To: Canada’s Economic Policymakers

From: Jeremy M. Kronick, Steve Ambler and Mawakina Bafale

Date: March 28, 2024

Re: New Tools to Analyze the Real Economy

The C.D. Howe Institute’s mission is to raise living standards by fostering economically sound public policies, including in the areas of monetary policy and financial stability.

In order to make informed policy recommendations, we need reliable and robust economic data. Researchers at the Institute have created many unique data sets and used them in their analyses and recommendations.

Among recent examples, our novel vulnerability barometer, which takes into account the amount Canadian households have to spend out of their income to service their debt, was able to better anticipate recessions in Canada – including the Great Financial Crisis – than similar existing measures. In another instance, we highlighted the return of the relationship between money growth and inflation during the COVID pandemic, and how a focus on monetary aggregates would have shown the lurking inflation danger during 2021, before the Bank started hiking the overnight rate.

In our latest C.D. Howe Institute paper, we outlined a series of indicators – all available on its website – using data sets developed in past Institute work. We also laid out how these indicators can be helpful to policymakers, including the Bank of Canada and the Office of the Superintendent of Financial Institutions (OSFI), particularly in the setting of the overnight rate target and monitoring financial stability. The latter includes OFSI’s setting of the Domestic Stability Buffer, or DSB, designed to cover potential losses at Canada’s largest banks in periods of financial stress.

The database not only brings together series used in earlier C.D. Howe Institute studies, but also introduces a novel, publicly available, leading indicator of economic activity.

The paper explains how each data series is constructed and how it is used to produce a particular indicator. It then shows the evolution of these indicators and their most recent values. Finally, we look at recent developments in the financial and economic indicators in this new toolkit in relation to the Bank of Canada’s monetary policy stance and OSFI’s decisions around the DSB.

These data sets are not a complete toolkit of variables. They are meant to present unique insights not necessarily available with other publicly (or for policymakers, privately) available data.

We discuss the following economic and financial indicators:

- A financial vulnerability indicator, which tracks vulnerabilities across the banking, corporate, housing, and household sectors, and which successfully flagged previous periods of financial stress and recessions.

- A diffusion index, which measures the extent to which expansions and contractions are widespread across different sectors of the economy, and which previously confirmed the breadth of contractions during the 2008 and 2020 recessions.

- A money overhang index, which tracks the gap between trend money growth and trend inflation, which flashed a strong warning signal of coming inflation in 2020 and early 2021 and is now signaling a decrease in inflation.

- A monetary policy stance indicator, which uses different versions of the so-called Taylor rule to estimate the appropriate level for the Bank of Canada’s target overnight rate, and which suggests today a rate in line with the Bank’s current monetary policy stance.

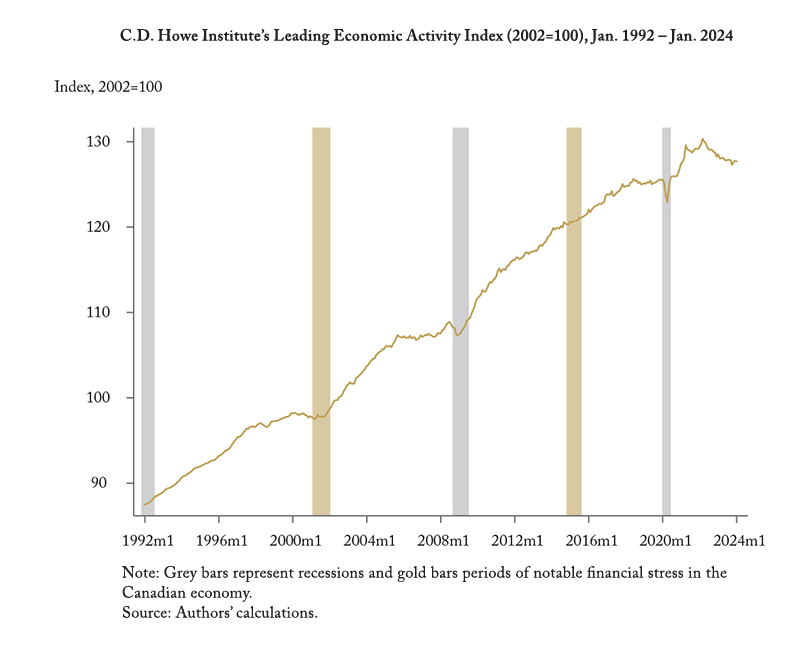

- A leading economic indicator, which predicted previous economic downturns, and which has been trending downward since the Bank of Canada began its last tightening cycle (see Figure).

- A statistical decomposition of Canadian inflation into supply-side and demand-side drivers, and which currently indicates that much of the remaining pressure on inflation is coming from the supply side.

The indicators suggest that the Bank of Canada should be at the end of its tightening cycle. They also suggest that even if financial risks have recently risen, the weak macroeconomic context means that an increase in the DSB, currently set at 3.5 percent of risk-weighted assets, would be counterproductive by restricting credit issued by the big six banks – most likely because of the impact on the cost of lending – and possibly amplifying any economic downturn.

Jeremy M. Kronick is Associate Vice President, and Director of the Centre on Financial and Monetary Policy at the C.D. Howe Institute, where Steve Ambler, emeritus professor of economics, Université du Québec à Montréal, is the David Dodge Chair in Monetary Policy, and Mawakina Bafale is a research associate.

To send a comment or leave feedback, email us at blog@cdhowe.org.

The views expressed here are those of the authors. The C.D. Howe Institute does not take corporate positions on policy matters.