The Study In Brief

- Despite having highly similar economies, in banking the experience of the crisis-prone United States contrasts starkly with Canada’s stability.

- For each major US crisis, different reasons have been put forward to explain Canada’s comparative stability in the face of broadly similar shocks, an issue that arose again in the context of the failure of Silicon Valley Bank and its aftermath.

- This Commentary examines whether there is a unifying explanation for these contrasting outcomes and what this implies for Canada’s future financial sector stability. It identifies the changes introduced in the 1890 and 1900 Bank Act revisions that led Canada to manage banking sector problems in a cooperative arrangement between the banks and the authorities. The aim was to address the externalities generated by bank failures while controlling the resultant moral hazard through social networks rather than market discipline.

- Importantly, the system ensured enough competition to be efficient. Drawing on this comparative analysis, the Commentary considers the lessons to be drawn for future financial regulation.

Introduction

Silicon Valley Bank (SVB), an iconic institution serving the US technology sector and the United States’ sixteenth-largest bank by assets, collapsed in a crisis that unfolded with shocking speed between March 8 and 10, 2023 (Chappatta 2023). The collapse sent shock waves through the US and global financial systems.

The context was anything but benign: on March 7, the day before the SVB crisis flared, Jerome Powell, the chair of the US Federal Reserve, in testimony before the Senate Banking Committee, commented that interest-rate increases could be larger and more rapid than previously anticipated. Specifically, Powell stated that “the ultimate level of interest rates is likely to be higher than previously anticipated” and that, if necessary, the Fed “would be prepared to increase the pace of rate hikes” (Schneider and Dunsmuir 2023).

With the US yield curve inverted since mid-2022,

- New York-based Signature Bank, the twenty-ninth-largest bank in the United States, failed two days after SVB (Giang 2023). The Federal Deposit Insurance Corporation (FDIC) seized the bank and sold it to Flagstar Bank, N.A., a subsidiary of New York Community Bancorp, with the latter bank assuming the business of Signature Bank as of March 20, 2023 (FDIC 2023a).

- San Francisco-based First Republic Bank, the fourteenth-largest bank in the United States, received a US$30 billion bank-led liquidity injection to shore up confidence after US$70 billion in emergency loans and other liquidity from the Federal Reserve and JPMorgan Chase had failed to stabilize it (Copeland et al. 2023). Even with this support, First Republic was unable to continue, and was seized by authorities on May 1, with its assets sold off to JP Morgan, which assumed First Republic’s deposit liabilities (FDIC 2023b).

- Zürich-based Credit Suisse’s share price collapsed, forcing a massive emergency injection of funds by the Swiss bank supervisory authorities (Cooban 2023) and subsequently a takeover by UBS (Patrick et al. 2023).

- SVB itself was sold, following a two-week auction process, to North Carolina-based First Citizens Bank, ending its history (Choe 2023). The FDIC estimated the cost of the SVB resolution to its Deposit Insurance Fund at approximately US$20 billion (FDIC 2023c).

The run was in part due to the initial approach by the US authorities to the SVB failure, which was to establish a Deposit Insurance National Bank under FDIC control to provide insured depositors immediate access to their insured funds and to pay out a portion of the funds owed to uninsured depositors through an Advance Dividend, while holding back a portion to help cover any losses to the Deposit Insurance Fund. The prospect of losses triggered a run on uninsured deposits in other banks, including Signature and First Republic.

The authorities (including the FDIC, the Federal Reserve and the Secretary of the Treasury) reacted by invoking the systemic risk exception under the Federal Deposit Insurance Act, which set aside the least-cost requirement to the Deposit Insurance Fund to protect the uninsured depositors in SVB and Signature (Gruenberg 2023).

As well, President Joe Biden sought to reassure markets and depositors to prevent further bank runs, saying “Your deposits will be there when you need them” (Sweet et al. 2023). And analysts emphasized that SVB and First Republic had been outliers in terms of business strategies – in particular, in terms of having asset-liability mismatches – that exposed them unduly to the risks posed by rising interest rates (see, for example, Defend, Mortier, and Germano 2023; Russell and Zhang 2023).

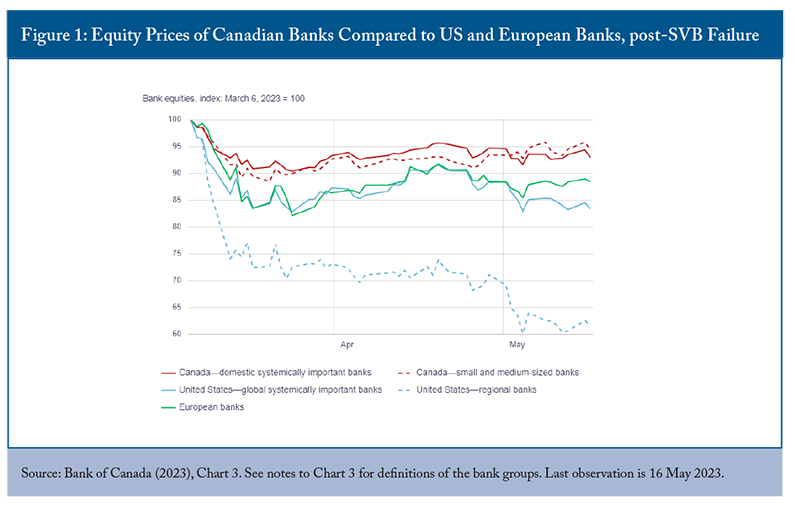

While markets generally discounted the risk of further knock-on events, nonetheless several mid-sized US banks that were judged not to be “too big to fail” – in particular, Los Angeles–based PacWest and Phoenix-based Western Alliance (Hirsch 2023a). Pacific Western was merged out of existence in July 2023 as it could not recover (Nishant and Saini 2023). The share price of Western Alliance did rebound but remains as of this writing well below its pre-SVB moment valuations, which suggests that markets have yet to issue an “all clear” signal.

In tallying up the damage, the assets of the three failed US banks totalled US$548 billion (FDIC 2023d), which is larger in absolute terms than the US$526 billion (inflation adjusted) held by the 25 US banks that collapsed in 2008 at the height of the subprime crisis (Russell and Zhang 2023) and of the same order of magnitude (2.4 percent versus 3.4 percent in the subprime crisis) when the two figures are compared as a share of total banking assets.

The Immediate Impact on Canada

The immediate ramifications on Canada, however, were minor. Canada’s banking regulator, the Office of the Superintendent of Financial Institutions (OSFI), took control of SVB’s Canadian branch, which had started operations in Canada only in 2019 (OSFI 2023b; Punchard 2023) and resumed a practice adopted during the COVID-19 pandemic of a daily check on bank liquidity levels.

As SVB’s Canadian branch was only authorized to lend and not take deposits in Canada, there were no ramifications in terms of depositor risk. Some Canadian technology companies that had established relationships with Silicon Valley did have deposit accounts in SVB, which then became part of the US resolution of the failure.

Canadian analysts hastened to emphasize the limited risk of instability to the Canadian banking sector (see Johnson 2023). Commentaries noted the small direct exposure of Canadian banks to the technology sector and that the main exposure of Canadian banks to US developments was indirect through their US bank subsidiaries.

• TD: 35% of TD’s earnings come from US retail banking (TD 2022), including from TD Bank, America’s Most Convenient Bank, which is the tenth largest US bank, and through its holdings in the Charles Schwab Corporation. See: https://www.td.com/about-tdbfg/corporate-information/corporate-profile/….

• RBC: 25% of RBC’s global revenue comes from the United States. RBC claims to be the leading Canadian investment bank in the United States and the 6th largest wealth manager in the United States (RBC 2023). It also holds LA-based City National, the 35th largest bank in the United States, which focuses on Hollywood.

• CIBC: 11.3% of its global revenue comes from its US operations (CIBC 2022).

And not for the first time, the “Canadian model” for banking was touted: “Not only should the failure of Silicon Valley Bank not have significant negative implications for our banks, but this crisis should actually be viewed as further vindication of the Canadian banking model” (Scotiabank analyst Meny Grauman, quoted in Bickis 2023).

The SVB collapse has been compared to the Bear Stearns moment as the subprime crisis started to unfold (Pollard et al. 2023). This raises the question of whether the system remains exposed to a Lehman moment parallel. Markets generally appear to have drawn a line under the SVB moment but there are reasons to consider the lessons from this incident.

First, while the US policy response to SVB nipped the incipient crisis in the bud, the US banking system remains fragile on a structural basis. As Jiang et al. (2023) note, “prior to the recent asset declines all US banks had positive bank capitalization. However, after the recent decrease in value of bank assets, 2,315 banks accounting for [US]$11 trillion of aggregate assets have negative capitalization relative to the face value of all their non-equity liabilities.” The Federal Reserve Board’s October 2023 Financial Stability Report confirms that “high interest rates continued to depress the fair value of longer-maturity, fixed-rate assets that, for some banks, were sizable.” As well, it notes that “a subset of banks continued to face funding pressures, reflecting concerns over uninsured deposits and other factors” (FRB 2023).

Second, the shadow banking sector, which engages in credit intermediation outside the framework of rules developed to govern banks in this activity, has grown its direct lending very substantially.

Third, while the tech sector exposure has been flagged as a reason to treat SVB as an isolated case, the larger risk for the financial system is rapid technological change driving pervasive structural change in the economy. For example, commercial real estate debt is a source of risk as increased work-from-home drives both reduced demand for office space and the products of the services sector that evolved to serve office workers. Also, it is unknowable what stresses the widespread adoption of artificial intelligence systems will unleash – but stresses there will be.

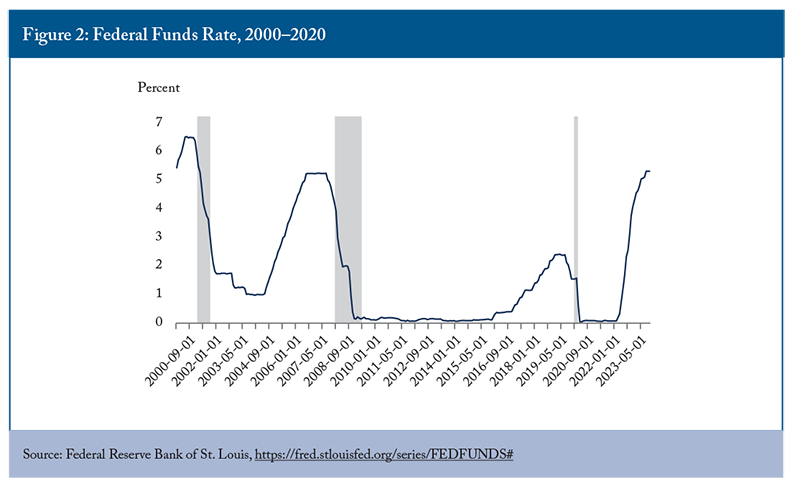

These structural issues loom large, since further monetary tightening has not been taken off the table as of this writing. Following the Federal Open Market Committee (FOMC) meeting of early November 2023, Fed chair Jerome Powell stated: “We haven’t made any decisions about future meetings…It’s fair to say that the question we’re asking is: Should we hike more?” (cited in Foster 2023). Perhaps even more important, the Fed has indicated that rates will remain high for longer. As can be seen from Figure 2, the subprime crisis did not break out immediately following the monetary tightening of 2006, but rather after an extended period of high interest rates, a situation that now looms for the US economy (note: the grey bars denote recessions).

Accordingly, even though the US money centre banks, which have been the focus of supervisory attention since the subprime crisis, are reportedly well capitalized, it is an open question of whether US authorities are in a position to revert to business as usual on bank closures without tipping the system into yet another crisis.

This is significant because while the SVB crisis has led to consideration of regulatory reforms in the United States,

In this Commentary, I consider what light can be shed on the policy course being taken in the United States from the historical evolution of the Canadian and US financial sectors in terms of financial stability. Where Canada has implicitly prioritized avoiding systemic risk in handling troubled financial institutions and has a remarkable history of stability, the United States has implicitly prioritized moral hazard and has an unparalleled history of financial crises.

The Commentary is organized as follows. The next section provides an overview of this history, documenting the differences in societal costs of the two approaches; the online Appendix reviews this history in greater detail. The following section discusses the many contending explanations for the divergence in historical outcomes. It identifies the tipping point in history where Canadian and US experience diverged given the choice made in Canada early in its history to prioritize prevention of the negative externalities associated with bank failures, while the United States tolerated failures to provide a market discipline on moral hazard. The next-to-last section discusses the implications of these choices for financial sector efficiency and stability and the extent to which there is a trade-off between the two objectives based on tolerance for risk taking. The final section concludes with a discussion of the lessons Canadian policymakers should draw from the SVB failure – and what lessons US policymakers might draw from the Canadian experience.

The Great Divergence

Canada and the United States are highly similar economies, as would be expected given the many common historical influences on economic policy and regulation, similar levels of income and urbanization, the shared geography (each Canadian region is part of a larger North American region with its US neighbour) and the high degree of economic interaction, amplified by more or less free trade since the 1989 Canada-US Free Trade Agreement. Importantly for the present discussion, the agreement removed US banks from the cap on foreign bank assets in Canada, opening up competitive pressure in Canada’s financial markets. The Bank Act reforms that authorized foreign branch banking in Canada further opened up the system to competition on the asset side, although not so much on the funding side.

Deep integration creates incentives for regulatory convergence, which in the North American context essentially means that Canadian standards and regulations tend to follow the rules adopted by the United States, even if they differ in their minutiae (Hart and Dymond 2007).

In the financial sector, however, and particularly in banking, the US model has not been the primary influence on Canada: where the United States has been crisis prone, Canada has a long history of stability. In fact, the two countries arguably occupy the polar extremes of the most and least crisis-prone financial sectors of the major economies.

The Anomalous History of US Financial Crises

The United States is a far outlier in terms of frequency of bank failures and financial crises. In its early history, the United States had recurring financial crises/panics/incipient panics on a decadal-plus basis, resulting in 3,401 banks suspending payments between 1865 and 1914 alone (Davis and Gallman 2001). The Federal Reserve Board was established in 1913 in response to the 1907 panic.

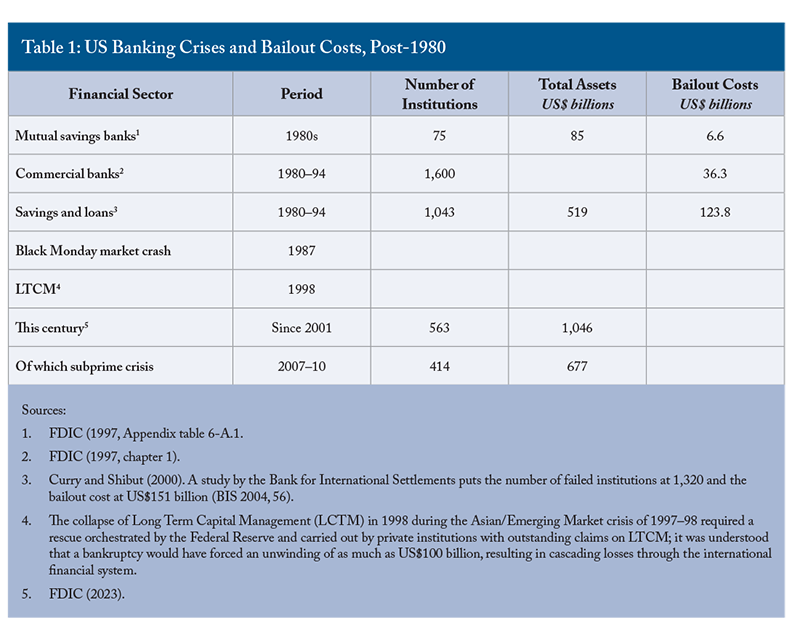

The interwar period featured additional waves of bank failures, including over 9,000 failures during the 1930–33 period alone (Calomiris and Mason 2003). During the Bretton Woods era, the United States had a brief respite from financial crises, but these returned with a vengeance in the 1980s. A partial tabulation of the post-1980 crises and the bailout costs they entailed (prior to the SVB event) is provided in Table 1.

The Sharp Contrast between Canada’s History and US Experience

The contrast between the US experience and that of Canada could not be greater, despite the fact that Canada experienced the same major shocks as did the United States. Since 1900, Canada has had only one significant bank failure (Home Bank in 1923).

Canada, however, had its version of the savings and loan crisis in the early 1980s. In the United States, this crisis was centred in the oil patch, with Texas the epicentre. In Canada, it was centred in Alberta. Canada closed two small banks (Canadian Commercial and Northland) and merged another troubled bank (Bank of British Columbia) out of existence, with financial support from the public purse. No depositor lost a cent and there was no crisis – although, as the Estey Commission underscored, it was the collapse of the Canadian Commercial Bank that undermined the Northland Bank’s “survival tactics” in raising capital (Estey 1986, 6). The cost to the Canadian government amounted to $1.39 billion, of which $875 million was payouts to uninsured depositors, $316 million was losses incurred by the Canada Deposit Insurance Corporation (CDIC), and $200 million injected by the federal government to facilitate the takeover of the Bank of British Columbia by Hongkong Bank of Canada (Chant et al. 2003). It is worth noting that this was the only instance in the history of Canada’s deposit insurance program where the banking system proper required assistance.

Canada also had an echo in its non-bank deposit-taking sector of the extended period of banking sector troubles in the United States from the early 1980s through the mid-1990s. Canada lost 38 trust and loan or mortgage companies insured by the CDIC during this period, including six in 1983. The last deposit-taking institution to fail in Canada was Security Home Mortgage Corporation, in 1996 (although there have been some close calls since). The total amount in deposit repayments or rehabilitation laid down by the CDIC amounted to $10.2 billion, with total losses of about $1.7 billion.

Canada emerged from the Great Financial Crisis of 2007–08 without the failure of a financial institution. To be sure, the Canadian banking system required liquidity support (including from the Federal Reserve) during the crisis due to the closing of global funding markets, but Canadian banks did not need any capital injections from public authorities.

That record has been maintained since, including through the SVB crisis, notwithstanding some close calls along the way.

Duelling Explanations

Canada and the United States provide a “natural experiment” for studying the impact of alternative financial sector regulatory and supervisory polices (see Bordo, Rockoff, and Redish 1994). Canadian officials have promoted the “Canadian model” – for example, through Canada’s Global Risk Institute in Financial Services) – researchers have tried to tease out just what about that model accounted for its apparent relative success and some countries (such as Ireland) have set out to imitate it. Nonetheless, the reason for the difference in outcomes is tantalizingly difficult to pin down.

Different Crises, Different Explanations

A first major challenge in identifying the source of Canada’s relative stability is that, for each US crisis, differing aspects of the “Canadian model” have been singled out as the key explanatory factor.

For example, it is generally argued that, in the Great Depression, Canada’s regionally diversified national banking system enabled it to avoid the waves of bank failures experienced in the US unit-bank-dominated system. As many analysts have pointed out, however, regional diversification breaks down as a risk-management measure when all regions of a country are subject to a common shock, as was the case in the Great Depression. Moreover, by the time of the subprime crisis, US banks had become regionally diversified, and the largest bank to fail in US history to that point – Washington Mutual – had as impressive a branch network as any of the major Canadian national banks.

When the United States had its savings and loan crisis, Canada largely avoided the problems because of a timely liberalization of interest rates in the late 1960s, prior to the inflationary surge of the 1970s, thus avoiding the disintermediation suffered by the US savings and loans institutions that was a major contributing factor to the crisis in the United States.

When the United States again lurched into crisis as a result of the subprime mortgage debacle, Canada’s system emerged largely unscathed despite many similar contextual developments. Some of the differences noted to explain the difference in outcomes in this latter incident include:

- statistically significant differences in particular balance-sheet ratios – for example, capital and liquidity ratios or the share of liabilities generated by retail versus wholesale deposits, as Rostnovski and Huang (2009) emphasize;

- the concentrated Canadian banking system (Bordo, Redish, and Rockoff 2011);

- differences relevant to the mortgage market, including the lesser run-up in housing prices in Canada, the fact that mortgage interest is not tax deductible in Canada, which works to constrain speculation, and the fact that Canadian mortgage loans are not non-recourse loans as is the case in many US states, (features emphasized by Dodge 2011);

- the consolidation of supervision of Canada’s federally supervised financial institutions under the Office of the Superintendent of Financial Institutions, which contrasted with the fragmented US regulatory framework;

Formal reviews of the functioning of Canada’s prudential regulatory and supervisory system also emphasize the effectiveness of interagency cooperation in Canada between OSFI, the Bank of Canada, the CDIC and the federal Department of Finance through formally established bodies such as the Senior Advisory Committee, which considers systemic issues, including crisis preparedness, and the Financial Institution Supervisory Committee, which addresses institution-specific problems, including early intervention into troubled financial institutions. More generally, Canada gets good marks for the collegial culture of information exchange and cooperation among the agencies with a formal role in financial system governance. See IMF (2019) for a detailed discussion of these issues and the division of responsibilities among Canada’s federal agencies for dealing with systemic-risk issues, including the overarching responsibility of the minister of finance for financial system stability, and the Bank of Canada’s responsibilities as lender of last resort and manager of the payments system. and - Canada’s innate conservatism in running the financial sector and stronger prudential requirements – for example, capital requirements over and above the Basel Accord requirements and limits on the role of innovative forms of capital in Tier 1 capital, points emphasized by Jackson (2013) in a Congressional Research Service report.

For example, in their exegesis of the subprime crisis, Bordo, Redish, and Rockoff (2011) attribute Canada’s escape from crisis to the fact that the concentrated Canadian banking system had absorbed the key sources of systemic risk that exploded in this crisis – namely, the mortgage market and investment banking – and was tightly regulated by one overarching regulator. By contrast, in the United States, a weaker fragmented banking sector had resulted in the evolution of a strong financial market that featured a large shadow banking system, multiple competing regulatory authorities, and a “labyrinthine set of regulations for financial institutions.” In the US system, the shadow banks were largely outside the regulatory umbrella and the risks that they took were therefore not well understood or monitored. While Canada had its version of the shadow banking crisis in the form of the meltdown of the non-bank asset-backed commercial paper (ABCP) market, this activity was relatively small in Canada compared to the United States (see, for example, Chant et al. 2003).

To be sure, the Canadian financial sector reforms in the early 1990s – which replaced the “four pillars” framework based on the separation of banking, trust, investment underwriting and insurance with an integrated financial sector model under one supervisory institution – explicitly targeted many of the risks that blew up in the United States in the subprime crisis.

Moreover, the risk-management rules both Canada and the United States adopted are broadly consistent with the global standards that have emerged through decades of work through international organizations such as the Bank for International Settlements (BIS) and the International Organization of Securities Commissions (IOSCO). Regulatory convergence has also gained impetus from international competitiveness concerns.

Paralleling the official processes, individual financial institutions have developed mathematically sophisticated techniques to manage risk, mining the massive databanks that have been developed on financial markets and instruments. Although individual institutions in Canada and the United States might have superior systems, it is hard to see why Canadian banks as a whole should consistently have more effective internal controls than do US banks.

To illustrate the difficulty of untangling this particular web, both Canada and the United States adopted a major financial sector reform prior to the subprime crisis, allowing banks into investment underwriting. In Canada, this was done through the “mini big bang” of 1987. In the United States, the reform was the repeal of the Glass-Steagall Act in 1999, a move that has been blamed explicitly for contributing to the subprime crisis. In Canada, the mini big bang was motivated by the desire to protect the banking system from disintermediation by a nascent shadow banking system – as signalled by the institution of the “bought deal” by Gordon Capital in the mid-1980s. Such a system would have created a dynamic problem of adverse selection as the banks’ best clients moved into direct financing, given that, at the time, they had as good or better credit ratings than the banks, which were saddled with non-performing sovereign loans associated with the Latin debt crisis. In one country, deregulation is said to have led to the crisis; in the other, the same deregulation can be argued to have prevented the crisis.

The Simultaneous Failure of Multiple Lines of Defence

The second major challenge in trying to nail down specific regulatory or supervisory features as responsible for Canada’s record of stability lies in the fact that, in managing their affairs, financial institutions have multiple lines of defence against failure: internal risk-monitoring management systems, internal auditors, boards of directors’ audit committees, boards of directors themselves, external auditors, and the disciplines generated by scrutiny from interested shareholders, market analysts and credit-rating agencies. Supervisory oversight and regulatory rules of the road are thus only one line of defence, and not necessarily the most important.

Given the various lines of defence, following every major financial debacle, of which we now have had four and counting in the span of a quarter-century – the Asian crisis, dot-com, subprime and now SVB – recriminations are levelled at each layer: the managers (and their pay/incentive packages), the directors, the auditors, the rating agencies, the market analysts, the risk models and the technicians who build them and, of course, public sector rules and the supervisory authorities.

For example, examining the subprime crisis, the Financial Crisis Inquiry Commission (FCIC 2011) seemingly apportioned equal blame to the “captains of finance and the public stewards of our financial system” who “failed to question, understand, and manage evolving risks” in the financial system, while commenting disapprovingly on households that “borrowed to the hilt.” The Commission listed its major findings as follows:

- The financial crisis was avoidable: it was the result of “human action and inaction, not of Mother Nature or computer models gone haywire” (FCIC 2011, xvii).

- There were failures in financial regulation and supervision: “The sentries were not at their posts, in no small part due to the widely accepted faith in the self-correcting nature of the markets” (FCIC 2011, xviii).

- There were “dramatic failures of corporate governance and risk management at many systemically important financial institutions” (FCIC 2011, xviii).

- There was “excessive borrowing, risky investments, and lack of transparency” (FCIC 2011, xix).

- The government was “ill prepared for the crisis, and its inconsistent response [allowing some institutions to fail but bailing out others] added to the uncertainty and panic in the financial markets” (FCIC 2011, xxi).

- There was a “systemic breakdown in accountability and ethics” (FCIC 2011, xxii).

More generally, the Commission blamed the collective “we” for allowing the development of a shadow banking system that lacked all the safeguards built around the formal banking system to prevent recurrence of the crises of the 1930s; in Biblical tones, the Commission concluded, “We had reaped what we had sown” (FCIC 2011, xx).

In the case of the subprime crisis, the chain of failure was multiplied many times over because of the multiple players involved in the generation of the derivative instruments at the heart of the crisis. As Baily, Litan, and Johnson (2009, 8) observe,

What is especially shocking...is how institutions along each link of the securitization chain failed so grossly to perform adequate risk assessment on the mortgage-related assets they held and traded. From the mortgage originator, to the loan servicer, to the mortgage-backed security issuer, to the CDO issuer, to the CDS protection seller, to the credit rating agencies, and to the holders of all those securities, at no point did any institution stop the party or question the little-understood computer risk models, or the blatantly unsustainable deterioration of the loan terms of the underlying mortgages.

The Asian crisis elicited a similar litany of recriminations of failure at every step in the line of defence: Where were the auditors? Where were the credit-rating agencies? Where were the risk models?

These recriminations are being reiterated at present in the SVB crisis (Barr 2023). For example, in the review of the SVB failure, it was noted that supervisory officials had warned SVB about the risk that higher interest rates posed to its balance sheet as far back as November 2021; SVB failed to address the concerns, however, exposing it to the deposit run that took it down (Son 2023) and exposing the supervisors for not having acted on their own warning.

That should give pause for reflection.

A theme that has received prominent discussion as a causal factor in financial crises is fraud. In the case of the subprime crisis, it was noted that none of the executives of the major failures went to jail: “Too big to fail, too powerful to jail?” is a question raised by Pontell, Black, and Geis (2014) in assessing why there were no major prosecutions – although hundreds of lower-level participants in the mortgage origination process were prosecuted (Nguyen and Pontell 2010). In a retrospective, Griffin (2021) identifies from a survey of the literature what he terms “a cohesive narrative that conflicts of interest and the malfeasant features it generated played a central role in the financial crisis.” Nguyen and Pontell (2010) describe the fraud as “built into” the financial system – that is, the system is structurally fraudulent in that “lax lending policies, poor underwriting standards, inadequate regulatory structure, and government oversight…entails significant amounts of fraud at various institutional levels.”

From the perspective of the present author, there are three major problems with assigning fraud a key role in the subprime or other financial crisis. First, fraud is a routine part of economic activity and is subject to routine monitoring and prosecution. For example, the US Mortgage Bankers Association estimated that, in 2006, mortgage fraud cost the industry between US$946 million and US$4.2 billion (cited in Nguyen and Pontell 2010). For its part, the FDIC issues a regular “Mortgage Loan Fraud Industry Assessment Based on Suspicious Activity Report Analysis.” The January 2017 report highlighted that the frequency of suspected frauds had risen substantially in the previous year (FDIC 2007).

The real issue, however, is not individual misrepresentations on mortgage applications by applicants who intend to repay, but “fraud for profit” – the latter is systematic (FBI 2007). That leads to the second point, which is that an allegation of fraud as a critical factor means “fraud for profit,” which then indicts the entire system – the “built-in” argument noted above. Fraud then becomes all-encompassing, and its role in “causing” the subprime crisis and, by extension, the longer history of US banking sector crises becomes inherently an “American-exceptionalism” argument – which is uncomfortable to rely on.

Finally, this fails to explain the failure of the entire system of controls all at once but only episodically. In short, fraud will always be found, will always be a contributing factor to the scale of the losses, but fails as a critical explanatory factor and, a fortiori, as a predictive factor.

Where the “fraud” explanation implicitly argues that the system was fine but there were bad apples in the barrel, a diametrically opposite explanation is to argue that the players were fine but risk models could not keep up with financial innovation.

Securitization is hardly new: it dates back to the 1800s, and the modern era, driven by securitization of mortgages, dates back to at least the 1970s (Kaplan 2014), if not the 1920s (Goetzmann and Newman 2010). The evolution of the overall financial system in terms of the relationships among the various types of intermediaries, their relative scale and so on would, of course, modify the system’s behaviour. For example, Gorton and Metrick (2010) point to the role of repurchase agreements in maturity transformation as the real culprit – although they acknowledge that all explanations remain controversial. In the big picture of long history, specific innovations become a digression in a footnote.

Canada Has the Bugs but Not the Disease

In light of the above, it is interesting, from the perspective of a comparative US-Canada analysis, to review the list of causal factors the CDIC lists in its own analysis of failures of Canadian financial institutions (CDIC 1997):

Mismanagement:

• lack of business plans and coherent strategies.

• excessive risk taking in expanding market segments.

Control system

• inadequate control systems to ensure compliance with internal policies and supervisory rules.

• inadequate credit analysis and loan review procedures.

Poor asset quality

• excessive concentration in a single sector.

• excessive loan growth in relation to management, control systems and funding sources.

• overlending (high loan-to-debt serviceability ratio).

Poor liquidity

• lack of cash to ensure the continuation of operations, caused by mismatch of loans and short-term assets and liabilities.

Capital adequacy

• inadequate capital to meet all applicable regulatory requirements and/or operating losses.

Fraud and concealment

• material fraud, which generally includes the intent to deceive and/or an attempt to conceal insider abuse in self-dealing.

Parent (or group contagion)

• difficulties caused by problems elsewhere in the group.

This list would not be out of place in any analysis of the US system. And yet, Canada’s system is stable and the US system is not. The bugs that are blamed for the disease of instability are present in Canada, but the disease is not. And this too gives pause for reflection.

The Tipping Point: Where Canada and the US Diverged

If we look to history for the answer, we need to focus on developments in Canada when its experience started to diverge. This was 1900. Prior to that date, Canada’s financial institutions failed as routinely as those in the United States. After that date, they did not. In 1900, Canada had a decennial revision of its Bank Act. For reasons that are probably completely buried in the sands of time, Canadian policymakers gave a prime role in resolving bank problems to the Canadian Bankers Association.

Here it is salient to note that the first Canadian banks were founded by Scots, and there are many parallels between Canadian banking history and Scottish banking history. Scotland had a history of banking stability that contrasted sharply with the tendency of the English banking system to lurch into crises. In their magnum opus to explain banking sector fragility as a “game of bank bargains,” Calomiris and Haber (2014) go into great depth in describing England’s troubled history but spend little time on Scotland, despite noting the distinctly different history. Nor do they unpack Canada’s similar divergence from its southern neighbour’s experience, despite Canada’s shared banking tradition with Scotland.

But there is a hook here on which to hang a theory. The implicit “model” that explains the sharp improvement in Canadian banking sector stability comes originally from the role of the Canadian Bankers Association. Bankers are strongly averse to instability because of the negative spillovers of such failures on their own banks and on the value of their bank charters. Any need for reinforcement of this perspective was provided by the fallout from the Home Bank failure in 1923. And thereafter, Canada handled incipient bank problems through mergers and acquisitions, not through allowing failures (see the Appendix for examples of how Canadian banks resolved incipient problems). The Canadian bankers controlled moral hazard through what we would refer to today as “social networks.” The United States, by contrast, prioritized the role of market disciplines in controlling moral hazard.

This, along with the historical accident of decennial revisions that prompted regular reform between crises rather than driven by crises, allowed the Canadian system to address the externalities generated by bank failures directly rather than indirectly through market discipline, while adapting to changing societal needs and technological conditions on a timely basis. Importantly, the system ensured enough competition to be efficient, as concluded by studies explicitly focused on this point conducted over many years (see the online Appendix for an elaboration and citations).

Following the SVB failure, Canada finds itself in a familiar position of observing a simmering financial crisis in the United States driven by a factor common to both countries – in this case rising interest rates due to monetary tightening – and facing similar factors in the risk environment, including commercial real estate and the increased potential rapidity of bank runs due to the digital transformation. Again, the United States is driven to consider a range of reforms in the wake of a crisis, while Canada is not.

Discussion and Conclusions

There are several takeaway points from the consideration of the comparative history of Canadian and US financial sector stability.

First, the US response in the SVB crisis balanced concerns about stability with concerns about longer-term efficiency from a possible heightening of moral hazard risk. In this regard, the US approach to SVB was much more in line with Canadian historical practice and does not necessarily create the risk of future crisis since, as Canada has demonstrated, moral hazard risks can be addressed between crises. The most comparable episode to SVB in US financial history is the Latin debt crisis, when the US authorities, alongside their international counterparts in this instance, exercised regulatory forbearance and avoided a US banking crisis on that account. That is encouraging for the prospects of avoiding a banking crisis in the present moment given the continuing vulnerabilities in the US banking system and the unknown risks in the shadow banking system.

Second, while US authorities are subject to the political necessity to be seen to be taking action, Canadian authorities are not. Nonetheless, OSFI was quick off the mark to monitor liquidity in the Canadian banking system, given that the SVB failure was triggered by a liquidity crisis, and the Canadian Bankers Association, although no longer armed with the powers conferred on it by the 1900 Bank Act, was similarly quick to issue a statement asserting the stability of the Canadian banking system. Forewarned is forearmed.

Third, while history tells us there is no parallel between the United States and Canada in terms of banking crises, the same history shows that Canada’s stability advantage was not quite as clean as it might appear. In this regard, see for example: the shrinkage of Canada’s bank branches in the Great Depression, which roughly matched the number of US bank failures; the litany of trust and loan company resolutions paralleling the US S&L and banking crises of the 1980s-1990s; and the collapse of Canada’s ABCP market during the subprime crisis in parallel with the collapse of similar instruments in the United States. Moreover, Canada's comparative stability also arguably owes something of a debt to serendipity – for example, the timely deregulation of interest rates for reasons unrelated to the benefit that Canada enjoyed as a result when accelerating inflation massively escalated the US savings and loan crisis. Accordingly, there is no basis for complacency. The present paper does not make the case for Canada to pat itself on the back. The SVB moment is, after all, the first such crisis in the age of social media, online banking and an unprecedented disruption that is unfolding in terms of the way we work flowing from the changes wrought by the pandemic and that are to come in the age of artificial intelligence.

Finally, while the evidence strongly argues that Canada did not buy stability through a grand trade-off with efficiency, since the US propensity for crisis has little to do with economic efficiency gains from optimizing competition in financial markets, this is not to argue that there is no trade-off at all between these objectives. Working within a regulatory/supervisory model that gives appropriate weight to the many and often destabilizing negative externalities of allowing financial institutions to fail and that acknowledges the de facto impossibility for depositors to judge the soundness of a bank from the quality of the marble in its foyers or the implications of the footnotes in its annual reports, it is possible to craft a financial sector policy that nudges the system toward greater efficiency while courting some additional margin of risk.

For example, the major Canadian banks reported Common Equity Tier 1 (CET1) ratios well above the regulatory minimum in 2022 (Rush 2023). From the perspective of the banks, this might reflect the need to maintain buffers above regulatory minima for risks not captured by the formal regulatory framework, including, for example, various uncertainties facing the economy, such as the historically high ratio of debt to income in Canada. From the perspective of the economy, however, it might reflect excessive prudence, as reflected in the fact that the margin between the prime business lending rate and the rate to small and medium-sized enterprises has tended to be the highest in the OECD (Kronick and Bafale 2022). In light of the narrative in this Commentary, one would be hard pressed to attribute the gap reported by Kronick and Bafale (2022) between the average spread for Canada (2.26 percentage points) and the United States (0.26 of a percentage point) to the treatment of moral hazard concerns in dealing with troubled institutions.

An informed reading of our own history – including reflecting on the Porter Commission’s advocacy for bank entry into conventional mortgage lending despite the mismatch in terms of assets and liabilities that this entailed – suggests that Canada has the margin to push for greater efficiency in its financial institutions policy. And, as also informed by its own history, this margin might be credited to the fact that, a century ago, in response to the last major bank failure in Canada, the collapse of Home Bank in 1923, Canada took the right decision about how to deal with the negative externalities of bank failures. The rest is history.

Canada has avoided its own banking crises over the past century, but it has not escaped the macroeconomic consequences of US banking crises. Nor would Canada escape the macroeconomic consequences of any knock-on financial trigger in the wake of the SVB failure, whether in the formal banking system or in the shadow banking system. The main takeaway lesson from Canada’s experience, when compared to that of the United States, is that there is no grand trade-off between economic dynamism and efficiency and instability. Instability is a choice made by prioritizing moral-hazard concerns over the negative externalities that come from bank failures. Moral-hazard issues are addressed far more effectively through regulatory design formulated in quiet periods rather than in the heat of a crisis. Economic efficiency can be pursued by fine-tuning the scope for risk taking through competition and regulatory design.

References

Allen, Jason, and Walter Engert. 2007. “Efficiency and Competition in Canadian Banking.” Bank of Canada Review, Summer, 33–45.

Allen, Jason, Walter Engert, and Ying Liu. 2007. “Are Canadian Banks Efficient? A Canada-U.S. Comparison.” Financial System Review. Ottawa: Bank of Canada.

Ames, Daniel, Chris S. Hines, and Jomo Sankara. 2014. “Credit Union Failures: Why Liquidate Instead of Merge?” Academy of Business Disciplines Journal 6 (1): 32–63.

Andrews, Edmund L. 2008. “Greenspan concedes error on regulation.” New York Times, October 23. https://www.nytimes.com/2008/10/24/business/economy/24panel.html.

Baillie, Charles. 1998. “Remarks to the House of Commons Standing Committee on Finance,” cited in The Standing Committee On Finance, Twelfth Report, https://www.ourcommons.ca/documentviewer/en/36-1/FINA/report-12/page-24

Baily, Martin Neil, Robert E. Litan, and Matthew S. Johnson. 2008. “The Origins of the Financial Crisis.” Washington, DC: Brookings Institution, Initiative on Business and Public Policy.

Bank of Canada. 2023. “Financial System Review 2023 – In Brief.” https://www.bankofcanada.ca/2023/05/financial-system-review-2023/.

Barr, Michael S. 2023. “Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank.” Board of Governors of the Federal Reserve System, April 28. https://www.federalreserve.gov/publications/files/svb-review-20230428.pdf.

Bean, Mary Ledwin, Martha Duncan-Hodge, William R. Ostermiller, Mike Spaid, and R. Steve Stockton. 1998. Managing the Crisis: The FDIC and RTC Experience, Washington, DC: Federal Deposit Insurance Corporation. https://www.fdic.gov/bank/historical/managing/v.

Bernanke, Ben S. 2012. “Some Reflections on the Crisis and the Policy Response.” Remarks at the Conference on “Rethinking Finance: Perspectives on the Crisis.” Russell Sage Foundation and the Century Foundation, New York, April 13.

Bernanke, Ben, Mark Gertler and Simon Gilchrist. 1996. “The Financial Accelerator and the Flight to Quality,” The Review of Economics and Statistics 78(1), February: 1-15.

Bickis, Ian. 2023. “Silicon Valley Bank collapse presents low risk for Canadian sector: analysts.” Canadian Press, March 13. https://www.ctvnews.ca/business/silicon-valley-bank-collapse-presents-low-risk-for-canadian-sector-analysts-1.6311098.

BIS (Bank for International Settlements). 2004. “Bank Failures in Mature Economies.” Working Paper 13, Basel: BIS.

Boone, Peter, and Simon Johnson. 2010. “Canadian Banking Is Not the Answer,” The New York Times, 25 March. https://archive.nytimes.com/economix.blogs.nytimes.com/2010/03/25/canadian-banking-is-not-the-answer/

Bourque, Michelle. 2014. “CDIC’s New Role as Canada’s Resolution Authority,” Speaking Notes for CDIC President and CEO, Michele Bourque, CD Howe Institute, 9 June. https://www.cdic.ca/wp-content/uploads/Speech_MBourque_CDHowe_jun2014.pdf

Bordo, Michael D. 1986. “Financial Crises, Banking Crises, Stock Market Crashes and the Money Supply: Some International Evidence, 1870–1933. In Financial Crises and World Banking System, ed. Forrest Capie and Geoffrey E. Wood, 190–248. New York: St. Martin’s Press.

———. 1990. “The Lender of Last Resort: Alternative Views and Historical Experience.” Federal Reserve Bank of Richmond Economic Review, January/February, 18–29.

———. 1995. “Regulation and Bank Stability: Canada and the United States, 1870–1980.” Policy Research Paper 1532. Washington, DC: World Bank.

Bordo, Michael D., Hugh Rockoff, and Angela Redish. 1994, “The U.S. Banking System from a Northern Exposure: Stability versus Efficiency.” Journal of Economic History 54 (2): 325–41.

Bordo, Michael D., and David C. Wheelock. 1998. “Price Stability and Financial Stability: The Historical Record.” Federal Reserve Bank of St. Louis Review, September/October, 41–62.

Borio, Claudio. 2003. “Towards a Macroprudential Framework for Financial Supervision and Regulation?” BIS Working Paper 128. Basel: Bank for International Settlements.

Brandenburger, Adam M., and Barry J. Nalebuff. 1996. Co-opetition: A Revolution Mindset that Combines Competition and Cooperation. Crown Business.

Calomiris, Charles W. 2007. “Bank Failures in Theory and History: The Great Depression and Other ‘Contagious’ Events,” NBER Working Paper No. 13597, November. https://www.nber.org/system/files/working_papers/w13597/w13597.pdf

Calomiris, Charles W., and Gary Gorton. 1991. “The Origins of Banking Panics: Models, Facts, and Bank Regulation,” Chapter 4 in R. Glenn Hubbard (ed.) Financial Markets and Financial Crises, University of Chicago Press: 109-174.

Calomiris, Charles W., and Stephen H. Haber. 2014. Fragile by Design: The Political Origins of Banking Crises & Scarce Credit. Princeton, NJ: Princeton University Press.

Calomiris, Charles W., and Joseph R. Mason. 2003. “Fundamentals, Panics, and Bank Distress during the Depression.” American Economic Review 93 (5): 1615–47.

Canada. 2006. “2006 Financial Institutions Legislation Review: Proposals for an Effective and Efficient Financial Services Framework.” Ottawa: Finance Canada. https://publications.gc.ca/collections/Collection/F2-178-2006E.pdf.

Carlson, Mark. 2006. “A Brief History of the 1987 Stock Market Crash with a Discussion of the Federal Reserve Response.” Finance and Economics Discussion Series. Washington, DC: Federal Reserve Board, Divisions of Research & Statistics and Monetary Affairs.

Carr, Jack, Frank Mathewson, and Neil Quigley. 1995. “Stability in the Absence of Deposit Insurance: The Canadian Banking System 1890–1966.” Journal of Money, Credit, and Banking 27 (4): 1137–58.

Chant, John. 2008. “The ABCP Crisis in Canada: The Implications for the Regulation of Financial Markets.” Paper prepared for the Expert Panel on Securities Regulation.

Chant, John, Alexandra Lai, Mark Illing and Fred Daniel. 2003. “Essays on Financial Stability,” Bank of Canada Technical Report No. 95, September.

Chappatta, Brian. 2023. “SVB’s 44-hour collapse was rooted in Treasury bets during pandemic.” Bloomberg, March 10. https://www.bloomberg.com/news/articles/2023-03-10/svb-spectacularly-fails-after-unthinkable-heresy-becomes-reality?leadSource=uverify%20wall.

Choe, Stan. 2023. “Deal to buy Silicon Valley Bank calms bank fears, for now.” Associated Press, March 27. https://ottawa.citynews.ca/national-business/deal-to-buy-silicon-valley-bank-calms-bank-fears-for-now-6762165

Clarfelt, Harriet, Martha Muir, Leo Lewis, and William Langley. 2023. “US bank shares rebound after rout sparked by SVB failure.” Financial Times, March 14.

CNN. 1998. “Fed cuts key interest rates.” October 15. https://money.cnn.com/1998/10/15/economy/fed/.

Cooban, Anna. 2023. “Credit Suisse got its lifeline. Investors are unconvinced.” CNN News, March 17. https://www.cnn.com/2023/03/17/investing/credit-suisse-shares-drop-despite-lifeline/index.html.

Copeland, Rob, Lauren Hirsch, Alan Rappeport, and Maureen Farrell. 2023. “Wall Street’s biggest banks rescue teetering First Republic.” New York Times, March 16. https://www.nytimes.com/2023/03/16/business/first-republic-bank-sale.html.

Cotis, Jean-Philippe. 2006. “Benchmarking Canada’s Economic Performance,” International Productivity Monitor 3 (Fall): 1–20.

Ciuriak, Dan. 2013. “Canadian and US Financial Sector Stability Differences over Long History: Is There a Unifying Explanation?” Working Paper, available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2246150

__________. 2016. “Book Review: ‘Fragile by Design: The Political Origins of Banking Crises & Scarce Credit’ by Charles W. Calomiris and Stephen H. Haber,” 24 June 2016. Available on SSRN, http://papers.ssrn.com/abstract=2797098

__________. 2023. “The Silicon Valley Bank Failure: Historical Perspectives and Knock-on Risks.” Working Paper. Available at SSRN: https://papers.ssrn.com/abstract=4392931

Curry, Timothy, and Lynn Shibut, 2000. “The Cost of the Savings and Loan Crisis: Truth and Consequences.” FDIC Banking Review, December, 26–8.

Curtiss, C. A. 1948. “Banking,” in W. Stewart Wallace (ed.), The Encyclopedia of Canada, Vol. I, Toronto: University Associates of Canada: 151-164.

Davis, Lance E., and Robert E. Gallman. 2001. Evolving Financial Markets and International Capital Flows: Britain, the Americas, and Australia, 1865–1914. Cambridge: Cambridge University Press.

Defend, Monica, Vincent Mortier, and Matteo Germano. 2023. “No systemic risk from SVB failure, but watch out for areas of vulnerability.” Amundi Investment Talks, March 14. https://research-center.amundi.com/article/no-systemic-risk-svb-failure-watch-out-areas-vulnerability.

Dimand, Robert W., and Robert H. Koehn. 2009. “Canada in Two World Financial Crises: Why No Canadian Banks Failed or Were Bailed Out in the 1930s or 2000s,” Paper Presented at the IVth Bi-Annual Conference on The Financial and Monetary Crisis: Rethinking Economic Policies and Redefining the Architecture and Governance of International Finance, University of Bourgogne, Dijon, December 12.

Dodge, David. 2011. “Public Policy for the Canadian Financial System: From Porter to the Present and Beyond.” In New Directions for Intelligent Government in Canada: Papers in Honour of Ian Stewart, ed. Fred Gorbet and Andrew Sharpe, 81–100. Ottawa: Centre for the Study of Living Standards.

Dowd, Kevin. 1999. “Too Big to Fail? Long-Term Capital Management and the Federal Reserve.” Briefing Paper 52. Washington, DC: Cato Institute.

Escobar, Sabrina. 2022. “First Horizon stock surges on deal to be bought by TD Bank.” Barron’s, February 28. https://www.barrons.com/articles/first-horizon-stock-price-td-bank-acquisition-51646051475.

External Advisory Committee on Smart Regulation. 2004. Smart Regulation: A Regulatory Strategy for Canada. Ottawa: Privy Council Office. http://epe.lac-bac.gc.ca/100/206/301/pco-bcp/committees/smart_regulation-ef/2006-10-11/www.pco-bcp.gc.ca/smartreg-regint/en/08/rpt_fnl.pdf.

FBI. 2007. “Mortgage Fraud Report 2006.” Washington, DC: Federal Bureau of Investigation, May. https://www.fbi.gov/stats-services/publications/mortgage-fraud-2006.

FCIC (Financial Crisis Inquiry Commission). 2011. The Financial Crisis Inquiry Report. Washington, DC: US Government Printing Office.

FDIC (Federal Deposit Insurance Corporation). 1997. An Examination of the Banking Crises of the 1980s and Early 1990s, Volume 1. Washington, DC: FDIC. http://www.fdic.gov/databank/hist80.

———. 2007. “Mortgage Loan Fraud Industry Assessment Based on Suspicious Activity Report Analysis.” Financial Institution Letter FIL-4-2007, January 16.

———. 2023a. “Subsidiary of New York Community Bancorp, Inc., to assume deposits of signature Bridge Bank, N.A..” Press Release, March. 19. https://www.fdic.gov/news/press-releases/2023/pr23021.html.

———. 2023b. “JPMorgan Chase Bank, National Association, Columbus, Ohio assumes all the deposits of First Republic Bank, San Francisco, California.” Press Release, May 1. https://www.fdic.gov/news/press-releases/2023/pr23034.html.

———. 2023c. “First–Citizens Bank & Trust Company, Raleigh, NC, to Assume All Deposits and Loans of Silicon Valley Bridge Bank, N.A., from the FDIC.” Press Release, March 26. https://www.fdic.gov/news/press-releases/2023/pr23023.html.

———. 2023d. “Bank Failures in Brief – 2023.” https://www.fdic.gov/bank/historical/bank/bfb2023.html.

Federal Reserve Bank of St. Louis. n.d. “10-Year Treasury Constant Maturity Minus 3-Month Treasury Constant Maturity.” https://fred.stlouisfed.org/series/T10Y3M.

———. n.d. “Total Assets, All Commercial Banks, Billions of U.S. Dollars, Weekly, Seasonally Adjusted.”

FOMC (Federal Open Market Committee). 1998a. “Minutes of the Federal Open Market Committee, September 29, 1998.” Federal Reserve Board. https://www.federalreserve.gov/fomc/minutes/19980929.htm

———. 1998b. “Minutes of the Federal Open Market Committee, November 17, 1998.” Federal Reserve Board. https://www.federalreserve.gov/fomc/minutes/19981117.htm.

Foster, Sarah. 2023. “Will the Fed raise interest rates one more time this year? Some economists aren’t convinced.” Bankrate, November 8. https://www.bankrate.com/banking/federal-reserve/how-much-will-fed-raise-rates-in-2023/#money.

Freedman, Charles. 1998. “The Canadian Banking System.” Paper delivered at the Conference on Developments in the Financial System: National and International Perspectives, Jerome Levy Economics Institute of Bard College, Annandale-on-Hudson, NY, April 10–11.

Friedman, Milton and Anna J. Schwartz. 1963. A Monetary History of the United States, 1867-1960. Princeton University Press.

Financial Stability Board. 2011. “Shadow Banking: Scoping the Issues: A Background Note of the Financial Stability Board.” Basel: Financial Stability Board, April 12. https://www.fsb.org/2011/04/shadow-banking-scoping-the-issues/.

———. 2012. “Global Shadow Banking Monitoring Report 2012,” Basel: Financial Stability Board, November 18.

FSRA (Financial Services Regulatory Authority of Ontario). 2023. “History of Closed Insured Institutions.” Toronto. https://www.fsrao.ca/consumers/credit-unions-and-deposit-insurance/find-credit-union-or-caisses-populaires-ontario/history-closed-insured-institutions.

GAO (General Accounting Office). 1997. “Financial Crisis Management: Four Financial Crises in the 1980s.” Staff Study GAO/GGD-97-96. Washington, DC.

Geithner, Timothy F. 2008. “Reducing Systemic Risk in a Dynamic Financial System: Remarks by Mr Timothy F Geithner, President and Chief Executive Officer of the Federal Reserve Bank of New York, at The Economic Club of New York, New York, 9 June 2008.” BIS Review 74.

Giang, Vivian. 2023. “Banking turmoil: What we know,” New York Times, March 15. https://www.nytimes.com/article/svb-silicon-valley-bank-explainer.html.

Gelzinis, Greg. 2019. “Strengthening the Regulation and Oversight of Shadow Banks.” Washington, DC: Center for American Progress, July 18. https://www.americanprogress.org/article/strengthening-regulation-oversight-shadow-banks/

Goetzmann, William N., and Frank Newman. 2010. “Securitization in the 1920's.” NBER Working Paper 15650. Cambridge, MA: National Bureau of Economic Research. http://www.nber.org/papers/w15650/.

Gorton, Gary B. 2010. “Slapped in the Face by the Invisible Hand: Banking and the Panic of 2007.” In Slapped in the Face by the Invisible Hand: Banking and the Panic of 2007, chap. 2. New York: Oxford University Press.

Gorton, Gary B., and Andrew Metrick. 2010. “Regulating the Shadow Banking System.” Brookings Papers on Economic Activity, Fall, 261–312.

Griffin, John M. 2021. “Ten Years of Evidence: Was Fraud a Force in the Financial Crisis?” Journal of Economic Literature 59 (4): 1293–321.

Grossman, Richard S., and Hugh Rockoff. 2015. “Fighting the Last War: Economists on the Lender of Last Resort.” NBER Working Paper 20832. Cambridge, MA: National Bureau of Economic Research. http://www.nber.org/papers/w20832.

Gruenberg, Martin J. 2023. “Remarks by Martin J. Gruenberg, Chairman, FDIC, on The Resolution of Large Regional Banks – Lessons Learned.” Federal Deposit Insurance Corporation, August 14. https://www.fdic.gov/news/speeches/2023/spaug1423.html.

Guardian. 2007. “When the music stops.” November 6. https://www.theguardian.com/commentisfree/2007/nov/06/comment.business.

Hart, Michael M. 2006. Taking Charge of Canada-US Regulatory Convergence. Commentary 229. Toronto: C.D. Howe Institute.

Hart, Michael, and William Dymond, 2007. “Trade Theory, Trade Policy, and Cross-Border Integration.” In Trade Policy Research 2006, ed. Dan Ciuriak, 103–58. Ottawa: Foreign Affairs and International Trade Canada.

Haubrich, Joseph G. 1990. “Nonmonetary Effects of Financial Crises: Lessons from the Great Depression in Canada,” Journal of Monetary Economics 25 (2): 223–52.

———. 2007. “Some Lessons on the Rescue of Long-Term Capital Management.” Policy Discussion Paper 19. Cleveland: Federal Reserve Bank of Cleveland, April.

Hirsch, Lauren. 2023a. “Bank turmoil is paving the way for even bigger ‘shadow banks.’” New York Times, May 6. https://www.nytimes.com/2023/05/06/business/dealbook/bank-crisis-shadow-banks.html.

———. 2023b. “Small banks rush to reassure investors as shares plunge.” New York Times, May 4. https://www.nytimes.com/2023/05/04/business/pacwest-stock.html.

Hughes, Stephanie. 2023. “TD Bank and First Horizon call off US$13.4-billion merger deal.” Financial Post, May 4. https://financialpost.com/fp-finance/banking/td-bank-first-horizon-terminate-merger.

IMF (International Monetary Fund). 2019. “Canada: Financial System Stability Assessment,” IMF Country Report 19/177. Washington, DC: International Monetary Fund.

Independent. 1998. “Bear Stearns’ $500m call triggered LTCM crisis.” September 26.

Jackson, James K. 2013. “Financial Market Supervision: Canada’s Perspective.” CRS Report to Congress R40687, April 4. Washington, DC: Congressional Research Service.

Jiang, Erica Xuewei, Gregor Matvos, Tomasz Piskorski, and Amit Seru. 2023. “Monetary Tightening and U.S. Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?” NBER Working Paper 31048. Cambridge, MA: National Bureau of Economic Research. https://www.nber.org/papers/w31048.

Johnson, Daniel. 2023. “After Silicon Valley Bank’s collapse, what would happen if a Canadian bank failed?” BNN Bloomberg, March 15. https://www.ctvnews.ca/business/after-silicon-valley-bank-s-collapse-what-would-happen-if-a-canadian-bank-failed-1.6314618.

Kaplan, Cathy M. 2014. “Securitisation: A Brief History and the Road Ahead.” Who’s Who Legal, August 8. https://whoswholegal.com/features/securitisation-a-brief-history-and-the-road-ahead.

Kronick Jeremy M., and Mawakina Bafale. 2022. “Deepening Canadian Capital Markets.” Intelligence Memo. Toronto: C.D. Howe Institute, 26 July. https://www.cdhowe.org/intelligence-memos/kronick-bafale-deepening-canadian-capital-markets.

Kryzanowski, Lawrence, and Gordon S. Roberts. 1993. “Canadian Banking Solvency, 1922–1940.” Journal of Money, Credit, and Banking 25 (1): 361–76.

———. 1998, “Capital Forbearance: Depression-era Experience of Life Insurance Companies.” Canadian Journal of Administrative Sciences 15 (1): 1–16.

———. 1999. “Perspectives on Canadian Bank Insolvency in the 1930s.” Journal of Money, Credit and Banking 31 (1): 130–6.

Lam, Eric. 2009. “CIBC ranked 15th in largest global bank losses for 2008.” Financial Post, July 2.

Macdonald, David. 2012. “The Big Banks’ Big Secret.” Report, Canadian Centre for Policy Alternatives, April. https://policyalternatives.ca/sites/default/files/uploads/publications/National%20Office/2012/04/Big%20Banks%20Big%20Secret.pdf

Macmillan Commission. 1933. Report of the Royal Commission on Banking and Currency in Canada. Chair, Lord Macmillan. https://publications.gc.ca/collections/collection_2014/bcp-pco/CP32-129-1933-1-eng.pdf.

McCulley, Paul. 2009. “The Shadow Banking System and Hyman Minsky’s Economic Journey.” In Insights into the Global Financial Crisis, ed. Laurence B. Siegel, 257–68. [n.p.]: Research Foundation of CFA Institute.

McDade, Susan E. 1989. “Latin American Debt Crisis and the Canadian Commercial Banks.” ISS Working Papers 53, General Series. The Hague: Erasmus University, International Institute of Social Studies.

Mor, Federico. 2018. “Royal Bank of Scotland Bailout: 10 Years and Counting.” Insight, House of Commons Library, October 12. https://commonslibrary.parliament.uk/royal-bank-of-scotland-bailout-10-years-and-counting/.

Nguyen, Tomson H., and Henry N. Pontell. 2010. “Mortgage Origination Fraud and the Global Economic Crisis: A Criminological Analysis.” Criminology and Public Policy 9 (3): 591–612.

Neufeld, Edward P. 1972. The Financial System of Canada. Toronto: Macmillan of Canada.

Nishant, Niket, and Manya Saini. 2023. “PacWest stock soars on $1.1 billion buyout deal with Banc of California.” Reuters, July 26. https://www.reuters.com/markets/deals/pacwest-stock-soars-11-bln-buyout-deal-2023-07-26/.

Noiseux, Marie Hélène. 2002, “Canadian Bank Mergers, Rescues and Failures.” PhD thesis, Concordia University.

Ontario Securities Commission. 2009. “In the Matter of the Securities Act R.S.O. 1990, c. S.5, as Amended and Coventree Inc., Geoffrey Cornish and Dean Tai: Statement of Allegations.” Ontario Securities Commission, December 7.

OSFI (Office of the Superintendent of Financial Institutions). 2022. “Who We Regulate.” https://www.osfi-bsif.gc.ca/Eng/wt-ow/Pages/wwr-er.aspx.

———. 2023a. “Foreign Bank Branches.” https://www.osfi-bsif.gc.ca/Eng/fi-if/dti-id/fbb-sbe/Pages/default.aspx.

———. 2023b. “Superintendent of Financial Institutions takes temporary control of Silicon Valley Bank’s Canadian branch.” Press Release, March 12. https://www.osfi-bsif.gc.ca/Eng/osfi-bsif/med/Pages/nr20230312.aspx.

PacWest. 2023. “Banc of California and PacWest announce transformational merger and $400 million equity raise from Warburg Pincus and Centerbridge.” Company Release, July 25. https://www.pacwestbancorp.com/news-market-data/news/news-details/2023/Banc-of-California-and-PacWest-Announce-Transformational-Mergerand-400-Million-Equity-Raise-from-Warburg-Pincus-and-Centerbridge/default.aspx.

Patrick, Margot, Ben Dummett, Dana Cimilluca, and Patricia Kowsmann. 2023. “UBS agrees to buy Credit Suisse for more than $3 billion.” Wall Steet Journal, March 19. https://www.wsj.com/articles/ubs-offers-1-billion-to-take-over-credit-suisse-bfac51fa.

Perino, Michael. 2012. “Crisis, Scandal and Financial Reform during the New Deal.” Legal Studies Research Paper Series 12-0004. Jamaica, NY: St. John’s School of Law. May.

Poapst. J.V. 1956. “The National Housing Act, 1954.” Canadian Journal of Economics and Political Science 22 (2): 234–43.

Pollard, Amelia, Giulia Morpurgo and Reshmi Basu. 2023. “SVB Isn’t a ‘Lehman Moment’ – But Could It Be a ‘Bear Stearns’ One?” Bloomberg, 14 March. https://www.bloomberg.com/news/newsletters/2023-03-14/what-s-the-next-banking-crisis-after-svb-analysts-say-it-won-t-be-last

Pontell, Henry N., William K. Black, and Gilbert Geis. 2014. “Too Big to Fail, Too Powerful to Jail? On the Absence of Criminal Prosecutions after the 2008 Financial Meltdown.” Crime, Law and Social Change 61: 1–13.

Punchard, Hilary. 2023. “OSFI takes permanent control of SVB’s Canadian branch assets.” BNN Bloomberg, March 15. https://www.bnnbloomberg.ca/osfi-takes-permanent-control-of-svb-s-canadian-branch-assets-1.1896031.

Rappeport, Alan. 2023. “F.D.I.C. proposes broadening bank insurance for businesses.” New York Times, May 1. https://www.nytimes.com/2023/05/01/business/fdic-bank-insurance-proposals.html.

Ratnovski, Lev, and Rocco Huang. 2009. “Why Are Canadian Banks More Resilient?” IMF Working Paper WP/09/152. Washington, DC: International Monetary Fund. July.

RBC. 2023. “Royal Bank of Canada Investor Presentation, Q3/2023.” https://www.rbc.com/investor-relations/_assets-custom/pdf/irdeck2023q3.pdf.

Ricks, Morgan. 2016. The Money Problem: Rethinking Financial Regulation. Chicago: University of Chicago Press.

Rowe Jr., and James L. “How a bank lent itself to disaster.” Washington Post, July 29. https://www.washingtonpost.com/archive/politics/1984/07/29/how-a-bank-lent-itself-to-disaster/ccff5657-af6b-4045-bc63-de6100e7dc07/.

Rubinstein, Mark. 2000. “Comments on the 1987 Stock Market Crash: Eleven Years Later.” Risks in Accumulation Products, Society of Actuaries: 1–6.

Rush, Geoff. 2023. “Banking in Transition: Fiscal Year 2022 Results Analysis: Analysis of the Six Major Canadian Banks’ Year-End Financial Results for 2022.” KPMG. https://kpmg.com/ca/en/home/insights/2023/01/banking-in-transition-fiscal-year-2022-results-analysis.html.

Russell, Karl, and Christine Zhang. 2023. “3 failed banks this year were bigger than 25 that crumbled in 2008.” New York Times, May 1. https://www.nytimes.com/interactive/2023/business/bank-failures-svb-first-republic-signature.html.

Sanati, Cyrus. 2010. “Prince finally explains his dancing comment.” New York Times, April 8. https://archive.nytimes.com/dealbook.nytimes.com/2010/04/08/prince-finally-explains-his-dancing-comment/.

Santomero, Anthony M., and Paul Hoffman. 1998. “Problem Bank Resolution: Evaluating the Options.” Wharton School Working Paper Series 98-05-B. Philadelphia: University of Pennsylvania, Wharton School.

Schneider, Howard, and Lindsay Dunsmuir. 2023. “Fed’s Powell sets the table for higher and possibly faster rate hikes.” Reuters, March 8. https://www.reuters.com/markets/us/feds-powell-hill-appearance-update-views-status-disinflation-2023-03-07/.

Scholes, Myron S. 2000. “Crisis and Risk Management.” American Economic Review 90 (2): 17–21.

Shaw, C.J. 2006. “Big Bank Merger Review in Canada.” Journal of International Banking Law and Regulation 8: 474-486.

Shearer, Ronald A. 1977. “The Porter Commission Report in the Context of Earlier Canadian Monetary Documents.” Canadian Journal of Economics 10 (1): 34–49.

———. 1978. “Proposals for the Revision of Banking Legislation.” Canadian Journal of Economics 11 (1): 121–36.

Sidel, Robin, David Enrich, and Dan Fitzpatrick. 2008.“WaMu is seized, sold off to J.P. Morgan, in largest failure in U.S. banking history.” Wall Street Journal, September 26. https://www.wsj.com/articles/SB122238415586576687.

Smialek, Jeanna. 2023. “Fed slams its own oversight of Silicon Valley Bank in post-mortem.” New York Times, April 28. https://www.nytimes.com/2023/04/28/business/economy/fed-silicon-valley-bank-failure-review.html.

Son, Hugh. 2023. “SVB customers tried to withdraw nearly all the bank’s deposits over two days, Fed’s Barr testifies.” CNBC, March 28. https://www.cnbc.com/2023/03/28/svb-customers-tried-to-pull-nearly-all-deposits-in-two-days-barr-says.html.

Sprague, O.M.W. 1910. History of Crises under the National Banking Act. Washington, DC: US Government Printing Office.

Sweet, Ken, Christopher Rugaber, Chris Megerian, and Cathy Bussewitz. 2023. “U.S. government races to reassure that banking system is safe.” CTV News, March 13. https://www.ctvnews.ca/business/u-s-government-races-to-reassure-that-banking-system-is-safe-1.6310632.

TD. 2022. Annual Report, 2022. htps://www.td.com/document/PDF/ar2022/ar2022-Complete-Report.pdf.

———. 2023. “TD Bank Group reports third quarter 2023 results: Report to shareholders, three and nine months ended July 31, 2023.” https://www.td.com/document/PDF/investor/2023/2023-Q3_Report_to_Shareholders_F_EN.pdf.

Tedesco, Theresa, and John Turley-Ewart. 2009. “Canadian Banks: A Better System.” National Post, April 5. https://nationalpost.com/news/canadian-banks-a-better-system.

Todd, Tim. 2010. “Integrity, Fairness and Resolve: Lessons from Bill Taylor and the Last Financial Crisis.” Federal Reserve Bank of Kansas City. https://www.kansascityfed.org/AboutUs/documents/6510/integrityfairnessandresolve.pdf

Turley-Ewart, John. 2004. “The Bank That Went Bust.” The Beaver, 1 August. https://www.canadashistory.ca/explore/business-industry/the-bank-that-went-bust

Wagster, John D. 2009. “Canadian-Bank Stability in the Great Depression: The Role of Capital, Implicit Government Support and Diversification.” Unpublished manuscript, Wayne State University.

Walter, John R. 2005. “Depression-Era Bank Failures: The Great Contagion or the Great Shakeout?” Federal Reserve Bank of Richmond Economic Quarterly 91 (1): 39–54. https://www.richmondfed.org/-/media/RichmondFedOrg/publications/research/economic_quarterly/2005/winter/pdf/walter.pdf.

Wells, Donald R. 1987. “Banking Before the Federal Reserve: The U.S. and Canada Compared.” The Freeman, Ideas On Liberty: 231-235.

Wicker, Elmus. 2001. “Banking Panics in the US: 1873–1933.” Net Encyclopaedia. Economic History Association. https://eh.net/encyclopedia/banking-panics-in-the-us-1873-1933/.

Wighton, David. 2017. “What we have learned 10 years after Chuck Prince told Wall St to keep dancing.” Financial News, July 14. https://www.fnlondon.com/articles/chuck-princes-dancing-quote-what-we-have-learned-10-years-on-20170714.

Witmer, Jonathan, and Lorie Zorn. 2007. “Estimating and Comparing the Implied Cost of Equity for Canadian and U.S. Firms.” Bank of Canada Working Paper 2007–48. Ottawa: Bank of Canada. https://www.bankofcanada.ca/2007/09/working-paper-2007-48/.

Online Appendix

US and Canadian Experiences, Regulatory Policies, and Tipping Points

The United States has a unique history of frequency of financial crises and financial institution failures. In its early history, the United States had recurring financial crises/panics/incipient panics, including in 1797, 1815, 1819, 1825, 1833, 1837, 1839, 1857, 1860–61, 1873, 1884, 1890, 1893, 1897, 1907 (the event which prompted the formation of the Federal Reserve System) and 1914.

The interwar period featured additional waves of bank failures. In particular, there were numerous failures in the agricultural states in the 1920s – although these were not associated with panic-type bank runs but rather reflected shocks to the real economy (Walter 2005) – followed by a total of over 9,000 failures nationwide during the 1930–33 period, which witnessed four separate episodes of bank panic (Calomiris and Mason 2003).

Following an extended period of relative calm from the 1940s through the 1970s, US bank failures surged between 1980 and 1994, including in the mutual savings bank sector, the commercial bank sector and the savings and loan sector.

The mutual savings bank problems surfaced early. Between late 1981 and year-end 1985, the Federal Deposit Insurance Corporation (FDIC) conducted 17 assisted mergers or acquisitions of mutual savings banks with total assets of nearly US$24 billion, at a cost estimated at about US$2.2 billion (FDIC 1997, chap. 6). Subsequently, 58 more savings banks with combined assets of about US$60.8 billion failed, including some that had been restructured in the first wave, at a cost to the public purse of US$6.6 billion (FDIC 1997, appendix table 6-A.1), bringing the overall total of savings bank failures during this period to 75, with total assets of US$85 billion, and generating a cost to the public of US$8.8 billion.

A much bigger problem erupted in the commercial bank sector. Between 1980 and 1994, more than 1,600 banks insured by the FDIC were closed or received FDIC financial assistance, with a total cost to the taxpayer estimated at US$36.3 billion (FDIC 1997, chap. 1). Prominent events in this period included the failure of an Oklahoma bank, Penn Square, in 1982 during the oil patch downturn; this had significant ripple effects due to loan participations it had sold to other banks. The Penn Square closure represented the largest bank failure in which uninsured depositors suffered losses up to that point in the FDIC’s history (FDIC 1997, chap. 3). Shortly after, in 1984, Continental Illinois collapsed, in part due to its connections to Penn Square. Continental Illinois was at the time the seventh-largest bank in the United States, the largest US commercial and industrial lender and one of the most highly regarded by the market in the year that preceded its collapse (see, for example, Rowe Jr. 1984). This crisis, featuring an electronic bank run by wholesale depositors, cost the FDIC US$1.1 billion in resolution costs and gave rise to the sobriquet “too big to fail,” as well as a debate about “nationalization” of banks due to the public capital injected to keep them from failing (FDIC 1997, chap. 7). These incidents, however, turned out to be just the prologue: at the height of the banking crisis in 1988–92, during the bust in the commercial real estate market, on average one bank failed in the United States every day.

Unfolding concurrently with the commercial banking crisis, the US savings and loan crisis resulted in the closing of 1,043 thrifts holding US$519 billion in assets, the insolvency of the Federal Savings and Loan Insurance Corporation, the federal insurer for the thrift industry, and a public bailout cost of US$123.8 billion (Curry and Shibut 2000).

(Todd 2010).

US capital markets then generated in short order several additional bouts of financial stress that threatened the banking system and pressured the Federal Reserve to make significant adjustments to monetary policy to avert systemic risks. The stock market crash of 1987 brought the US financial system to the point of breakdown and raised fears of a widespread credit crunch, requiring the Federal Reserve to inject liquidity into markets and to prompt commercial banks to extend credit to securities firms, despite any concerns they might have had about the size of their exposure (Carlson 2006; GAO 1997). Through contagion, the effects spread worldwide and prompted new regulatory initiatives (such as circuit breakers). To this day, the event remains poorly understood despite the fact that it provoked extensive study because of the spanner it threw into the workings of conventional finance theory.