. Ottawa’s compensation costs rose by about $4.4 billion, or 8 percent, in 2020/21, and it booked about $10 billion for contingent liabilities related to indigenous child welfare – an amount added to expenses, in an unprecedented move, after the federal auditor general had already signed its 2020/21 financial statements. It is reasonable to wonder if COVID provided cover for other increases in federal spending. Adding the federal government’s reported 94.1 percent increase in program expenses other than health and transfers to the average of all governments for which we can make the year-over-year comparison raises the average increase to 16.7 percent.

Variances in Net Debt Servicing Costs by Government

The cost of servicing their accumulated deficits influenced senior governments’ 2020/21 results less than many items discussed so far. It merits a look nevertheless, partly because of some unusual federal numbers, and mainly because the increases in their accumulated deficits – the federal government again being the standout – will make the cost of debt servicing more of an issue in the years ahead than it has been for a long time.

In looking at the implications of governments’ accumulated surpluses or deficits for their future budgets and financial results, both investment income and interest payments matter. Alongside their market debt and other liabilities, Canada’s senior governments have financial assets that yield revenue, such as equity in Crown corporations. The net amount – investment income minus interest payments – is the flow that corresponds to the accumulated surplus or deficit.

Once again, cross-government comparisons require some notes about differences in presentations.

Unrecognized Pension Liability: One wrinkle is that the federal government under-records the cost of the pensions its employees earn while they are working.

Other Wrinkles: A second wrinkle is that the government of the Northwest Territories shows projected interest expense in its budget, but does not report it separately in its financial statements after year-end.

A third wrinkle is that Nunavut does not separate out investment income in its budget. Nunavut’s investment income is included in its own-source revenue, so we do not have comparable numbers for Nunavut.

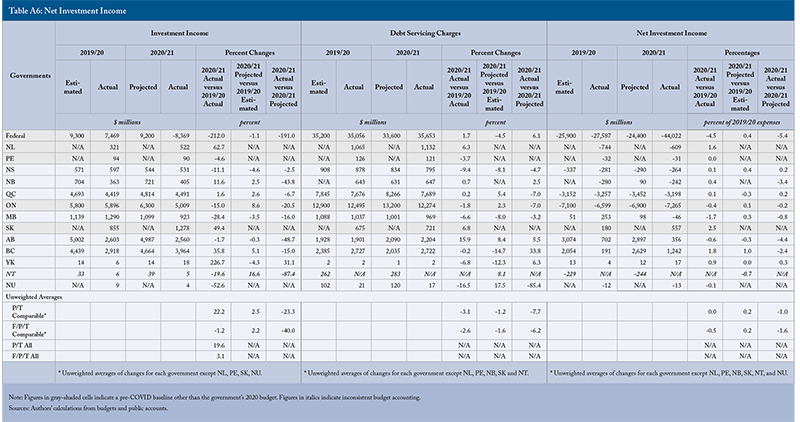

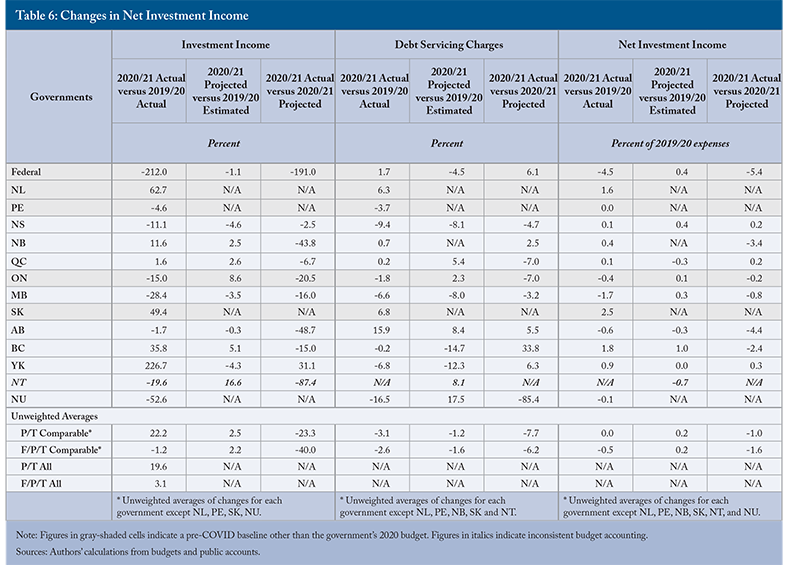

Table 6 shows the changes in investment income and interest payments for all the governments that published the relevant numbers, as well as the difference between them: net investment income (a version of this table with the dollar amounts is in the online Appendix). Again, figures for governments with accounting discrepancies are italicized, and figures for governments without suitable baseline budgets are in gray-shaded cells.

Investment Income: The provinces and territories generally reported lower investment income in 2020/21. Seven of the 13 reported lower investment income than in the previous year. Eight of the nine for which we can make the comparison reported investment income lower than projected – not surprising in a year when lack of demand for credit as well as central bank liquidity injections kept interest rates very low and a weak economy hurt the financial performance of Crown corporations.

The federal government’s investment income in 2020/21 was worse than low. Instead of the revenue of $7.5 billion reported in 2019/20, or the revenue of $9.2 billion projected in the 2019 Update, it reported a negative figure of $8.4 billion – hence the remarkable negative changes and variances of about 200 percent.

Debt-Servicing Charges: Turning to interest payments, 2020/21’s results relative to 2019/20’s results and to 2020/21’s projections are a mixed bag. In some cases, the low interest rates that prevailed during the pandemic dominated the result; in others, the higher debts run up over the year dominated. Among the 13 governments for which we can compare 2020/21 to 2019/20 (not the Northwest Territories, which does not report interest expense), seven reported lower payments in 2020/21, and the average across all the governments was a decline of 2.6 percent. Among the nine governments for which we can compare 2020/21 results to projections (not Newfoundland and Labrador, PEI, New Brunswick, Saskatchewan or the Northwest Territories), five overshot and four undershot, with the larger undershoots producing a negative all-government average.

As for the net number – debt-servicing costs minus investment income – gaps in the data mean we can only make full comparisons with previous results and projections for eight provincial or territorial governments. (For this comparison, we scale to 2019/20 expenses to avoid distorted percent changes from numbers close to zero.) Most of those eight did worse than projected, with the average provincial/territorial shortfall coming in at 1.0 percent of 2019/20 expenses. Ottawa yet again stands out: thanks to its negative investment income, its net debt servicing charges in 2020/21 were higher than its gross debt servicing charges. The deterioration in its net investment income was equal to about 4.5 percent of its 2019/20 expenses, and fell short of projections by an amount equal to 5.4 percent of its prior-year expenses. Averaging across all nine governments for which we can make the comparisons, net investment income was lower in 2020/21 than in 2019/20, and worse than projected by 1.6 percent of 2019/20 expenses. The influence of higher accumulated deficits outweighed the influence of lower interest rates.

Variances in Bottom Lines by Government

Finally, we turn to the variances between fiscal plans and results on the bottom line. How did the surpluses or deficits prefigured in budgets and other projections compare to the reported changes in accumulated surpluses or deficits during 2020/21?

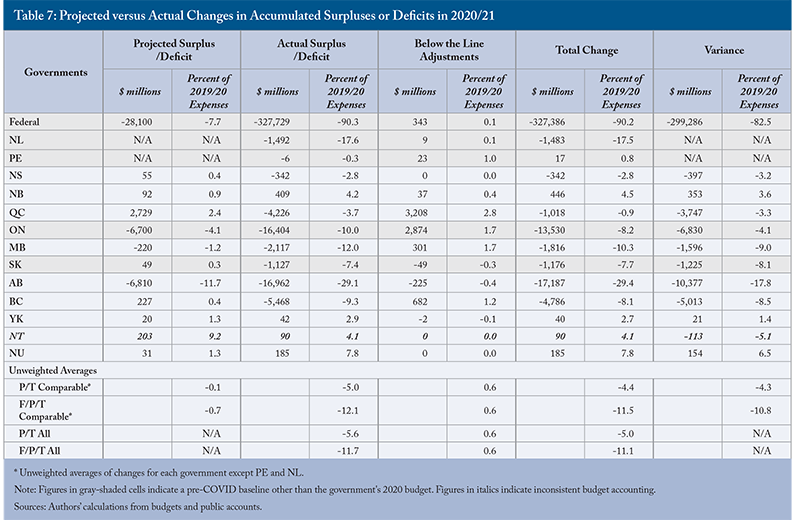

We already explored the variances between the changes governments projected and reported in their revenues and expenses and bottom lines, expressed in percentages. That gave a flavour of the variances – mostly negative, often spectacularly so. Table 7 also shows the numbers in levels – a closer inspection justified by two considerations.

One reason is simply that changes in governments’ accumulated surpluses or deficits matter so much. Governments’ net worth reflects their capacity to deliver services in the future, which COVID markedly affected.

Beyond that point of emphasis is a point of substance. A government’s projected surplus or deficit may not accurately prefigure the change in its accumulated surplus or deficit. Governments’ financial statements often include adjustments below the annual surplus or deficit, reflecting changes in their accumulated surpluses or deficits beyond those reported in their statements of operations.

These below-the-line adjustments have justifications, such as when they report gains or losses related to a Crown corporation operating at arm’s length. But they are a challenge for legislative control of public funds, since legislators cannot see nor vote on them ahead of time (Robson and Dahir 2022). So in addition to the variances in surpluses or deficits, Table 7 includes any below-the-line adjustments, and shows the total change in governments’ accumulated surpluses and deficits in relation to the fiscal plan.

Although the size of the deficits projected by the federal government and Alberta make the all-government average slightly negative – 0.7 percent of 2019/20 expenses – most of the 12 governments for which we have useable numbers (not PEI or Newfoundland and Labrador) projected surpluses in 2020/21. Except for New Brunswick and the territories, all of them reported deficits. The provincial/territorial average deficit was 5.0 percent of 2019/20 expenses, and the federal government’s enormous deficit – equal to more than 90 percent of its prior-year expenses – pushes the average of all the government providing comparable numbers down to 12.1 percent.

The below-the-line adjustments in 2020/21 mitigated that result. They were positive for eight of the 11 governments that reported such adjustments, producing an average boost to bottom lines equal to 0.6 percent of 2019/20 expenses.

Notwithstanding those boosts, nine of the 14 governments reported deteriorations in their accumulated surpluses or deficits in 2020/21. As noted already, the all-government average deterioration equaled about 11 percent of 2019/20 expenses. The net impact of smaller than usual revenue overshoots, larger than usual expense overshoots, worse net investment income and a boost from below-the-line adjustments was a sharp deterioration in net worth compared to 2019/20 – one that exceeded average projections by about the same amount.

Highlights and Discussion

Our discussion of the gaps and discrepancies in governments’ financial presentations highlights some obstacles to assessing the fiscal impact of COVID. Aside from the inevitable problems of establishing plausible pandemic-free baselines, the information governments provided about their plans for 2020/21 was inadequate.

Impact of COVID on Health Expenses

In the first full pandemic fiscal year, 2020/21, the impact of COVID on expenses in general, and on health expense in particular, is naturally a top-of-mind question. Governments spent a lot more than they did in the previous year and a lot more than they projected. What did they spend it on, and to what effect?

Our goal in this report has been to rely on the key documents legislators use, and in understanding what happened in 2020/21, the public accounts would ideally be an adequate source of information. Since governments’ disclosure of COVID-related expenses in their 2020/21 public accounts was uneven, however, we consult two other sources.

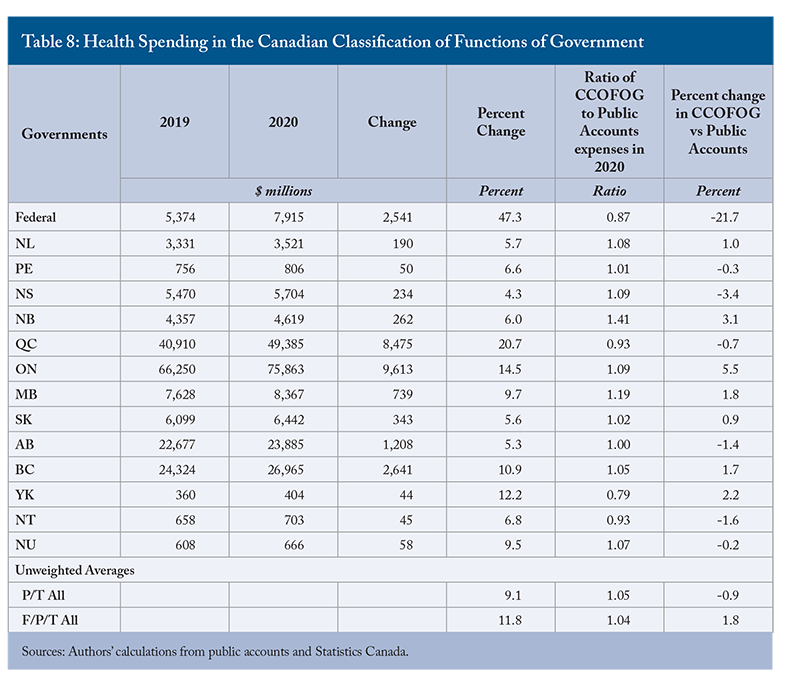

Table 8 shows spending on health in 2019 and 2020 as calculated by Statistics Canada’s Canadian Government Finance Statistics program in its Canadian Classification of Functions of Government (CCOFOG) compilation, and the percent changes between them.

These numbers differ from those underlying Table 5 and in online Appendix Table A5 for several reasons. The CCOFOG counts healthcare spending by the federal government more narrowly than the federal public accounts, eliminating Health Canada transfers to the provinces to avoid double counting. To facilitate comparisons among governments with different sub-jurisdictional arrangements, the CCOFOG consolidates all entities under provincial/territorial jurisdiction, notably health and social service institutions, municipalities and other local public administrations. In addition, as noted above, Quebec, Yukon and the Northwest Territories aggregate health and other social services in their public accounts, so the CCOFOG numbers for them are smaller than those in Table A5.

Using the CCOFOG tally for the provinces and territories slightly lowers the average change in health spending from 2019 to 2020 for those governments to around 9 percent. The CCOFOG shows smaller percent increases in health spending than the public accounts for half the provincial and territorial governments – PEI, Nova Scotia, Quebec, Alberta, Northwest Territories, and Nunavut – and larger percent increases for the other half of provincial and territorial governments – Newfoundland and Labrador, New Brunswick, Ontario, Manitoba, Saskatchewan, British Colombia, and Yukon. The CCOFOG’s narrower definition for the federal government produces a smaller percent increase for it – 47 compared to less than 70 using the public accounts.

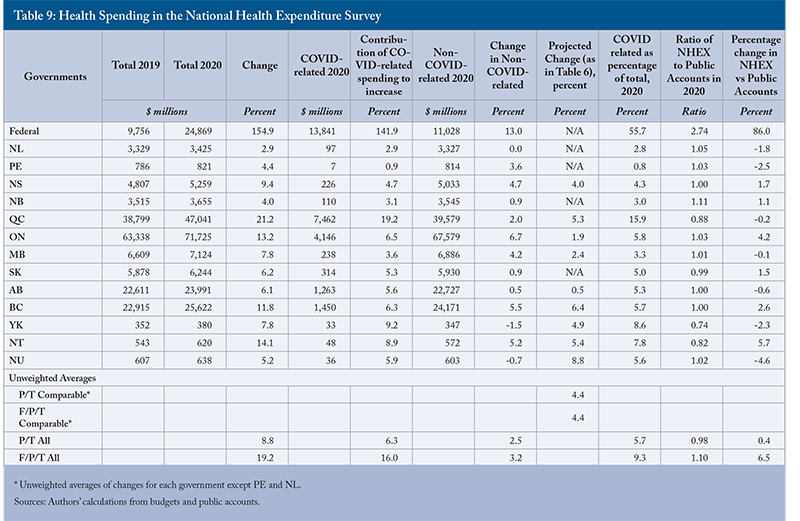

A second source of health-spending data is the annual National Health Expenditure (NHEX) Survey from the Canadian Institute for Health Information (CIHI). The CIHI numbers on health spending also differ in several ways from those underlying Table 5 and appearing in Table A5. The NHEX uses calendar years: combining one-quarter of governments’ expenses from the fiscal year covering the January-March period with three-quarters of their expenses from the fiscal year covering the April-December period. The NHEX tries to measure on a consistent basis across governments that allocate healthcare responsibilities differently between the provincial government itself, and social service agencies and municipalities.

Unlike the CCOFOG, the NHEX survey measures healthcare spending by the federal government more broadly than the federal public accounts, which tally expense under Health Canada. The NHEX survey includes direct health spending by other departments, including spending on particular groups such as the military and First Nations, as well as direct federal spending on health research, protection and promotion. Like the CCOFOG, the NHEX shows smaller numbers for the governments that include other social services with health in their public accounts: Quebec, Yukon and the Northwest Territories. Helpfully, recent NHEX compilations have attempted to isolate spending on COVID from other health spending. Table 9 shows spending on health from the NHEX in 2019 and 2020 by government, and shows the growth rates including COVID-related spending and without it.

Among the provinces and territories, the average change in health spending from 2019 to 2020 calculated from the NHEX is only slightly higher than the change calculated from the public accounts – 8.8 percent rather than 8.4 percent.

Pandemic Health Spending: The NHEX’s breakout of COVID-related spending should shed light on the contribution of COVID to overall health spending growth – and, by subtraction, shed light on what happened to non-COVID-related spending across the governments in 2020. The NHEX numbers show that COVID boosted the average increase in health spending across the provinces and territories by 6.3 percent. That is not a remarkable average, but the range – stretching from an almost imperceptible 0.9 percent COVID-related boost to health spending in PEI to a colossal 19.2 percent boost in Quebec – cries out for explanation.

Non-Pandemic Health Spending: As for non-COVID-related health spending, these numbers suggest that the average increase across the provinces and territories was 2.5 percent in 2020. Again, while the average seems reasonable, the range is oddly wide. Non-COVID spending apparently fell in Yukon and Nunavut, rose by little or nothing in Newfoundland and Labrador, New Brunswick, Saskatchewan and Alberta, and rose more than 5 percent in Ontario, British Columbia and the Northwest Territories.

Table 9 reproduces from Table 5 the percentage increase in health expense prefigured in the budgets or projections of the governments that provided such numbers before COVID struck. Notwithstanding the differences in measurement, the NHEX tallies are mostly close enough to the public accounts totals to let us compare the NHEX’s increases in non-COVID-related health spending to the projections from governments that provided useable figures. This approach also suggests a wide range of responses. Some governments appear to have managed growth rates in non-COVID health spending close to their projections – in Alberta’s case, identical to them. In other cases, and reflected in the unweighted average across the provincial and territorial governments, growth in non-COVID-related health spending was less than projected, suggesting a diversion of resources from other health services, as in the cases of Quebec, Yukon and Nunavut. Ontario is a notable case of the opposite, with growth in non-COVID-related spending well beyond what it projected. The federal government’s pre-COVID projections did not isolate health spending so we can make no meaningful comparison for it.

To repeat, we resort to the CCOFOG and NHEX numbers because the information in governments’ public accounts on health spending was so uneven and health spending is a key area of interest in a crisis such as COVID. Legislators did not have these sources, and ideally should not need them. Budgets and public accounts that were more timely and complete would have helped them understand, and approve, or not, their own governments’ responses, without seeking and waiting for other compilations.

Does Varying Experience with COVID Explain Differences among Governments?

Did the contrasting fiscal experiences of provincial and territorial governments reflect differences in factors such as lower economic activity due to spontaneous reactions and official restrictions, and the number and severity of COVID infections? A comprehensive account of the interplay between pandemic, economic and fiscal factors is beyond the scope of this paper (see Di Matteo 2022 for more on this), but we can scan a few summary indicators.

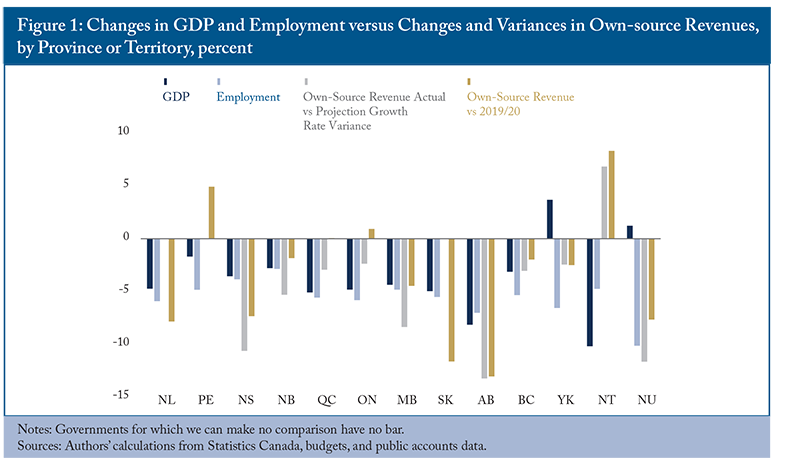

On the revenue side, we might expect lower economic activity to correlate with declines in own-source revenue and/or shortfalls in own-source revenue relative to projections. We use real GDP and employment to check that – GDP because it is a more comprehensive measure that correlates with governments’ tax bases, employment because we can use monthly figures to get measures that match the fiscal year.

Manitoba’s experience is perhaps most in line with what we might expect, with declines in GDP, employment, and a shortfall in own-source revenue between 4 and 5 percent. Newfoundland and Labrador, Saskatchewan and Alberta, suffered relatively large declines in GDP and employment, and experienced relatively large declines in revenue – though in Alberta’s case, revenue out-performed gloomy projections. Quebec and Ontario were also quite hard hit economically, but their own-source revenues, though below projections, were up year-over-year.

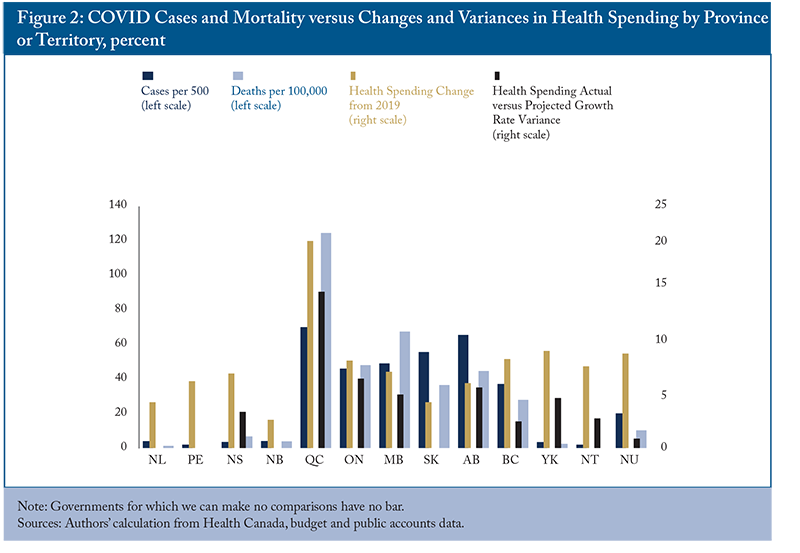

On the spending side, it is less clear what to expect. Extraordinary public-health measures might produce a negative correlation between expenses and COVID’s severity. Or more severe COVID might produce more health spending. Figure 2 shows two measures of severity – cases and deaths relative to population – alongside changes in health expense between 2020/21 and 2019/20, and variances between projected and actual changes in health expense (where we have projections). Cases and mortality data are cumulative cases and deaths since the start of the pandemic until the last observation in the 2020/21 fiscal year, from the Government of Canada’s weekly COVID-19 epidemiology update.

The picture is indeed mixed. COVID hit Quebec harder than any other province, as measured by cases and deaths. That seems a reasonable explanation for Quebec’s big increase in health expenses, and country-leading over-run relative to projections. The experience from Ontario west, however, shows no obvious correlation between the severity of COVID and the increases and over-runs in health expenses. The Atlantic Provinces are in a different category altogether, with much lower rates of morbidity and mortality from COVID, but similar magnitudes of health expense increases and overruns. It is asking a lot of public accounts data to help legislators figure out if, say, the Atlantic Provinces succeeded in containing COVID better with their health-expense increases. But these documents are a key source, and it would be better if governments themselves had provided more comprehensive accounting of the fiscal impact of COVID and their responses.

Notwithstanding shortfalls relative to own-source revenue projections in some provinces and territories – a contrast to the historical pattern of revenue under-projections – and the decline in the federal government’s revenues, a striking feature of 2020/21 is the robustness of revenues overall. Revenues were higher in 2020/21 for 10 of the 14 governments. Own-source revenues were sharply lower in the resource-dependent provinces, but not in most others – the federal government’s transfer payments to individuals and businesses supported nominal income and spending, and boosted provincial/territorial tax bases. Federal direct transfers to these governments also made a huge difference, turning what would have been year-to-year declines into increases for four of them.

The importance of indirect and direct federal support to provincial and territorial governments in 2020/21 merits emphasis because so much of it was temporary. The federal government was only able to borrow as much as it did during the pandemic because the Bank of Canada bought the greatest part of the bonds it issued. With the resulting liquidity having pushed CPI inflation more than 6 percentage points above the 2 percent target agreed between the government and the Bank, the Bank has stopped buying federal bonds and is letting its existing holdings mature. Inflation continued to boost nominal incomes and spending, and therefore tax revenues, in 2021/22 (Sondhi 2023), but a return to 2 percent inflation and a weaker economy will likely produce at least a couple of years of revenue growth in low single digits. In a sense, some of the revenue shortfalls we might have expected when a pandemic stunted or shut down large parts of the economy are still to come.

Varying Increases in Non-Health Expenses

Changes in program expenses other than health across the governments call out for investigation. Two governments – New Brunswick and Alberta – reported lower non-health program expenses in 2020/21 than in 2019/20. Among the nine governments for which we can compare results to projections, three – Nova Scotia, Quebec and Nunavut – undershot their non-health program expense projections. That might indicate that they diverted resources to COVID while trying to stay closer to their overall fiscal frameworks. Other governments – notably Ontario, Manitoba and British Columbia – reported non-health program expenses sharply higher than both the previous year and projections.

Because the federal government’s 2019 Fall Update projections did not show health expenses, we have no exact figure for its overshoot of non-health (and non-transfer) program expenses. But the increase – these expenses almost doubled in 2020/21 – was so colossal that we can estimate its magnitude without knowing the exact amount. The federal government overshot its projected expenses on items other than interest, intergovernmental transfers and health by more than $230 billion. Parliament played virtually no role in overseeing or approving this spending. Although the federal government at first issued weekly bulletins on disbursements through the Canada Emergency Wage Subsidy, these reports ceased in late 2021, and no comparable reports on that program’s successors or other support payments occurred (Brethour 2022). Not even the finance minister, let alone parliamentarians, knew in advance what the prime minister would announce the next day.

The Hidden Cost of Servicing Higher Net Debt

Another important feature of the fiscal experience of Canada’s senior governments in the pandemic year was their weak net investment income. Despite rock-bottom interest rates and the Bank of Canada’s purchases of debt, four of the nine governments for which we can make the comparisons undershot their projections due to some combination of higher than projected interest payments and lower than projected investment income.

The weakness in the federal government’s net investment income merits particular attention. Focusing on interest payments alone masks the extent to which ballooning debt affected the federal budget in the pandemic year. As previously mentioned, the Bank of Canada’s acquisition of federal government bonds on the market resulted in a significant markdown and negative investment income. The Bank financed those purchases using settlement balances, incurring interest costs at the overnight rate. During the pandemic year, the overnight rate was so low – the Bank’s target was 0.25 percent – that the yields on the bonds exceeded the financing cost, producing a profit for the Bank. If the overnight rate had remained near zero, the profits made by the Bank and remitted to the government could have slowly compensated for the one-time balance-sheet markdown. However, the recent, successive hikes of the target overnight rate mean that the Bank of Canada will pay more in financing costs than it gets on the bonds, meaning losses for the Bank and lower investment income for the government in the future (Tombe and Chen 2023; Ambler, Koeppl and Kronick 2022).

The results for gross interest payments suggest that some governments paid less to service their debt in 2020/21 than they had the year before or than they projected. But net investment income, the appropriate flow to set against the stock of net debt, reveals that the costs of higher borrowing outweighed the savings from lower interest rates even in the pandemic year – a sign of things to come.

An overarching theme of this review of COVID’s impact on the finances of Canada’s senior governments – arguably as important as any of the observations we have made on revenues, expenses and accumulated surpluses or deficits – is the lack of relevant information. The first pandemic fiscal year 2020/21 highlighted gaps in the formal processes of accountability and in the timeliness, completeness and reliability of the information governments provided to legislatures and the public.

Nova Scotia, New Brunswick, Quebec, Manitoba, Alberta, British Columbia, Yukon, the Northwest Territories and Nunavut presented timely budgets for 2020/21. But Ontario, Newfoundland and Labrador, Saskatchewan and Prince Edward Island did not, and the federal government produced no budget at all.

For a review such as this, resorting to previous fiscal updates to get projections for 2020/21 in the cases of the federal government and Ontario, and using other proxies for such projections in the case of Saskatchewan, is more complicated to do and explain than is ideal. But those frustrations are small compared to the larger issue: namely that elected representatives in the legislatures concerned had no opportunity to approve spending before the fiscal year began. An egregious attempt to escape legislative scrutiny was the federal government’s late-March 2020 draft bill to give cabinet authority to spend, levy new or increased taxes, and borrow without parliamentary approval (Stephenson and Connolly 2020). Although the resulting uproar led the government not to proceed with that proposal, it did not present a budget in 2020 – a deeply troubling precedent.

Federal members of parliament were in a particularly a weak position to understand the fiscal implications of economic developments and measures the federal government undertook during the pandemic. But in many other jurisdictions – notably Prince Edward Island and Newfoundland and Labrador, for which we could find no projections for 2020/21 at all – legislators did not have numbers sufficient for even a superficial understanding of COVID’s impact.

The variable and generally thin information on COVID’s impact in the senior governments’ public accounts means that legislators were poorly briefed even well after the fact. After a crisis, Canadian citizens and legislators should have insight into its impact on public finances and how their governments reacted. Without that, they cannot evaluate the responses to the event, nor learn how to respond better to a future crisis.

The C.D. Howe Institute’s most recent report on the quality of these documents from the 14 federal, provincial and territorial governments (Robson and Dahir 2022) awarded grades in the A range to only two: Alberta and Yukon. Our attempt to outline, even at a high level, the fiscal developments during the pandemic year highlights additional gaps – notably with respect to the time horizons and detail in fiscal projections – that legislators in all jurisdictions should work to fix.

Fiscal Accountability Post-COVID

Although our understanding of the longer-term impacts of the pandemic on health, the economy and public finances is still incomplete, they appear to be almost uniformly and strongly negative. COVID’s impact on health and human capital formation

These challenges will increase the need for legislators and the Canadians they represent to monitor the capacity of their governments to finance services. While many of the formal mechanisms of accountability exist in Canada, the projections in the budgets and fiscal updates of Canada’s senior governments have consistently under-projected revenue and spending, suggesting that legislators were not getting reliable information, and did not demand better.

The COVID-19 crisis highlighted some particular problems. The coincidence of the pandemic starting toward the end of the 2019/20 fiscal year highlighted the difference between governments that presented timely budgets and those – the no-budget federal government worst of all, but also Newfoundland and Labrador, Prince Edward Island, Ontario, and Saskatchewan – that did not. Future engagement by legislator and the public, and improved accountability for budget presentations and outcomes, will be greater if all senior governments present budgets before the end of February.

It also highlighted deficiencies in the way some governments report their revenues and expenses. Governments should show returns on investment as a distinct category of revenue. Governments should show the cost of servicing their liabilities, market debt and other liabilities such as pensions, as a distinct category of expense – not show some items separately from expenses as the federal government does with some of its pension costs, or leave interest costs out of its public accounts, as the Northwest Territories does. A useful supplementary table in the public accounts could show both investment income and debt servicing costs, provide a net number, and show how it relates to the accumulated surplus or deficit.

Governments should show gross revenue and expenses, not netting some expenses against revenues as the federal government does with the GST credit. Governments should show key items in detail in their projections, including transfers of all kinds and spending on major programs such as healthcare.

Legislators, including legislators aligned with government parties, need to be more aggressive in scrutinizing expenses both before and after they are incurred. The federal government’s reopening of its books after the federal auditor general had already signed off to back-date about $10 billion in spending is a dismaying bookend to a year that started with no budget, underlining the extent to which legislators lost their will and ability to act as stewards of public funds in 2020/21. The dearth of systematic numbers on COVID’s fiscal impact in public accounts showed that governments did not, in general, provide information commensurate with the scale of a crisis unlike anything Canada has experienced since the Second World War.

If legislative control over public money is to be more than a fiction, legislators need to exert their powers more, notably in demanding better fiscal transparency and accountability. Budgets should precede the start of the fiscal year, and provide the detail legislators require to understand the fiscal plan. Public accounts with financial statements should appear promptly after fiscal year-end, and provide the information needed – as too many governments’ public accounts for 2020/21 did not – to understand variances from plans, and how major events such as COVID affected those outcomes.

COVID’s fiscal impact has raised the stakes. More than ever, legislators and voters should demand that Canada’s federal, provincial and territorial governments improve their budgeting processes and their transparency about how well, or badly, they fulfill their budget commitments. The pandemic prompted increases in expenses that will persist for years and increases in debt that will persist for decades. Legislators and voters should demand more timely and complete fiscal plans, and better accounting for success or failure in achieving them, in the future.

References

Publications Other Than Government Financial Documents.

Ambler, Steve, Thorsten Koeppl and Jeremy Kronick. 2022. The Consequences of the Bank of Canada’s Ballooned Balance Sheet. Commentary 631. Toronto: C.D. Howe Institute. November.

Agrawal, David R., and Aline Bütikofer. 2022. “Public Finance in the Era of the COVID-19 Crisis.” GLO Discussion Paper, No. 1176, Global Labor Organization (GLO), Essen.

Brethour, Patrick. 2022. “Tax & Spend: Ottawa’s silence on hiring subsidy statistics is a secret wrapped in a mystery.” The Globe and Mail. May 30. https://www.theglobeandmail.com/investing/personal-finance/taxes/article-ottawas-silence-on-hiring-subsidy-statistics-is-a-secret-wrapped-in-a/

Finance Canada. 2021. Annual Financial Report of the Government of Canada, 2020-2021.

Di Matteo, Livio. 2022. “Storm without End: The Economic and Fiscal Impact of COVID in Canada.” Vancouver: Fraser Institute.

Halloran, Clare, Rebecca Jack, James C. Okun and Emily Oster. 2021. “Pandemic Schooling Mode and Student Test Scores: Evidence from US States,” NBER Working Paper 29497. National Bureau of Economic Research. November.

Laurin, Alexandre, and William B.P. Robson. 2020. “Under the Rug: The Pitfalls of an “Operating Balance” Approach for Reporting Federal Employee Pension Obligations.” E-Brief. Toronto: C.D. Howe Institute. November.

Laurin, Alexandre, and Don Drummond. 2021. “Rolling the Dice on Canada’s Fiscal Future.” E-Brief. Toronto: C.D. Howe Institute. July.

Mahboubi, Parisa. 2019. Intergenerational Fairness: Will Our Kids Live Better than We Do? Commentary 529. Toronto: C.D. Howe Institute. January.

Morneau, Bill. 2023. Where To From Here: A Path to Canadian Prosperity. Toronto: ECW Press.

Robson, William B.P. 2020. There is No Try: Sustainable Healthcare Requires Reining in Spending Overshoots. Commentary 566. Toronto: C.D. Howe Institute. February.

Robson, William B.P., and Alexandre Laurin. 2017. Hidden Spending: The Fiscal Impact of Federal Tax Concessions. Commentary 469. Toronto: C.D. Howe Institute. February.

Robson, William B.P., and Miles Wu. 2021a. Good, Bad, and Incomplete: Grading the Fiscal Transparency of Canada’s Senior Governments, 2021. Commentary 607. Toronto: C.D. Howe Institute. September.

____________. 2021b. Trouble on the Bottom Line: Canada's Governments Must Produce More Reliable Budgets. Commentary 611. Toronto: C.D. Howe Institute. November.

Robson, William B.P., and Nicholas Dahir. 2022. The Right to Know: Grading the Fiscal Transparency of Canada’s Senior Governments, 2022. Commentary 628. Toronto: C.D. Howe Institute, September.

Sondhi, Rishi. 2023. “2023 Budget Season Recap: Windfalls, Tax Relief, Spending.” TD Economics. April 26.

Stephenson, Mercedes, and Amanda Connolly. 2020. “Liberal bill on coronavirus would give feds power to spend, tax without parliamentary approval.” Global News, March 30.

Tombe, T., and Chen, Yu. 2023. “Reversal of Fortunes: Rising Interest Rates and Losses at the Bank of Canada.”E-Brief. Toronto: C.D. Howe Institute. January.

Budgets and Fiscal Updates

Federal. Economic and Fiscal Update 2019. Accessible at: https://www.budget.canada.ca/efu-meb/2019/docs/statement-enonce/efu-meb-2019-eng.pdf

Newfoundland and Labrador. Fiscal Update 2020-21. Accessible at: https://www.gov.nl.ca/fin/files/Fiscal-Update-20-21-Presentation-July-24-2020.pdf

Nova Scotia. Budget 2020-21. Accessible at: https://beta.novascotia.ca/sites/default/files/documents/6-2046/ftb-bfi-041-en-budget-2020-2021.pdf

New Brunswick. 2020-21 Budget Speech. Accessible at: https://www2.gnb.ca/content/dam/gnb/Departments/fin/pdf/Budget/2020-2021/BudgetSpeech2020-2021.pdf

Quebec. The Quebec Budget Plan 2020-2021. Accessible at: http://www.budget.finances.gouv.qc.ca/budget/2020-2021/en/documents/BudgetPlan_2021.pdf

Ontario. 2019 Ontario Economic Outlook and Fiscal Review. Accessible at: https://budget.ontario.ca/2019/fallstatement/contents.html

Manitoba. Budget 2020-Budget and Budget Papers. Accessible at: https://www.gov.mb.ca/asset_library/en/budget2020/budget.pdf

Saskatchewan. Highlights of 2019-20 Budget. Accessible at: https://publications.saskatchewan.ca/api/v1/products/100136/formats/110484/download

Alberta. Fiscal Plan – A plan for Jobs and the Economy. Accessible at: https://open.alberta.ca/dataset/05bd4008-c8e3-4c84-949e-cc18170bc7f7/resource/79caa22e-e417-44bd-8cac-64d7bb045509/download/budget-2020-fiscal-plan-2020-23.pdf

British Colombia. Budget 2020. Accessible at: https://www.bcbudget.gov.bc.ca/2020/pdf/2020_budget_and_fiscal_plan.pdf

Yukon. 2020-21 Operations and Maintenance and Capital Estimates. Accessible at: https://yukon.ca/sites/yukon.ca/files/fin-2020-21-budget_en.pdf

Northwest Territories. 2020-21 Budget Address and Papers. Accessible at: https://www.fin.gov.nt.ca/sites/fin/files/resources/2020-2021_budget_address_and_papers_final.pdf

Nunavut. 2020-21 Consolidated Budget of the Government Reporting Entity. Accessible at: https://gov.nu.ca/sites/default/files/2020-21_consolidated_budget_final.pdf

Public Accounts

Receiver General for Canada. 2021 Public Accounts. Accessible at: https://www.tpsgc-pwgsc.gc.ca/recgen/cpc-pac/2021/pdf/2021-vol1-eng.pdf

Newfoundland and Labrador. 2021 Public Accounts. Accessible at: https://www.gov.nl.ca/exec/tbs/files/Public-Accounts-March-31-2021.pdf

Prince Edward Island. 2021 Public Accounts. Accessible at: https://www.princeedwardisland.ca/sites/default/files/publications/volume_1_2020-2021_web.pdf

Nova Scotia. 2021 Public Accounts. Accessible at: https://notices.novascotia.ca/files/public-accounts/2021/pa-volume-1-financial-statements-2021.pdf

New Brunswick. 2021 Public Accounts. Accessible at: https://www2.gnb.ca/content/dam/gnb/Departments/tb-ct/pdf/OC/pa-2021-v1-e.pdf

Quebec. 2021 Public Accounts. Accessible at: http://www.finances.gouv.qc.ca/documents/Comptespublics/en/CPTEN_vol1-2020-2021.pdf

Ontario. 2021 Public Accounts. Accessible at: https://files.ontario.ca/tbs-2020-21-annual-report-and-consolidated-financial-statements-en.pdf

Manitoba. 2021 Public Accounts. Accessible at: https://www.gov.mb.ca/asset_library/en/proactive/20212022/public-accounts-2021.pdf

Saskatchewan. 2021 Public Accounts. Accessible at: https://www.saskatchewan.ca/-/media/news-release-backgrounders/2021/jun/2020-21-volume-1.pdf

Alberta. 2021 Public Accounts. Accessible at: https://open.alberta.ca/dataset/7714457c-7527-443a-a7db-dd8c1c8ead86/resource/500cd6f2-9de7-41c3-94b9-966b423ad005/download/2020-21-goa-annual-report.pdf

British Columbia. 2021 Public Accounts. Accessible at: https://www2.gov.bc.ca/assets/gov/british-columbians-our-governments/government-finances/public-accounts/2020-21/public-accounts-2020-21.pdf

Yukon. 2021 Public Accounts. Accessible at: https://yukon.ca/sites/yukon.ca/files/fin/fin-2020-21-yukon-public-accounts-protected.pdf

Northwest Territories. 2021 Public Accounts. Accessible at: https://www.fin.gov.nt.ca/sites/fin/files/resources/2020-2021-public_accounts-section_i.pdf

Nunavut. 2021 Public Accounts. Accessible at: https://www.gov.nu.ca/sites/default/files/CHildDayPosters/2021_public_accounts_-_english_web_version.pdf

Other Sources

Canadian Institute for Health Information (CIHI). National Health Expenditure Trends 2022. Health spending data tables C & D4. Accessible at: https://www.cihi.ca/en/national-health-expenditure-trends.

Government of Canada. COVID-19 epidemiology update: Key updates. Accessible at: https://health-infobase.canada.ca/covid-19/#tiles.

Statistics Canada. Table 10-10-0005-01. Canadian classification of functions of government, by consolidated government component (x 1,000,000) Accessible at: https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1010000501.

Statistics Canada. Table 36-10-0402-01. Gross domestic product (GDP) at basic prices, by industry, provinces and territories (x 1,000,000). Accessible at: https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610040201.

Statistics Canada. Table 14-10-0292-01. Labour force characteristics by territory, three-month moving average, seasonally adjusted and unadjusted, last 5 months. Accessible at: https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1410029201.

Statistics Canada. Table 14-10-0287-01. Labour force characteristics, monthly, seasonally adjusted and trend-cycle, last 5 months. Accessible at: https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1410028701.

Data Sources

Online Appendix

Expanded Versions of Tables 4, 5, and 6

We present here fuller versions of these tables, showing dollar amounts as well as percent changes. We do this so readers can get additional information about the relative contributions of different items to overall fiscal impact. We also do it in case readers of the more summary tables wonder about the relationships between the overshoots and undershoots relative to projections and the final year-to-year changes. As we mentioned in our first look at projections versus results, the prior-year numbers in budgets and fiscal updates (labelled “2019/20 Estimate in 2020/21 Projections” in these tables) were not the same as the numbers for 2019/20 that appeared later in public accounts. For that reason, projected changes relative to the prior year plus the under- or overshoot relative to projections will typically not sum to the year-to-year change shown in the public accounts.